Overnight Markets

Today’s Must-Know News

US equities advanced Wednesday (S&P 500 +0.38%; Nasdaq Composite +0.62%; DJIA +0.29%) as June PPI unexpectedly fell 0.3% MoM, easing rate-hike concerns and pushing the 10-year Treasury yield 4.2 bps lower to 4.547%. Alphabet (GOOGL +3.17%); Meta (META +3.07%) lifted communication services (XLC +1.73%), while Energy (XLE -0.79%) & Utilities (XLU -1.03%) lagged. Buffett said he initiated Berkshire’s (BRK/B -0.56%) investment in Alphabet, not Greg Abel. Apple (AAPL +4.01%) received approval to launch Apple Intelligence in China using Alibaba (9988.HK +2.35%; BABA +4.78%) & Baidu (9888.HK +1.42%; BIDU +1.59%) technology and is reportedly exploring AI-chip acquisitions. Semicon (SOXX -2.23%) declined as MU -9.02%; SNDK -8.12%; SKHY -9.0% sold off ahead of CXMT’s USD 8.55 bn IPO on concerns that additional Chinese memory capacity would increase supply and pressure prices. ASML (ASML NA -0.41%) beat 2Q26 estimates and raised FY26 sales guidance to EUR 43–45 bn, but shares reversed early gains as elevated AI expectations left TSMC (2330.TT +0.83%; TSM -0.22%), reporting 2Q26 results later today, under pressure to show strong demand, tight advanced-chip and packaging capacity, higher capex and rising margins. J&J (JNJ -2.69%) raised FY26 guidance after 2Q26 sales increased 6.6% to USD 25.3 bn, although medtech weakness weighed on shares. PayPal (PYPL +17.2%) is reviewing options after Stripe and Advent offered USD 60.50 per share, a 28% premium, while SpaceX (SPCX -0.6%) briefly traded below its IPO price. META, XLE, RBK/B, 9988.HK, SOXX, TSM, & JNJ are our Core Recommendations; GOOGL, MU, SKHY are our Trading Buys.

Trader’s Corner (Details on Page 6-7)

Ticker | Name | Rec. | Support | Resistance |

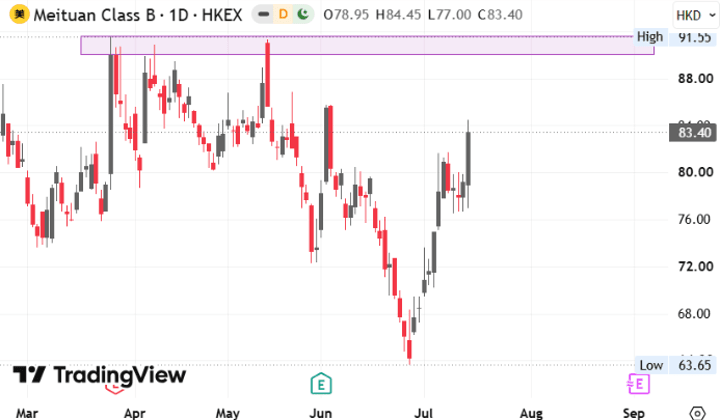

3690.HK | Meituan | - | HKD 76.65 / 70.20 | HKD 91.35 / 107.00 |

0001.HK | CK Hutchison | - | HKD 67.75 / 65.95 | HKD 80.15 / 86.00 |

CR = Core Recommendation; TB = Trading Buy

Hong Kong IPO Calendar

No upcoming IPOs.

Americas

Iran escalation keeps oil above USD 80. The US launched further strikes as Trump threatened to intensify attacks until Iran stops targeting Hormuz shipping. The front month WTI & Brent rose 0.3% each to USD 79.6/bbl & USD 84.95/bbl respectively. However, energy (XLE -0.79%) shares lagged Wednesday as investors bought communication services (XLC +1.73%) and Financial (XLF +0.68%) shares. Fed Chair Kevin Warsh said AI-related price increases may prove temporary rather than persistently inflationary. (Bloomberg)

Nvidia says Rubin is on track and expands with Toyota. Nvidia (NVDA +0.33%) denied reports of delays to its Vera Rubin systems and said production had started, while Toyota Motor (7203 JP +1.29%) will deploy Nvidia technology across smart cities, factories and vehicle-software development. (MarketWatch / Bloomberg) NVDA is our Core Recommendation.

