Periodic/Sector reports

Plantation: Softer Stance On Indonesia’s Export Policy

OVERWEIGHT (Maintained)

Analyst

Highlights

- DSI's role as a pricing oversight body, rather than a sole exporter, alleviates concerns over export bottlenecks and palm oil supply disruptions.

- We expect the regulatory discount on Indonesian plantation stocks to narrow as the latest development points to limited earnings impact on planters.

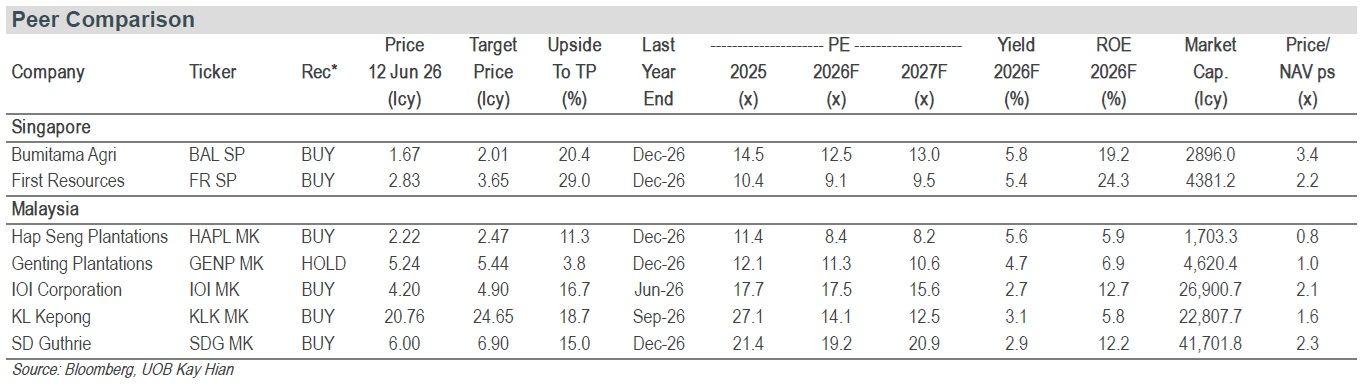

- Maintain OVERWEIGHT. Upgrade First Resources to BUY (from HOLD) with an unchanged target price of S$3.65, and reiterate our positive view on Bumitama Agri with an unchanged target price of S$2.01.

Analysis

- DSI: From gatekeeper to auditor. Per official sources, Danantra Sumberdaya Indonesia (DSI) will no longer assume the sole-exporter role targeted for Jan 27. Exporters retain commercial relationships with buyers but must justify declared pricing, with below-market values subject to revision. The retreat removes the most disruptive reading of the scheme just 11 days into its transition phase.

- Implications. We view the latest development as modestly positive for Indonesian planters. By preserving direct commercial relationships between exporters and overseas buyers, concerns over export bottlenecks and trade-flow disruptions should largely dissipate. Consequently, we expect limited impact on upstream planters' earnings and a gradual narrowing of the regulatory discount currently reflected in Indonesian plantation stocks. The supply-dislocation premium that has supported CPO prices since the initial announcement should also fade, while expectations of demand substitution towards Malaysian CPO may moderate.

- Policy overhang remains, but risks have eased. That said, the overhang is unlikely to disappear entirely. Key details surrounding DSI's pricing review mechanism and long-term role remain unclear, with PP No. 24/2026 envisaging a larger role for DSI from Jan 27. Nonetheless, the swift recalibration following adverse market reaction and industry pushback suggests policymakers remain focused on curbing under-invoicing and transfer pricing rather than materially disrupting established trade flows.

