Overnight Markets

Today’s Must-Know News

- Chip & memory makers lead AI-driven selloff Tuesday. S&P 500 fell 1.44% & edged towards its 50-day SMA. Tech (QQQ -3.29%) underperformed, while Semis (SOXX -7.88%) plunged. Micron (MU -13.18%) sank ahead of 3QFY26 earnings after-market later today. Samsung (005930 KS -12.9%) & SK Hynix (000660 KS -13.18%) also recorded steep declines. SpaceX (SPCX +0.98%) rebounded after attracting about USD 89 bn in demand for its first US bond sale, ending a three-day selloff that had erased over USD 600 bn in market value. SOXX & MU are our Trading Buys.

- Alphabet joins DJIA. Alphabet (GOOGL -1.02%) rose 1.0% after-market Tuesday following news that it will replace Verizon (VZ +3.02%) in the DJIA (INDU -0.09%) effective prior to the opening of trading on June 29. VZ fell 0.4% after-market. GOOGL is our Trading Buy.

- Qualcomm pivots to AI beyond phones. Qualcomm (QCOM -8.01%) is expected at its Investor Day later today to outline expansion into data centre, automotive and IoT AI workloads, with investor focus on hyperscaler pipeline and design wins. QCOM is our Trading Buy.

- Alibaba leads pushback on Pentagon blacklist. Alibaba (BABA -2.26%; 9988.HK -3.84%) is challenging its US Pentagon blacklist in court, calling the designation unfounded & unlawful. 9988.HK is our Core Recommendation.

