Overnight Markets

Today’s Must-Know News

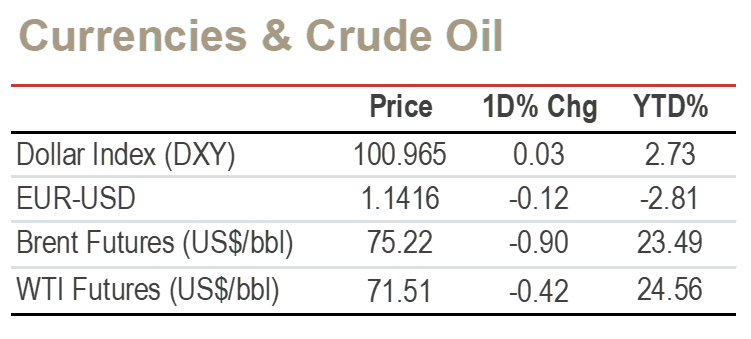

S&P 500 and Nasdaq-100 futures fell 0.3% and 0.5% Sunday as renewed US-Iran strikes pushed front-month WTI 3.1% higher, while S&P 500 cash gained 0.42% Friday & for a second straight weekly rise of 1.23%. This week’s key earnings include Bank of America (BAC +0.71%) & JPMorgan (JPM +0.3%) on Jul 14, J&J (JNJ -0.82%) on Jul 15 and TSMC (TSM -0.65%; 2330.TT -2.03%) on Jul 16. SK Hynix US ADRs (SKHYV +12.76%) jumped above its USD 149 offer price Friday and may issue more shares, while warning memory shortages could persist beyond 2030 - regular trading begins under ticker SKHY later today (Jul 13). The US 10% Section 122 import surcharge is scheduled to expire on Jul 24, with any extension posing renewed inflation and market risks. The Trump administration plans to ease UAE export controls, expanding access to AI chips from Nvidia (NVDA +4.03%) and AMD (AMD +2.04%). Meta (META +5.97%) outperformed after SemiAnalysis projected that its AI-compute capacity could exceed OpenAI and Anthropic combined by year-end. Tencent (0700.HK +2.0%) is in talks to become Manus’ largest external shareholder after Chinese regulators blocked Meta’s planned acquisition of the agentic-AI developer. Healthcare (XLV -0.82%) lagged as Moderna (MRNA -10.83%) posted its worst session in over a year after JPMorgan reportedly recommended shorting the stock. Shein is targeting a Hong Kong IPO in Sep-Oct 2026 after securing CSRC approval, marking its third listing attempt. JNJ, TSM, NVDA, META, 0700.HK are our Core Recommendations.

Trader’s Corner (Details on Page 5-6)

| Last Close | Support | Resistance |

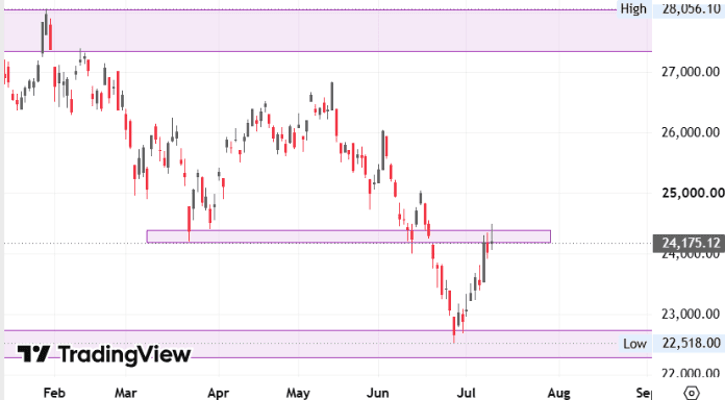

Hang Seng Index | 24,175.12 | 22,520 / 21,565 | 24,565 / 25,045 |

Hang Seng Tech Index | 4,499.00 | 4,230/ 3,765 | 4,870 / 5,040 |

Hong Kong IPO Calendar

No upcoming IPOs.