- El Niño could potentially pressure CPO supply in 2027. The US National Oceanic and Atmospheric Administration officially declared an El Niño episode on 11 June, upgrading its alert status to an El Niño Advisory. However, we maintain our near-term CPO production expectations considering that moisture stress typically hits fresh fruit bunch (FFB) yields with a six- to 12-month lag. The immediate price effect instead skews bearish, as past El Niño episodes historically favour benign US Midwest summers and better South American soybean rainfall, suggesting favourable conditions for the 2026/27 season, weighing on the soft-oils complex where crude palm oil's (CPO) competitiveness is already stretched. The bullish leg should arrive in 2027, where accumulated moisture stress presents an upside risk to our 2027 CPO price assumption of RM4,400/tonne.

Valuation/Recommendation

- Maintain OVERWEIGHT. Following the latest development on Indonesia’s export policy, we have turned more constructive on the Indonesian based planters under our coverage. Since concerns over the export framework emerged, First Resources and Bumitama have declined by 23%/18% respectively, significantly underperforming Malaysian peers, with the KLPLTN index down only 4%, despite CPO prices remaining resilient, trading at around RM4,500 per tonne. We believe the recent sell-off has largely priced in the regulatory risk and expect sentiment to improve as policy uncertainties ease. Valuations remain supported by the companies’ attractive yield, underpinned by their resilient earnings, strong cash generation and healthy financial position. The broader sector outlook remains favourable, driven by structural demand growth from expanding regional biodiesel mandates, while a potential El Niño event could tighten supply, hence providing further upside to CPO prices.

- First Resources (FR SP): Upgrade to BUY; target price unchanged at S$3.65, based on 12x 2026F PE. We upgrade FR to BUY following the share price correction, which presents compelling upside to our target price. We expect FR to deliver a 9% yoy earnings growth in 2026, supported by the full-year contribution from the Austindo Nusantara Jaya acquisition, with management guiding for 5-10% FFB production growth. FR may also potentially benefit from increased biodiesel blending allocation from the B50 implementation.

- Bumitama Agri (BAL SP): Maintain BUY; target price unchanged at S$2.01, based on 14x 2026F PE. We believe BAL’s premium valuation is warranted given its positive dividend track records and relatively stable production profile. BAL’s earnings are forecasted to grow 15% yoy in 2026, underpinned by resilient operational performance and stronger CPO prices. FFB growth is on track to meet the upper end of management's 0-5% guidance range, as output rose 6.5% in 1Q26, while the group’s external FFB purchase continues to support mill utilisation above 75%.

Sector Catalyst/Risk

- Stronger-than-expected CPO prices.

- Dry and hot weather alongside the potential for El Niño in 2H26 may threaten FFB yield and industry supply.

- Reinstatement of DSI’s role as the sole exporter and domestic price setter.

| Timeline: DSI-related announcements | |

| Date | Event |

| 20 May 26 | President Prabowo announces that all exports of coal, crude palm oil and ferroalloys will be routed through DSI, a newly created entity 99%-owned by sovereign wealth fund Danantara. The Indonesian KPBN’s CPO prices benchmark fell 5.77% following the announcement. |

| 1 Jun 26 | Transition phase begins, scheduled to run until at least 31 Aug 26. Exporters continue to sell independently and existing contracts are honoured, but all shipments must now be reported to DSI through the customs directorate's CEISA 4.0 digital platform. A parallel regulation requiring natural-resource export proceeds to be retained onshore takes effect the same day. |

| Early Jun 26 | Palm oil exporters reportedly cancel planned cargo shipments for fear of breaching the new rules and incurring penalties, while overseas buyers hold back pending compliance clarity. Industry groups warn that Indonesian palm oil export costs (already ~36% of export value vs ~6% in Malaysia) could rise further under a single-channel regime. |

| 11 Jun 26 | Government officials signal a scale-back: DSI will no longer become the sole exporter. Its role narrows to pricing oversight: Exporters keep their commercial relationships with buyers, but must justify declared prices, with values below market benchmarks subject to revision. DSI will charge only a 0.05-0.10% administrative fee to sustain operations. |

| 1 Jan 27 | The original target for full implementation of DSI's "single-window" export control system remains nominally on the books (1 Jan 27, or as early as Sep 26). |