| Trader's Corner (Details on Page 6-7) | ||||

| Ticker | Name | Rec. | Support Levels | Resistance Levels |

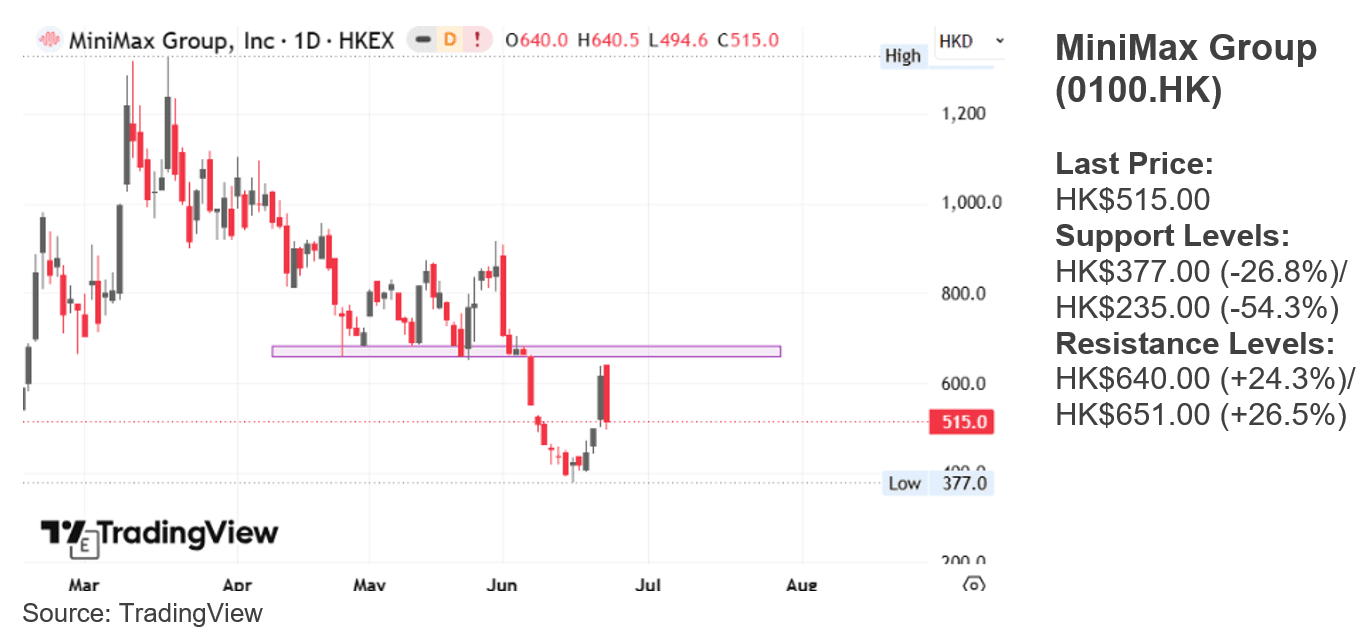

| 0100.HK | MiniMax | - | HK$377.00/$235.00 | HK$640.00/$651.00 |

| 9880.HK | Ubtech Robotics | - | HK$84.60/$75.90 | HK$110.70/$114.50 |

| CR = Core Recommendation; TB = Trading Buy | ||||

| Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 1688.HK | Lingyi iTech | Technology | Jun 26 |

| 1956.HK | Wenge AI | Technology | Jun 26 |

| 2272.HK | Keytop Parking | Discretionary | Jun 26 |

| 3661.HK | SG Micro | Discretionary | Jun 26 |

| 6228.HK | Merdekagold-DRS | Materials | Jun 26 |

| 9630.HK | CFMEE | Technology | Jun 26 |

| 1191.HK | Crealights | Technology | Jun 29 |

| 2672.HK | Baige Digital | Technology | Jun 29 |

| 9637.HK | Alebund-B | Healthcare | Jun 29 |

| 2697.HK | TH Medical-B | Healthcare | Jun 30 |

| 3952.HK | Laifual | Industrials | Jun 30 |

| 6715.HK | XunLong Scitech | Consumer Staples | Jun 30 |

| 6915.HK | Jiangxi Bio | Healthcare | Jun 30 |

| 0668.HK | Anker | Technology | Jul 2 |

Americas

- Quantum stocks surge on US policy push. Quantum names including IonQ (IONQ -0.81%), Rigetti (RGTI -0.47%) and D-Wave (QBTS +2.29%) rallied after Trump signed executive orders aimed at accelerating quantum adoption and cyber capabilities, driving expectations of stronger federal support and procurement. The move also lifted broader sentiment across the ecosystem, with IBM (IBM +5.04%) highlighted for its USD 10 bn+ quantum investment commitment. (Bloomberg)

- Drug pricing pressure hits Eli Lilly rollout. Eli Lilly (LLY +0.45%) said Trump administration “most-favoured-nation” drug pricing policy could complicate European reimbursement talks and influence its obesity drug launch strategy in Europe. LLY still targets rollout from 2H 2026 to early 2027 via telehealth and direct-to-patient channels but expects greater reliance on out-of-pocket payments, highlighting pricing friction across US and global pharma markets (Bloomberg). LLY is our Core Recommendation.

- Walmart expands ad push with Vibe.co deal. Walmart (WMT +1.91%) is acquiring French ad-tech firm Vibe.co for about USD 1.4 bn, marking a major step in its push to grow advertising revenue and compete with Amazon (AMZN +0.57%) in digital ads. The deal includes USD 1.2 bn in cash and about USD 180 mn in retention-linked payments for executives, and builds on Walmart's earlier acquisition of Vizio. (WSJ) WMT & AMZN are our Core Recommendations.

- Gold drops as Fed hike bets rise. Gold (XAU -1.74%) fell Tuesday to USD4,117.19/oz as a stronger US dollar and rising Fed hike expectations weighed. Markets are now pricing a higher probability of at least one rate hike by July, with CME FedWatch showing odds rising to 37.4% from 8.5% a week earlier (Reuters)

- Nike appoints Pfizer executive as CFO. Nike (NKE -1.88%) rose 0.6% after-market Tuesday on news of an upcoming leadership transition and an unexpected financial uplift. The firm named Pfizer (PFE -1.44%) veteran David M. Denton as its new CFO and flagged a favourable boost to 4Q results from tariff refunds. (investing.com)