CoreWeave weighs chip-price hedges. CoreWeave (CRWV -3.53%) is exploring derivatives to protect against a future decline in memory and storage-chip prices, though discussions remain preliminary and no hedges have been executed. Long-term supply deals with Micron (MU -9.02%) and SanDisk (SNDK -8.12%) include price floors, while new capacity from SK Hynix (SKHY -9.0%; 000660 KS +4.17%) and Micron is expected to ramp fully by early 2028. (Reuters) MU & SKHY are our Trading Buys.

Amazon expands satellites as AWS leadership changes. Amazon (AMZN +3.02%) said senior AWS executive Dave Brown will leave after 19 years and be replaced by Dave Treadwell on 1 August. Separately, Amazon Leo partnered with Herotel to launch satellite broadband in rural South Africa in 2027 (Reuters) AMZN is our Core Recommendation.

Microsoft sharpens its enterprise AI pitch. Microsoft (MSFT +2.78%) is training sales staff to challenge OpenAI and Anthropic by emphasising lower costs, stronger security controls and a more complete platform for deploying and monitoring AI. (Bloomberg) MSFT is our Core Recommendation.

Drug strength offsets J&J device weakness. Johnson & Johnson (JNJ -2.69%) beat 2Q estimates and raised its full-year sales and profit outlook as Darzalex and Tremfya drove pharmaceutical growth. Medical-device performance lagged as US demand for Impella heart pumps fell 2% following a UK study that raised concerns over some high-risk procedures. (Reuters) JNJ is our Core Recommendation.

Lilly nears a psychedelic-drug acquisition. Eli Lilly (LLY +0.35%) is in talks to acquire AtaiBeckley (ATAI -5.47%), which is developing treatments for resistant depression and social anxiety, with an announcement possible this week. (Bloomberg) LLY is our Core Recommendation.

Stripe-Advent bid sends PayPal higher. PayPal (PYPL +17.2%) received a USD 60.50-a-share offer from Stripe and Advent International, valuing the company at more than USD 53 bn and representing a 28% premium to Tuesday’s close. The proposal is backed by about USD 50 bn in financing and would give Stripe and Advent equal stakes, though no deal is certain. (Reuters)

Google defends overturned EU fine. Alphabet (GOOGL +3.17%) urged the EU’s top court to preserve a ruling that annulled a EUR 1.49 bn AdSense antitrust fine, with a non-binding opinion due on 12 November before a final judgment (Reuters) GOOGL is our Trading Buy.

Anthropic prepares for an October IPO. The Claude developer plans investor meetings in the coming weeks and is considering a listing as early as October, potentially ahead of OpenAI and DeepSeek. (Bloomberg)

Netflix faces an engagement test. Netflix (NFLX +0.2%) is expected to report 13.6% 2Q revenue growth to USD 12.59 bn, its slowest pace in more than four quarters, as weaker viewer retention and a slower-than-expected advertising ramp compound a decline of more than 20% in the stock this year (Reuters)

SpaceX slips near IPO price. SpaceX (SPCX -0.6%) closed at USD 135.27 after briefly falling below its USD 135 IPO price, well below last month’s peak that lifted its valuation above Microsoft (MSFT +2.78%) and Amazon (AMZN +3.02%). Analysts expect its first post-listing results in early August, while an upcoming lock-up expiry could add selling pressure. (Reuters) MSFT & AMZN are our Core Recommendations.