Source: Government announcements, media reports, UOB Kay Hian

| Summary of PP No. 24/2026: Strategic Natural Resource Export Governance | |

| BUMN export | - Strategic natural resource commodities can only be exported by a designated BUMN Export. - The BUMN Export may act as owner or sole intermediary. - The BUMN Export can determine selling prices and charge a reasonable margin. |

| Commodities covered | - Coal, ferroalloy, palm oil (including CPO, RBD palm oil and RBD palm olein). - More commodities can be added later. |

| Transition timeline | - Exports through BUMN must be implemented no later than 31 Dec 26. - The government will evaluate implementation within three months after the regulation takes effect. - The deadline can be brought forward depending on the evaluation. |

| Possible exemptions | - Companies may be exempted if they have contracts or agreements with the government that include at least investment, divestment, and domestic processing or refining commitments. |

Source: Indonesian Ministry of State Secretariate, UOB Kay Hian

Highlights

- DSI's role as a pricing oversight body, rather than a sole exporter, alleviates concerns over export bottlenecks and palm oil supply disruptions.

- We expect the regulatory discount on Indonesian plantation stocks to narrow as the latest development points to limited earnings impact on planters.

- Maintain OVERWEIGHT. Upgrade First Resources to BUY (from HOLD) with an unchanged target price of S$3.65, and reiterate our positive view on Bumitama Agri with an unchanged target price of S$2.01.

Analysis

- DSI: From gatekeeper to auditor. Per official sources, Danantra Sumberdaya Indonesia (DSI) will no longer assume the sole-exporter role targeted for Jan 27. Exporters retain commercial relationships with buyers but must justify declared pricing, with below-market values subject to revision. The retreat removes the most disruptive reading of the scheme just 11 days into its transition phase.

- Implications. We view the latest development as modestly positive for Indonesian planters. By preserving direct commercial relationships between exporters and overseas buyers, concerns over export bottlenecks and trade-flow disruptions should largely dissipate. Consequently, we expect limited impact on upstream planters' earnings and a gradual narrowing of the regulatory discount currently reflected in Indonesian plantation stocks. The supply-dislocation premium that has supported CPO prices since the initial announcement should also fade, while expectations of demand substitution towards Malaysian CPO may moderate.

- Policy overhang remains, but risks have eased. That said, the overhang is unlikely to disappear entirely. Key details surrounding DSI's pricing review mechanism and long-term role remain unclear, with PP No. 24/2026 envisaging a larger role for DSI from Jan 27. Nonetheless, the swift recalibration following adverse market reaction and industry pushback suggests policymakers remain focused on curbing under-invoicing and transfer pricing rather than materially disrupting established trade flows.

- El Niño could potentially pressure CPO supply in 2027. The US National Oceanic and Atmospheric Administration officially declared an El Niño episode on 11 June, upgrading its alert status to an El Niño Advisory. However, we maintain our near-term CPO production expectations considering that moisture stress typically hits fresh fruit bunch (FFB) yields with a six- to 12-month lag. The immediate price effect instead skews bearish, as past El Niño episodes historically favour benign US Midwest summers and better South American soybean rainfall, suggesting favourable conditions for the 2026/27 season, weighing on the soft-oils complex where crude palm oil's (CPO) competitiveness is already stretched. The bullish leg should arrive in 2027, where accumulated moisture stress presents an upside risk to our 2027 CPO price assumption of RM4,400/tonne.

Valuation/Recommendation

- Maintain OVERWEIGHT. Following the latest development on Indonesia’s export policy, we have turned more constructive on the Indonesian based planters under our coverage. Since concerns over the export framework emerged, First Resources and Bumitama have declined by 23%/18% respectively, significantly underperforming Malaysian peers, with the KLPLTN index down only 4%, despite CPO prices remaining resilient, trading at around RM4,500 per tonne. We believe the recent sell-off has largely priced in the regulatory risk and expect sentiment to improve as policy uncertainties ease. Valuations remain supported by the companies’ attractive yield, underpinned by their resilient earnings, strong cash generation and healthy financial position. The broader sector outlook remains favourable, driven by structural demand growth from expanding regional biodiesel mandates, while a potential El Niño event could tighten supply, hence providing further upside to CPO prices.