- FedEx beats, flags trade and cost pressure. FedEx (FDX -3.51%) sank 6.6% after-market Tuesday following a FY2027 outlook that came in well below expectations. The firm guided adjusted FY27 EPS of USD16.90–18.10 versus a USD19.86 consensus, overshadowing an otherwise solid quarterly beat for 4QFY26 and warned that tariff-driven trade uncertainty and cost inflation continue to weigh on its express network. (Bloomberg / Investing.com)

- Honeywell aerospace spin-off surged on index inclusion. Honeywell Aerospace (HONAV -6.14%) jumped > 6% after-market Tuesday after S&P Dow Jones Indices confirmed it will be added to both the S&P 100 and S&P 500 effective at the June 29 market open, replacing Honeywell International (HON -2.52%) and Conagra Brands (CAG +4.51%) as part of a broader index reshuffle. (Investing.com)

- Merger hopes offset Tesla concerns. Tesla (TSLA -5.79%) fell Tuesday despite growing speculation that Elon Musk could eventually merge the EV maker with SpaceX (SPCX +0.98%), with some analysts assigning more than an 80% probability to a deal next year. (Bloomberg)

- Meta pushes down-market in smart glasses. Meta (META -0.29%) is launching first own-brand smart glasses at USD299 alongside a USD399 model, expanding beyond its Ray-Ban partnership to scale AI wearables, while also remaining the only major US AI developer yet to join the voluntary AI safety review framework but signalling intent to do so. (Bloomberg) META is our Core Recommendation.

- Amazon ordered to bargain with union in US labour dispute. Amazon (AMZN +0.57%) has been directed by a US National Labor Relations Board judge to negotiate with a Teamsters-backed group representing about 120 warehouse workers in San Francisco. That came after findings the firm failed to properly recognise majority support under a 2023 union recognition framework (Reuters) AMZN is our Core Recommendation.

- Nvidia hit with AI copyright lawsuit. Nvidia (NVDA -4.13%) has been sued by Jamendo, alleging unauthorized use of hundreds of thousands of music files and metadata to train AI models including Fugatto and Audio Flamingo, intensifying legal scrutiny over AI training data. The Luxembourg-based platform is seeking damages of up to USD 150,000 per infringement. (Reuters) NVDA is our Core Recommendation.

- UK clears Apple iCloud lawsuit. Apple (AAPL -0.91%) faces a GBP 3 bn (USD 4 bn) UK class action after a tribunal approved claims that the firm used its market position to favour iCloud over rival cloud-storage providers. The case covers nearly 40 mn UK users from 2018 to 2026, with potential compensation of up to GBP77 per person if successful. Apple disputes the allegations and a trial is expected in 2028 (Reuters)

- Private credit liquidity strain at Morgan Stanley fund. Morgan Stanley (MS -0.47%) has tightened withdrawals from its USD7bn North Haven Private Income Fund after investors sought to redeem about 11.6% of units, with only 43% of 2Q requests to be met. (Reuters)

- Anthropic launches AI agent for Slack. Anthropic on Tuesday launched Claude Tag, an AI agent integrated into Salesforce's (CRM +2.2%) Slack that can join group chats, analyze conversations and assist employees with tasks. The tool is in beta for Claude Enterprise and Claude Team customers on Slack, with expansion to other platforms planned in the coming weeks. (Reuters)

Greater China

- China, Hong Kong stocks retreat. Mainland China and Hong Kong shares fell on Tuesday as rising bets of a Federal Reserve rate hike and uncertainty over US-Iran talks weighed on sentiment. CSI 300 Index lost 2.77%, while HSI fell 1.82%. (Reuters)

- China urged to rebalance economic growth. A policy adviser to PBOC warned that unbalanced economic growth could threaten long-term sustainability and said policymakers should focus on raising household incomes and confidence through stronger social security support to boost consumption. The adviser added that continued measures supporting consumers and improving wealth effects from housing or equity markets could help underpin spending. (Bloomberg)

- Tencent reviews Japanese game stakes. Tencent (0700.HK -4.2%) is considering selling stakes in several Japanese game studios, including Marvelous (7844.JP -2.29%), as part of a global portfolio review. The firm said it remains committed to Japan's gaming market and will continue supporting its investee companies. (Reuters) 0700.HK is our Core Recommendation.