Palantir warns on Chinese AI and US resistance. Palantir (PLTR +0.03%) CTO Shyam Sankar alleged that Chinese developers used unauthorised model distillation and said domestic opposition to US data-centre construction poses an additional economic risk. (Bloomberg)

Trump pushes faster weapons production. President Trump urged defence contractors to expand capacity as US stockpiles tighten, supported by a USD 2.5 bn shipbuilding agreement with General Dynamics (GD -1.05%) and new manufacturing investments by Northrop Grumman (NOC -0.65%) and L3Harris (LHX -1.1%) to accelerate weapons production (Reuters)

Trading and deals lift Morgan Stanley. Morgan Stanley (MS +0.39%) beat 2Q profit estimates as equity net revenue jumped 69% and investment-banking revenue rose 58% to USD 2.44 bn, driving record group revenue. Wealth-management assets reached USD 10 tn, while the bank said AI-related capital spending could total USD 10 tn over several years. (Reuters)

ETF inflows lift BlackRock earnings. BlackRock (BLK +6.63%) reported 2Q adjusted EPS of USD 13.91, beating estimates, as net inflows reached USD 192 bn and assets under management rose to a record USD 15.34 tn. Its adjusted operating margin increased to 45.9%, the highest in almost five years. (Reuters)

Greater China

Hong Kong outperforms as China rotates. The CSI300 was down 0.2% Wednesday as weak 2Q GDP growth of 4.3% and profit-taking in chip stocks offset gains in traditional sectors. The HSI rose 1.4%, led by technology. (Reuters)

AI upcycle fuels CXMT IPO optimism. ChangXin Memory Technologies will open subscriptions for its USD 8.6 bn Shanghai IPO on Thursday ahead of a July 27 listing, with investors betting its valuation could rise sharply from RMB 579.18 bn. Demand is being supported by the AI memory upcycle and Beijing’s push for semiconductor self-reliance. (Reuters)

China clears Apple Intelligence rollout. Apple (AAPL +4.01%) received regulatory approval to launch Apple Intelligence in China using technology from Alibaba (9988.HK +2.35%; BABA +4.78%) and Baidu (9888.HK +1.42%; BIDU +1.59%), potentially strengthening its position against Huawei in the world’s largest smartphone market. (Bloomberg) 9988.HK is our Core Recommendation.

Tencent links Yuanbao to JD shopping. Tencent (0700.HK +3.9%) integrated Yuanbao with JD.com’s (9618.HK +1.67%; JD +1.53%) AI-agent mini-program ecosystem, allowing users to compare products, receive recommendations and access shopping links directly within conversations. The feature creates a seamless path from product enquiries to purchases. (AAStocks) 0700.HK is our Core Recommendation.

DeepSeek seeks fresh capital before IPO. DeepSeek plans to raise as much as RMB 50 bn at an approximately RMB 500 bn valuation and is considering a Shanghai STAR Market filing this year, weeks after completing a USD 7.4 bn fundraising round (Reuters)

AI demand drives another TSMC record. TSMC (2330.TT +0.83%; TSM -0.22%) is expected to report a 59% YoY rise in 2Q net profit to TWD 632.6 bn, or USD 19.65 bn, marking a fifth consecutive quarter of record earnings. Strong demand for advanced nodes and CoWoS packaging continues to outpace other foundries. (Reuters) TSM is our Core Recommendation.

Sinopec restructures around four businesses. Sinopec (0386.HK -1.19%) is reorganising into energy, finance, refining and supply-chain units to improve returns as Chinese fuel demand slows and petrochemical overcapacity weighs on margins; management said the overhaul is not intended to reduce headcount (Reuters)

Innolight nears major Hong Kong listing. Zhongji Innolight (300308.SZ -1.24%) is close to securing Chinese regulatory approval for a Hong Kong share sale that could raise about USD 7 bn, potentially one of the city’s largest listings in years. The Nvidia (NVDA +0.33%), Alphabet (GOOGL +3.17%) and Meta (META +3.07%) supplier has gained more than 90% this year, lifting its market value to RMB 1.3 tn. (Bloomberg) NVDA & META are our Core Recommendations; GOOGL is our Trading Buy.