- First Resources (FR SP): Upgrade to BUY; target price unchanged at S$3.65, based on 12x 2026F PE. We upgrade FR to BUY following the share price correction, which presents compelling upside to our target price. We expect FR to deliver a 9% yoy earnings growth in 2026, supported by the full-year contribution from the Austindo Nusantara Jaya acquisition, with management guiding for 5-10% FFB production growth. FR may also potentially benefit from increased biodiesel blending allocation from the B50 implementation.

- Bumitama Agri (BAL SP): Maintain BUY; target price unchanged at S$2.01, based on 14x 2026F PE. We believe BAL’s premium valuation is warranted given its positive dividend track records and relatively stable production profile. BAL’s earnings are forecasted to grow 15% yoy in 2026, underpinned by resilient operational performance and stronger CPO prices. FFB growth is on track to meet the upper end of management's 0-5% guidance range, as output rose 6.5% in 1Q26, while the group’s external FFB purchase continues to support mill utilisation above 75%.

Sector Catalyst/Risk

- Stronger-than-expected CPO prices.

- Dry and hot weather alongside the potential for El Niño in 2H26 may threaten FFB yield and industry supply.

- Reinstatement of DSI’s role as the sole exporter and domestic price setter.

| Timeline: DSI-related announcements | |

| Date | Event |

| 20 May 26 | President Prabowo announces that all exports of coal, crude palm oil and ferroalloys will be routed through DSI, a newly created entity 99%-owned by sovereign wealth fund Danantara. The Indonesian KPBN’s CPO prices benchmark fell 5.77% following the announcement. |

| 1 Jun 26 | Transition phase begins, scheduled to run until at least 31 Aug 26. Exporters continue to sell independently and existing contracts are honoured, but all shipments must now be reported to DSI through the customs directorate's CEISA 4.0 digital platform. A parallel regulation requiring natural-resource export proceeds to be retained onshore takes effect the same day. |

| Early Jun 26 | Palm oil exporters reportedly cancel planned cargo shipments for fear of breaching the new rules and incurring penalties, while overseas buyers hold back pending compliance clarity. Industry groups warn that Indonesian palm oil export costs (already ~36% of export value vs ~6% in Malaysia) could rise further under a single-channel regime. |

| 11 Jun 26 | Government officials signal a scale-back: DSI will no longer become the sole exporter. Its role narrows to pricing oversight: Exporters keep their commercial relationships with buyers, but must justify declared prices, with values below market benchmarks subject to revision. DSI will charge only a 0.05-0.10% administrative fee to sustain operations. |

| 1 Jan 27 | The original target for full implementation of DSI's "single-window" export control system remains nominally on the books (1 Jan 27, or as early as Sep 26). |

Source: Government announcements, media reports, UOB Kay Hian

| Summary of PP No. 24/2026: Strategic Natural Resource Export Governance | |

| BUMN export | - Strategic natural resource commodities can only be exported by a designated BUMN Export. - The BUMN Export may act as owner or sole intermediary. - The BUMN Export can determine selling prices and charge a reasonable margin. |

| Commodities covered | - Coal, ferroalloy, palm oil (including CPO, RBD palm oil and RBD palm olein). - More commodities can be added later. |

| Transition timeline | - Exports through BUMN must be implemented no later than 31 Dec 26. - The government will evaluate implementation within three months after the regulation takes effect. - The deadline can be brought forward depending on the evaluation. |

| Possible exemptions | - Companies may be exempted if they have contracts or agreements with the government that include at least investment, divestment, and domestic processing or refining commitments. |

Source: Indonesian Ministry of State Secretariate, UOB Kay Hian

OVERWEIGHT (Maintained)

Analyst

IMPORTANT NOTICE - DISCLOSURES AND DISCLAIMERS

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/df64a6ea-7980-447c-ae9e-fd19b93257dc, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.