- CATL unveils sodium battery storage system. CATL (688411.SZ +8.68%) launched its TENER sodium battery energy storage system, with initial deliveries in China set for September and global shipments starting in June 2027, as it expands beyond lithium technology. The firm said it aims to boost sodium battery capacity to meet rising energy storage demand from data centers under its dual-track battery strategy. (Bloomberg)

- Momenta targets Hong Kong IPO launch. Chinese autonomous driving developer Momenta plans to launch its Hong Kong initial public offering as early as next Monday. The firm could raise about USD 0.9 bn from the offering, with pricing tentatively scheduled for July 3 and trading set to begin on July 8. (Reuters)

- China Resources New Energy IPO sees strong demand. China Resources New Energy (001248.SZ) attracted about RMB 6.4 tn in bids from retail investors for its Shenzhen IPO, with demand for the public tranche exceeding 1,000 times the shares initially offered. The China Resources Power (0836.HK -0.05%) unit is set to raise up to RMB 24.5 bn, potentially making it Shenzhen's largest IPO on record. (Reuters)

- Doubao nears launch of new model. ByteDance's Doubao is set to officially release its new video generation model, Seedance 2.5, in early July after completing final internal testing. The model is said to support video generation of up to 30 seconds, accept up to 50 multimodal reference materials and offer enhanced editing controls to improve creators' efficiency and output quality. (AAStocks)

- ByteDance doubles down on AI. ByteDance CEO Liang Rubo said the firm's key priority is strengthening large model capabilities as it sharpens its focus on artificial intelligence. Speaking at the Volcengine Force Conference, Liang said Volcengine's MaaS business has been elevated to a core business segment and will continue to receive long-term investment. (AAStocks)

Asia ex. China

- SK Hynix ETF becomes Hong Kong's largest. A leveraged ETF linked to SK Hynix (000660 KS -13.18%) managed by CSOP Asset Management has grown to more than USD 16.8 bn in assets under management, surpassing the Tracker Fund to become Hong Kong's largest ETF. The rapid asset growth highlights strong investor demand for leveraged semiconductor exposure. (Reuters)

- Nissan halts electric Qashqai development. Nissan (7201 JP -3.84%) has stopped development of a fully electric version of its top-selling Qashqai model in Europe as part of its global restructuring and cost-cutting efforts. The move could leave the Japanese automaker trailing rivals in a key market segment as European and Chinese competitors expand their affordable EV offerings. (Reuters)

EMEA and Others

- European shares open lower. European shares fell on Tuesday as expectations of imminent Federal Reserve rate hikes and concerns over rising corporate spending on AI weighed on sentiment. STOXX 600 index declined 0.73%, while Germany's DAX, France's CAC 40, and London’s FTSE 100 slipped 0.98%, 0.71%, and 0.09% respectively. Technology stocks were among the biggest drags as higher borrowing costs raised concerns over debt-funded investment. (Reuters)

- Ferrari names former BMW executive CMO. Ferrari (RACE IM -1.47%) appointed former BMW (BMW GR -0.16%) Italy chief Massimiliano Di Silvestre as chief marketing and commercial officer, replacing long-serving executive Enrico Galliera. Di Silvestre will join Ferrari on July 1 and report directly to CEO Benedetto Vigna. (Reuters)

- Heineken appoints JDE Peet's CEO. Heineken (HEIN NA +2.2%) named JDE Peet's (JDE GR +0.19%) CEO Rafael Oliveira as its new chair and CEO, marking the first time the Dutch brewer has appointed an outsider to the top role. Oliveira will join Heineken on October 1 for a four-year term as the firm seeks to accelerate its 2030 strategy and revive growth. (Reuters)

TRADERS’ CORNER

Source: TradingView | HBM (2142.HK)

Last Price: HK$11.22 Support Levels: HK$10.06 (-10.3%)/ HK$9.46 (-15.7%) Resistance Levels: HK$13.68 (+21.9%)/ HK$14.98 (+33.5%) |

Our Technical View

- Price was rejected at its support-turned-resistance zone, which is punctuated by a bearish engulfing candlestick pattern.