China growth weakens as tariff risks approach. China’s second-quarter GDP growth slowed to 4.3%, below its 4.5–5.0% full-year target, as fixed-asset investment contracted 5.7% and retail sales rose only 1.0% in June despite export strength. Export front-loading partly reflected expectations that the current 10% US tariff, expiring on 24 July, could be replaced by higher levies, including a proposed 12.5% rate (Reuters)

China loan demand remains subdued. New yuan lending reached RMB 1.61 tn in June, below the RMB 2 tn consensus, while outstanding loan growth slowed to a record-low 5.2% as the property downturn and weak business investment restrained credit demand (Reuters)

Asia ex. China

Korea rate hike looms. The Bank of Korea was expected to raise its policy rate by 25 bps to 2.75% after stronger economic data and an AI-driven semiconductor boom strengthened the case for tighter policy. (Bloomberg)

DBS targets SGD 1 tn in wealth assets. DBS Group (DBS SP +1.32%) aims to increase wealth assets from SGD 632 bn in 2025 to more than SGD 1 tn by 2030 and plans to hire over 600 advisers and engineers by end-2028 (Reuters)

Fuel and Air India cap SIA earnings. Singapore Airlines (SIA SP -0.26%) is expected to post near-breakeven 1QFY27 earnings as high fuel costs and Air India losses offset broadly in-line June operating data. FY27 earnings are raised by 22% on lower Air India loss assumptions but maintained HOLD with a target price of SGD 6.76. (UOB Kay Hian Institutional Research)

EMEA and Others

Luxury rebound edges Europe higher. The Stoxx 600 rose 0.1% and France’s CAC 40 gained 0.19% on Wednesday, while Germany’s DAX and the UK’s FTSE 100 fell 0.59% and 0.13% repsectivelyas luxury strength offset weakness in telecom and technology shares. ASML (ASML NA -0.41%) declined despite raising its 2026 sales outlook, while US-Iran tensions kept sentiment cautious. (Reuters)

AI demand lifts ASML outlook. ASML (ASML NA -0.41%) raised its 2026 revenue forecast to EUR 43-45 bn after 2Q revenue rose to EUR 9.33 bn and net income reached EUR 2.92 bn, both above estimates. The firm plans to expand capacity by 30% in 2027-2028, while Intel (INTC -4.43%) will use its High-NA tools for selected Panther Lake chips. (Reuters)

Nokia and Nvidia advance AI-RAN platform. Nokia (NOK -3.85%) and Nvidia (NVDA +0.33%) are developing a commercial AI-powered radio access network platform designed to help operators carry twice as much data over existing spectrum by 2028. Nokia expects spectrum efficiency gains of about 50% when deployment begins next year, versus roughly 20% currently. (AAStocks) NVDA is our Core Recommendation; NOK is our Trading Buy.

Novo secures EU approval for Wegovy pill. Novo Nordisk (NVO +3.04%) won EU approval for the first oral GLP-1 weight-loss treatment, with trials showing average weight loss of about 17%; launches in additional markets are planned for the second half of 2026 (Reuters)

Kering appoints new Bottega Veneta chief. Kering (KER FP +3.64%) appointed LVMH fragrance executive Romain Spitzer as Bottega Veneta CEO from 1 September, filling a position vacant since March (Reuters)

Jewellery demand drives Richemont beat. Richemont (CFR SW +6.68%) reported 20% constant-currency sales growth to EUR 6.33 bn, above forecasts, as jewellery revenue jumped 24% and demand accelerated across Greater China and the Americas (Reuters)

TRADERS’ CORNER

Source: TradingView |

| Meituan (3690.HK)

|

Our Technical View

Price cleanly penetrated its recent swing high with a bullish candle, signalling an aggressive breakout that confirms expanding upward momentum.

The RSI rises constructively above its 50-neutral midline.

- Backed by this active demand, the technical layout projects sustained upward continuation toward the primary overhead resistance zone.

Source: TradingView |

| CK Hutchison (0001.HK)

|

Our Technical View

Price has executed a clean post-breakout retest and defence, keeping the bullish trend intact.

The RSI is scaling steadily above the 50 threshold to confirm dominant buy-side control.

A decisive penetration above the recent swing high will serve as the definitive execution trigger for a sustained extension into the next distribution zone.

Today’s Must-Know News

US equities advanced Wednesday (S&P 500 +0.38%; Nasdaq Composite +0.62%; DJIA +0.29%) as June PPI unexpectedly fell 0.3% MoM, easing rate-hike concerns and pushing the 10-year Treasury yield 4.2 bps lower to 4.547%. Alphabet (GOOGL +3.17%); Meta (META +3.07%) lifted communication services (XLC +1.73%), while Energy (XLE -0.79%) & Utilities (XLU -1.03%) lagged. Buffett said he initiated Berkshire’s (BRK/B -0.56%) investment in Alphabet, not Greg Abel. Apple (AAPL +4.01%) received approval to launch Apple Intelligence in China using Alibaba (9988.HK +2.35%; BABA +4.78%) & Baidu (9888.HK +1.42%; BIDU +1.59%) technology and is reportedly exploring AI-chip acquisitions. Semicon (SOXX -2.23%) declined as MU -9.02%; SNDK -8.12%; SKHY -9.0% sold off ahead of CXMT’s USD 8.55 bn IPO on concerns that additional Chinese memory capacity would increase supply and pressure prices. ASML (ASML NA -0.41%) beat 2Q26 estimates and raised FY26 sales guidance to EUR 43–45 bn, but shares reversed early gains as elevated AI expectations left TSMC (2330.TT +0.83%; TSM -0.22%), reporting 2Q26 results later today, under pressure to show strong demand, tight advanced-chip and packaging capacity, higher capex and rising margins. J&J (JNJ -2.69%) raised FY26 guidance after 2Q26 sales increased 6.6% to USD 25.3 bn, although medtech weakness weighed on shares. PayPal (PYPL +17.2%) is reviewing options after Stripe and Advent offered USD 60.50 per share, a 28% premium, while SpaceX (SPCX -0.6%) briefly traded below its IPO price. META, XLE, RBK/B, 9988.HK, SOXX, TSM, & JNJ are our Core Recommendations; GOOGL, MU, SKHY are our Trading Buys.

Trader’s Corner (Details on Page 6-7)

Ticker | Name | Rec. | Support | Resistance |

3690.HK | Meituan | - | HKD 76.65 / 70.20 | HKD 91.35 / 107.00 |

0001.HK | CK Hutchison | - | HKD 67.75 / 65.95 | HKD 80.15 / 86.00 |

CR = Core Recommendation; TB = Trading Buy

Hong Kong IPO Calendar

No upcoming IPOs.

Americas

Iran escalation keeps oil above USD 80. The US launched further strikes as Trump threatened to intensify attacks until Iran stops targeting Hormuz shipping. The front month WTI & Brent rose 0.3% each to USD 79.6/bbl & USD 84.95/bbl respectively. However, energy (XLE -0.79%) shares lagged Wednesday as investors bought communication services (XLC +1.73%) and Financial (XLF +0.68%) shares. Fed Chair Kevin Warsh said AI-related price increases may prove temporary rather than persistently inflationary. (Bloomberg)

Nvidia says Rubin is on track and expands with Toyota. Nvidia (NVDA +0.33%) denied reports of delays to its Vera Rubin systems and said production had started, while Toyota Motor (7203 JP +1.29%) will deploy Nvidia technology across smart cities, factories and vehicle-software development. (MarketWatch / Bloomberg) NVDA is our Core Recommendation.