- This structural failure is heavily validated by a deteriorating momentum profile, with the MACD firmly entrenched in a negative regime and primed to execute a fresh bearish crossover.

- This confluence of overhead supply and expanding selling velocity strongly favours a continuation of the broader primary downtrend.

Source: TradingView | Sunny Optical (2382.HK)

Last Price: HK$79.55 Support Levels: HK$73.80 (-7.2%)/ HK$69.80 (-12.3%) Resistance Levels: HK$86.30 (+8.5%)/ HK$90.05 (+13.2%) |

Our Technical View

- Price was capped at its support-turned-resistance zone, and subsequently broke down to violate its recent structural low.

- This technical weakness is reinforced by the MACD which has turned bearish and is expanding lower within a negative regime.

- This combination of an established overhead supply ceiling and accelerating downward velocity significantly increases the probability of a sustained extension lower.

Today’s Must-Know News

- Chip & memory makers lead AI-driven selloff Tuesday. S&P 500 fell 1.44% & edged towards its 50-day SMA. Tech (QQQ -3.29%) underperformed, while Semis (SOXX -7.88%) plunged. Micron (MU -13.18%) sank ahead of 3QFY26 earnings after-market later today. Samsung (005930 KS -12.9%) & SK Hynix (000660 KS -13.18%) also recorded steep declines. SpaceX (SPCX +0.98%) rebounded after attracting about USD 89 bn in demand for its first US bond sale, ending a three-day selloff that had erased over USD 600 bn in market value. SOXX & MU are our Trading Buys.

- Alphabet joins DJIA. Alphabet (GOOGL -1.02%) rose 1.0% after-market Tuesday following news that it will replace Verizon (VZ +3.02%) in the DJIA (INDU -0.09%) effective prior to the opening of trading on June 29. VZ fell 0.4% after-market. GOOGL is our Trading Buy.

- Qualcomm pivots to AI beyond phones. Qualcomm (QCOM -8.01%) is expected at its Investor Day later today to outline expansion into data centre, automotive and IoT AI workloads, with investor focus on hyperscaler pipeline and design wins. QCOM is our Trading Buy.

- Alibaba leads pushback on Pentagon blacklist. Alibaba (BABA -2.26%; 9988.HK -3.84%) is challenging its US Pentagon blacklist in court, calling the designation unfounded & unlawful. 9988.HK is our Core Recommendation.

| Trader's Corner (Details on Page 6-7) | ||||

| Ticker | Name | Rec. | Support Levels | Resistance Levels |

| 0100.HK | MiniMax | - | HK$377.00/$235.00 | HK$640.00/$651.00 |

| 9880.HK | Ubtech Robotics | - | HK$84.60/$75.90 | HK$110.70/$114.50 |

| CR = Core Recommendation; TB = Trading Buy | ||||

| Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 1688.HK | Lingyi iTech | Technology | Jun 26 |