CoreWeave weighs chip-price hedges. CoreWeave (CRWV -3.53%) is exploring derivatives to protect against a future decline in memory and storage-chip prices, though discussions remain preliminary and no hedges have been executed. Long-term supply deals with Micron (MU -9.02%) and SanDisk (SNDK -8.12%) include price floors, while new capacity from SK Hynix (SKHY -9.0%; 000660 KS +4.17%) and Micron is expected to ramp fully by early 2028. (Reuters) MU & SKHY are our Trading Buys.

Amazon expands satellites as AWS leadership changes. Amazon (AMZN +3.02%) said senior AWS executive Dave Brown will leave after 19 years and be replaced by Dave Treadwell on 1 August. Separately, Amazon Leo partnered with Herotel to launch satellite broadband in rural South Africa in 2027 (Reuters) AMZN is our Core Recommendation.

Microsoft sharpens its enterprise AI pitch. Microsoft (MSFT +2.78%) is training sales staff to challenge OpenAI and Anthropic by emphasising lower costs, stronger security controls and a more complete platform for deploying and monitoring AI. (Bloomberg) MSFT is our Core Recommendation.

Drug strength offsets J&J device weakness. Johnson & Johnson (JNJ -2.69%) beat 2Q estimates and raised its full-year sales and profit outlook as Darzalex and Tremfya drove pharmaceutical growth. Medical-device performance lagged as US demand for Impella heart pumps fell 2% following a UK study that raised concerns over some high-risk procedures. (Reuters) JNJ is our Core Recommendation.

Lilly nears a psychedelic-drug acquisition. Eli Lilly (LLY +0.35%) is in talks to acquire AtaiBeckley (ATAI -5.47%), which is developing treatments for resistant depression and social anxiety, with an announcement possible this week. (Bloomberg) LLY is our Core Recommendation.

Stripe-Advent bid sends PayPal higher. PayPal (PYPL +17.2%) received a USD 60.50-a-share offer from Stripe and Advent International, valuing the company at more than USD 53 bn and representing a 28% premium to Tuesday’s close. The proposal is backed by about USD 50 bn in financing and would give Stripe and Advent equal stakes, though no deal is certain. (Reuters)

Google defends overturned EU fine. Alphabet (GOOGL +3.17%) urged the EU’s top court to preserve a ruling that annulled a EUR 1.49 bn AdSense antitrust fine, with a non-binding opinion due on 12 November before a final judgment (Reuters) GOOGL is our Trading Buy.

Anthropic prepares for an October IPO. The Claude developer plans investor meetings in the coming weeks and is considering a listing as early as October, potentially ahead of OpenAI and DeepSeek. (Bloomberg)

Netflix faces an engagement test. Netflix (NFLX +0.2%) is expected to report 13.6% 2Q revenue growth to USD 12.59 bn, its slowest pace in more than four quarters, as weaker viewer retention and a slower-than-expected advertising ramp compound a decline of more than 20% in the stock this year (Reuters)

SpaceX slips near IPO price. SpaceX (SPCX -0.6%) closed at USD 135.27 after briefly falling below its USD 135 IPO price, well below last month’s peak that lifted its valuation above Microsoft (MSFT +2.78%) and Amazon (AMZN +3.02%). Analysts expect its first post-listing results in early August, while an upcoming lock-up expiry could add selling pressure. (Reuters) MSFT & AMZN are our Core Recommendations.

Palantir warns on Chinese AI and US resistance. Palantir (PLTR +0.03%) CTO Shyam Sankar alleged that Chinese developers used unauthorised model distillation and said domestic opposition to US data-centre construction poses an additional economic risk. (Bloomberg)

Trump pushes faster weapons production. President Trump urged defence contractors to expand capacity as US stockpiles tighten, supported by a USD 2.5 bn shipbuilding agreement with General Dynamics (GD -1.05%) and new manufacturing investments by Northrop Grumman (NOC -0.65%) and L3Harris (LHX -1.1%) to accelerate weapons production (Reuters)