| 1956.HK | Wenge AI | Technology | Jun 26 |

| 2272.HK | Keytop Parking | Discretionary | Jun 26 |

| 3661.HK | SG Micro | Discretionary | Jun 26 |

| 6228.HK | Merdekagold-DRS | Materials | Jun 26 |

| 9630.HK | CFMEE | Technology | Jun 26 |

| 1191.HK | Crealights | Technology | Jun 29 |

| 2672.HK | Baige Digital | Technology | Jun 29 |

| 9637.HK | Alebund-B | Healthcare | Jun 29 |

| 2697.HK | TH Medical-B | Healthcare | Jun 30 |

| 3952.HK | Laifual | Industrials | Jun 30 |

| 6715.HK | XunLong Scitech | Consumer Staples | Jun 30 |

| 6915.HK | Jiangxi Bio | Healthcare | Jun 30 |

| 0668.HK | Anker | Technology | Jul 2 |

Americas

- Quantum stocks surge on US policy push. Quantum names including IonQ (IONQ -0.81%), Rigetti (RGTI -0.47%) and D-Wave (QBTS +2.29%) rallied after Trump signed executive orders aimed at accelerating quantum adoption and cyber capabilities, driving expectations of stronger federal support and procurement. The move also lifted broader sentiment across the ecosystem, with IBM (IBM +5.04%) highlighted for its USD 10 bn+ quantum investment commitment. (Bloomberg)

- Drug pricing pressure hits Eli Lilly rollout. Eli Lilly (LLY +0.45%) said Trump administration “most-favoured-nation” drug pricing policy could complicate European reimbursement talks and influence its obesity drug launch strategy in Europe. LLY still targets rollout from 2H 2026 to early 2027 via telehealth and direct-to-patient channels but expects greater reliance on out-of-pocket payments, highlighting pricing friction across US and global pharma markets (Bloomberg). LLY is our Core Recommendation.

- Walmart expands ad push with Vibe.co deal. Walmart (WMT +1.91%) is acquiring French ad-tech firm Vibe.co for about USD 1.4 bn, marking a major step in its push to grow advertising revenue and compete with Amazon (AMZN +0.57%) in digital ads. The deal includes USD 1.2 bn in cash and about USD 180 mn in retention-linked payments for executives, and builds on Walmart's earlier acquisition of Vizio. (WSJ) WMT & AMZN are our Core Recommendations.

- Gold drops as Fed hike bets rise. Gold (XAU -1.74%) fell Tuesday to USD4,117.19/oz as a stronger US dollar and rising Fed hike expectations weighed. Markets are now pricing a higher probability of at least one rate hike by July, with CME FedWatch showing odds rising to 37.4% from 8.5% a week earlier (Reuters)

- Nike appoints Pfizer executive as CFO. Nike (NKE -1.88%) rose 0.6% after-market Tuesday on news of an upcoming leadership transition and an unexpected financial uplift. The firm named Pfizer (PFE -1.44%) veteran David M. Denton as its new CFO and flagged a favourable boost to 4Q results from tariff refunds. (investing.com)

- FedEx beats, flags trade and cost pressure. FedEx (FDX -3.51%) sank 6.6% after-market Tuesday following a FY2027 outlook that came in well below expectations. The firm guided adjusted FY27 EPS of USD16.90–18.10 versus a USD19.86 consensus, overshadowing an otherwise solid quarterly beat for 4QFY26 and warned that tariff-driven trade uncertainty and cost inflation continue to weigh on its express network. (Bloomberg / Investing.com)

- Honeywell aerospace spin-off surged on index inclusion. Honeywell Aerospace (HONAV -6.14%) jumped > 6% after-market Tuesday after S&P Dow Jones Indices confirmed it will be added to both the S&P 100 and S&P 500 effective at the June 29 market open, replacing Honeywell International (HON -2.52%) and Conagra Brands (CAG +4.51%) as part of a broader index reshuffle. (Investing.com)

- Merger hopes offset Tesla concerns. Tesla (TSLA -5.79%) fell Tuesday despite growing speculation that Elon Musk could eventually merge the EV maker with SpaceX (SPCX +0.98%), with some analysts assigning more than an 80% probability to a deal next year. (Bloomberg)

- Meta pushes down-market in smart glasses. Meta (META -0.29%) is launching first own-brand smart glasses at USD299 alongside a USD399 model, expanding beyond its Ray-Ban partnership to scale AI wearables, while also remaining the only major US AI developer yet to join the voluntary AI safety review framework but signalling intent to do so. (Bloomberg) META is our Core Recommendation.

- Amazon ordered to bargain with union in US labour dispute. Amazon (AMZN +0.57%) has been directed by a US National Labor Relations Board judge to negotiate with a Teamsters-backed group representing about 120 warehouse workers in San Francisco. That came after findings the firm failed to properly recognise majority support under a 2023 union recognition framework (Reuters) AMZN is our Core Recommendation.

- Nvidia hit with AI copyright lawsuit. Nvidia (NVDA -4.13%) has been sued by Jamendo, alleging unauthorized use of hundreds of thousands of music files and metadata to train AI models including Fugatto and Audio Flamingo, intensifying legal scrutiny over AI training data. The Luxembourg-based platform is seeking damages of up to USD 150,000 per infringement. (Reuters) NVDA is our Core Recommendation.

- UK clears Apple iCloud lawsuit. Apple (AAPL -0.91%) faces a GBP 3 bn (USD 4 bn) UK class action after a tribunal approved claims that the firm used its market position to favour iCloud over rival cloud-storage providers. The case covers nearly 40 mn UK users from 2018 to 2026, with potential compensation of up to GBP77 per person if successful. Apple disputes the allegations and a trial is expected in 2028 (Reuters)

- Private credit liquidity strain at Morgan Stanley fund. Morgan Stanley (MS -0.47%) has tightened withdrawals from its USD7bn North Haven Private Income Fund after investors sought to redeem about 11.6% of units, with only 43% of 2Q requests to be met. (Reuters)

- Anthropic launches AI agent for Slack. Anthropic on Tuesday launched Claude Tag, an AI agent integrated into Salesforce's (CRM +2.2%) Slack that can join group chats, analyze conversations and assist employees with tasks. The tool is in beta for Claude Enterprise and Claude Team customers on Slack, with expansion to other platforms planned in the coming weeks. (Reuters)

Greater China

- China, Hong Kong stocks retreat. Mainland China and Hong Kong shares fell on Tuesday as rising bets of a Federal Reserve rate hike and uncertainty over US-Iran talks weighed on sentiment. CSI 300 Index lost 2.77%, while HSI fell 1.82%. (Reuters)

- China urged to rebalance economic growth. A policy adviser to PBOC warned that unbalanced economic growth could threaten long-term sustainability and said policymakers should focus on raising household incomes and confidence through stronger social security support to boost consumption. The adviser added that continued measures supporting consumers and improving wealth effects from housing or equity markets could help underpin spending. (Bloomberg)

- Tencent reviews Japanese game stakes. Tencent (0700.HK -4.2%) is considering selling stakes in several Japanese game studios, including Marvelous (7844.JP -2.29%), as part of a global portfolio review. The firm said it remains committed to Japan's gaming market and will continue supporting its investee companies. (Reuters) 0700.HK is our Core Recommendation.

- CATL unveils sodium battery storage system. CATL (688411.SZ +8.68%) launched its TENER sodium battery energy storage system, with initial deliveries in China set for September and global shipments starting in June 2027, as it expands beyond lithium technology. The firm said it aims to boost sodium battery capacity to meet rising energy storage demand from data centers under its dual-track battery strategy. (Bloomberg)

- Momenta targets Hong Kong IPO launch. Chinese autonomous driving developer Momenta plans to launch its Hong Kong initial public offering as early as next Monday. The firm could raise about USD 0.9 bn from the offering, with pricing tentatively scheduled for July 3 and trading set to begin on July 8. (Reuters)

- China Resources New Energy IPO sees strong demand. China Resources New Energy (001248.SZ) attracted about RMB 6.4 tn in bids from retail investors for its Shenzhen IPO, with demand for the public tranche exceeding 1,000 times the shares initially offered. The China Resources Power (0836.HK -0.05%) unit is set to raise up to RMB 24.5 bn, potentially making it Shenzhen's largest IPO on record. (Reuters)