Trading and deals lift Morgan Stanley. Morgan Stanley (MS +0.39%) beat 2Q profit estimates as equity net revenue jumped 69% and investment-banking revenue rose 58% to USD 2.44 bn, driving record group revenue. Wealth-management assets reached USD 10 tn, while the bank said AI-related capital spending could total USD 10 tn over several years. (Reuters)

ETF inflows lift BlackRock earnings. BlackRock (BLK +6.63%) reported 2Q adjusted EPS of USD 13.91, beating estimates, as net inflows reached USD 192 bn and assets under management rose to a record USD 15.34 tn. Its adjusted operating margin increased to 45.9%, the highest in almost five years. (Reuters)

Greater China

Hong Kong outperforms as China rotates. The CSI300 was down 0.2% Wednesday as weak 2Q GDP growth of 4.3% and profit-taking in chip stocks offset gains in traditional sectors. The HSI rose 1.4%, led by technology. (Reuters)

AI upcycle fuels CXMT IPO optimism. ChangXin Memory Technologies will open subscriptions for its USD 8.6 bn Shanghai IPO on Thursday ahead of a July 27 listing, with investors betting its valuation could rise sharply from RMB 579.18 bn. Demand is being supported by the AI memory upcycle and Beijing’s push for semiconductor self-reliance. (Reuters)

China clears Apple Intelligence rollout. Apple (AAPL +4.01%) received regulatory approval to launch Apple Intelligence in China using technology from Alibaba (9988.HK +2.35%; BABA +4.78%) and Baidu (9888.HK +1.42%; BIDU +1.59%), potentially strengthening its position against Huawei in the world’s largest smartphone market. (Bloomberg) 9988.HK is our Core Recommendation.

Tencent links Yuanbao to JD shopping. Tencent (0700.HK +3.9%) integrated Yuanbao with JD.com’s (9618.HK +1.67%; JD +1.53%) AI-agent mini-program ecosystem, allowing users to compare products, receive recommendations and access shopping links directly within conversations. The feature creates a seamless path from product enquiries to purchases. (AAStocks) 0700.HK is our Core Recommendation.

DeepSeek seeks fresh capital before IPO. DeepSeek plans to raise as much as RMB 50 bn at an approximately RMB 500 bn valuation and is considering a Shanghai STAR Market filing this year, weeks after completing a USD 7.4 bn fundraising round (Reuters)

AI demand drives another TSMC record. TSMC (2330.TT +0.83%; TSM -0.22%) is expected to report a 59% YoY rise in 2Q net profit to TWD 632.6 bn, or USD 19.65 bn, marking a fifth consecutive quarter of record earnings. Strong demand for advanced nodes and CoWoS packaging continues to outpace other foundries. (Reuters) TSM is our Core Recommendation.

Sinopec restructures around four businesses. Sinopec (0386.HK -1.19%) is reorganising into energy, finance, refining and supply-chain units to improve returns as Chinese fuel demand slows and petrochemical overcapacity weighs on margins; management said the overhaul is not intended to reduce headcount (Reuters)

Innolight nears major Hong Kong listing. Zhongji Innolight (300308.SZ -1.24%) is close to securing Chinese regulatory approval for a Hong Kong share sale that could raise about USD 7 bn, potentially one of the city’s largest listings in years. The Nvidia (NVDA +0.33%), Alphabet (GOOGL +3.17%) and Meta (META +3.07%) supplier has gained more than 90% this year, lifting its market value to RMB 1.3 tn. (Bloomberg) NVDA & META are our Core Recommendations; GOOGL is our Trading Buy.