- Doubao nears launch of new model. ByteDance's Doubao is set to officially release its new video generation model, Seedance 2.5, in early July after completing final internal testing. The model is said to support video generation of up to 30 seconds, accept up to 50 multimodal reference materials and offer enhanced editing controls to improve creators' efficiency and output quality. (AAStocks)

- ByteDance doubles down on AI. ByteDance CEO Liang Rubo said the firm's key priority is strengthening large model capabilities as it sharpens its focus on artificial intelligence. Speaking at the Volcengine Force Conference, Liang said Volcengine's MaaS business has been elevated to a core business segment and will continue to receive long-term investment. (AAStocks)

Asia ex. China

- SK Hynix ETF becomes Hong Kong's largest. A leveraged ETF linked to SK Hynix (000660 KS -13.18%) managed by CSOP Asset Management has grown to more than USD 16.8 bn in assets under management, surpassing the Tracker Fund to become Hong Kong's largest ETF. The rapid asset growth highlights strong investor demand for leveraged semiconductor exposure. (Reuters)

- Nissan halts electric Qashqai development. Nissan (7201 JP -3.84%) has stopped development of a fully electric version of its top-selling Qashqai model in Europe as part of its global restructuring and cost-cutting efforts. The move could leave the Japanese automaker trailing rivals in a key market segment as European and Chinese competitors expand their affordable EV offerings. (Reuters)

EMEA and Others

- European shares open lower. European shares fell on Tuesday as expectations of imminent Federal Reserve rate hikes and concerns over rising corporate spending on AI weighed on sentiment. STOXX 600 index declined 0.73%, while Germany's DAX, France's CAC 40, and London’s FTSE 100 slipped 0.98%, 0.71%, and 0.09% respectively. Technology stocks were among the biggest drags as higher borrowing costs raised concerns over debt-funded investment. (Reuters)

- Ferrari names former BMW executive CMO. Ferrari (RACE IM -1.47%) appointed former BMW (BMW GR -0.16%) Italy chief Massimiliano Di Silvestre as chief marketing and commercial officer, replacing long-serving executive Enrico Galliera. Di Silvestre will join Ferrari on July 1 and report directly to CEO Benedetto Vigna. (Reuters)

- Heineken appoints JDE Peet's CEO. Heineken (HEIN NA +2.2%) named JDE Peet's (JDE GR +0.19%) CEO Rafael Oliveira as its new chair and CEO, marking the first time the Dutch brewer has appointed an outsider to the top role. Oliveira will join Heineken on October 1 for a four-year term as the firm seeks to accelerate its 2030 strategy and revive growth. (Reuters)

TRADERS’ CORNER

Source: TradingView | HBM (2142.HK)

Last Price: HK$11.22 Support Levels: HK$10.06 (-10.3%)/ HK$9.46 (-15.7%) Resistance Levels: HK$13.68 (+21.9%)/ HK$14.98 (+33.5%) |

Our Technical View

- Price was rejected at its support-turned-resistance zone, which is punctuated by a bearish engulfing candlestick pattern.

- This structural failure is heavily validated by a deteriorating momentum profile, with the MACD firmly entrenched in a negative regime and primed to execute a fresh bearish crossover.

- This confluence of overhead supply and expanding selling velocity strongly favours a continuation of the broader primary downtrend.

Source: TradingView | Sunny Optical (2382.HK)

Last Price: HK$79.55 Support Levels: HK$73.80 (-7.2%)/ HK$69.80 (-12.3%) Resistance Levels: HK$86.30 (+8.5%)/ HK$90.05 (+13.2%) |

Our Technical View

- Price was capped at its support-turned-resistance zone, and subsequently broke down to violate its recent structural low.

- This technical weakness is reinforced by the MACD which has turned bearish and is expanding lower within a negative regime.

- This combination of an established overhead supply ceiling and accelerating downward velocity significantly increases the probability of a sustained extension lower.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.