China growth weakens as tariff risks approach. China’s second-quarter GDP growth slowed to 4.3%, below its 4.5–5.0% full-year target, as fixed-asset investment contracted 5.7% and retail sales rose only 1.0% in June despite export strength. Export front-loading partly reflected expectations that the current 10% US tariff, expiring on 24 July, could be replaced by higher levies, including a proposed 12.5% rate (Reuters)

China loan demand remains subdued. New yuan lending reached RMB 1.61 tn in June, below the RMB 2 tn consensus, while outstanding loan growth slowed to a record-low 5.2% as the property downturn and weak business investment restrained credit demand (Reuters)

Asia ex. China

Korea rate hike looms. The Bank of Korea was expected to raise its policy rate by 25 bps to 2.75% after stronger economic data and an AI-driven semiconductor boom strengthened the case for tighter policy. (Bloomberg)

DBS targets SGD 1 tn in wealth assets. DBS Group (DBS SP +1.32%) aims to increase wealth assets from SGD 632 bn in 2025 to more than SGD 1 tn by 2030 and plans to hire over 600 advisers and engineers by end-2028 (Reuters)

Fuel and Air India cap SIA earnings. Singapore Airlines (SIA SP -0.26%) is expected to post near-breakeven 1QFY27 earnings as high fuel costs and Air India losses offset broadly in-line June operating data. FY27 earnings are raised by 22% on lower Air India loss assumptions but maintained HOLD with a target price of SGD 6.76. (UOB Kay Hian Institutional Research)

EMEA and Others

Luxury rebound edges Europe higher. The Stoxx 600 rose 0.1% and France’s CAC 40 gained 0.19% on Wednesday, while Germany’s DAX and the UK’s FTSE 100 fell 0.59% and 0.13% repsectivelyas luxury strength offset weakness in telecom and technology shares. ASML (ASML NA -0.41%) declined despite raising its 2026 sales outlook, while US-Iran tensions kept sentiment cautious. (Reuters)

AI demand lifts ASML outlook. ASML (ASML NA -0.41%) raised its 2026 revenue forecast to EUR 43-45 bn after 2Q revenue rose to EUR 9.33 bn and net income reached EUR 2.92 bn, both above estimates. The firm plans to expand capacity by 30% in 2027-2028, while Intel (INTC -4.43%) will use its High-NA tools for selected Panther Lake chips. (Reuters)

Nokia and Nvidia advance AI-RAN platform. Nokia (NOK -3.85%) and Nvidia (NVDA +0.33%) are developing a commercial AI-powered radio access network platform designed to help operators carry twice as much data over existing spectrum by 2028. Nokia expects spectrum efficiency gains of about 50% when deployment begins next year, versus roughly 20% currently. (AAStocks) NVDA is our Core Recommendation; NOK is our Trading Buy.

Novo secures EU approval for Wegovy pill. Novo Nordisk (NVO +3.04%) won EU approval for the first oral GLP-1 weight-loss treatment, with trials showing average weight loss of about 17%; launches in additional markets are planned for the second half of 2026 (Reuters)

Kering appoints new Bottega Veneta chief. Kering (KER FP +3.64%) appointed LVMH fragrance executive Romain Spitzer as Bottega Veneta CEO from 1 September, filling a position vacant since March (Reuters)

Jewellery demand drives Richemont beat. Richemont (CFR SW +6.68%) reported 20% constant-currency sales growth to EUR 6.33 bn, above forecasts, as jewellery revenue jumped 24% and demand accelerated across Greater China and the Americas (Reuters)

TRADERS’ CORNER

Source: TradingView |

| Meituan (3690.HK)

|

Our Technical View

Price cleanly penetrated its recent swing high with a bullish candle, signalling an aggressive breakout that confirms expanding upward momentum.

The RSI rises constructively above its 50-neutral midline.

- Backed by this active demand, the technical layout projects sustained upward continuation toward the primary overhead resistance zone.

Source: TradingView |

| CK Hutchison (0001.HK)

|

Our Technical View

Price has executed a clean post-breakout retest and defence, keeping the bullish trend intact.

The RSI is scaling steadily above the 50 threshold to confirm dominant buy-side control.

A decisive penetration above the recent swing high will serve as the definitive execution trigger for a sustained extension into the next distribution zone.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.