Americas

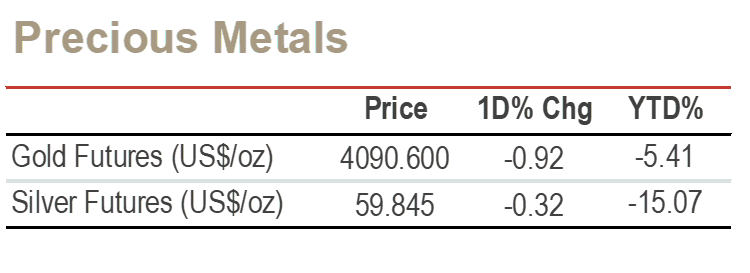

Iran strikes, earnings optimism. The US launched its fourth round of strikes on Iran within a week as Washington and Tehran disputed whether the Strait of Hormuz remained open, while gold (XAU -1.2%) fell to USD 4,069.47/oz on early Sunday. S&P 500 cash rose 0.42% in the regular trading session as 2Q earnings are projected to grow 23.7% yoy per LSEG, with materials leading on higher fertilizer prices and Moderna (MRNA -10.83%) driving health care lower after JPMorgan named it a short idea. (Bloomberg)

Memory competition broadens. Samsung’s (005930 KS +1.42%) weaker-than-expected earnings response weighed on Micron (MU -1.24%), although SK Hynix’s successful listing restored confidence in the AI-memory cycle. China’s CXMT is also expanding rapidly, increasing competitive pressure on Samsung, SK Hynix (000660 KS -2.31%) and Micron. (Bloomberg)

AI developers compete on cost. OpenAI, Meta (META +5.97%) and SpaceXAI released new models focused on lowering customer costs as businesses scrutinise usage-based AI bills. OpenAI said GPT-5.6 can complete more work with fewer tokens, while Meta indicated it is prepared to price its developer offering aggressively. (Bloomberg) META is our Core Recommendation.

Meta reverses image launch. Meta (META +5.97%) withdrew its newly launched Muse Image feature following criticism that public Instagram photos were automatically available for AI image generation without clear consent. (Reuters) META is our Core Recommendation.

SpaceX AI returns stay earthbound. SpaceX (SPCX -4.51%) could generate over USD 28 bn annually from terrestrial AI deals with Anthropic, Alphabet (GOOGL -0.48%) and Reflection AI, while orbital data centres remain constrained by launch costs and technology. (Reuters) GOOGL is our Trading Buy.

Amazon settlement shifts liability. Amazon (AMZN -0.69%) agreed to a USD 201 mn judgment over alleged illegal gambling transactions through social-casino apps, but class members would pursue payment from third-party developers rather than Amazon. The settlement, which requires court approval, follows earlier developer agreements that returned more than USD 650 mn to consumers. (Reuters) AMZN is our Core Recommendation.

Apple escalates OpenAI rivalry. Apple (AAPL -0.28%) sued OpenAI and two former employees, alleging they transferred confidential designs, supplier data and manufacturing processes. Apple said 400+ former employees now work at OpenAI, which denied seeking trade secrets. (Reuters)

Delta signals resilient pricing power. Delta Air Lines (DAL -1.81%) reaffirmed its 2026 profit forecast and issued a stronger-than-expected 3Q outlook, saying fare increases helped recover about 60% of the quarterly fuel-cost rise. The airline expects its annual fuel bill to increase by USD 4 bn and warned that fuel-price volatility remains a key risk. (Reuters)

JPMorgan tests investing agents. JPMorgan (JPM +1.47%) developed an AI asset-allocation system that outperformed a traditional 60/40 portfolio by 0.7 percentage point annually in historical simulations, with lower volatility. The bank cautioned that backtested results do not establish that AI can consistently outperform in live markets. (Bloomberg)

Circle secures bank charter. Circle Internet (CRCL +4.97%) received final approval to establish Circle National Trust, allowing it to provide institutional digital-asset custody under federal oversight. The charter does not permit Circle to accept cash deposits or extend loans, limiting its near-term revenue contribution. (Bloomberg)

Netflix considers broader content mix. Netflix (NFLX -2.78%) is considering live television, streaming bundles, additional sports and short-form video to strengthen engagement and advertising growth. Its US television-viewing share fell to 7.8% in April from 9% at end-2025, although TF1’s linear-channel launch increased viewing by 16% within three weeks. (Bloomberg)

Altera accelerates growth before IPO. Altera, spun out of Intel (INTC -2.4%), is growing about 20% annually and more than doubling operating income as it prepares for an eventual listing, with mid-20% growth expected this year. Silver Lake owns 51% after a USD 4.46 bn investment valuing Altera at USD 8.75 bn, while Intel retains 49%. (Reuters)

Greater China

China tech rotation lifts Hong Kong. HSI rose 0.6% on Friday and had its strongest weekly gain since March 2025, as investors rotated into internet stocks; Alibaba (9988.HK +2.04%) gained while Tencent (0700.HK -2.0%) fell. Mainland shares also advanced, with the CSI 300 down 1.96%, as investors took profits ahead of Changxin Memory Technologies’ anticipated listing. UBS said further internet-sector gains may require stronger earnings confirmation. (Reuters).

Shein clears key Hong Kong hurdle. Shein won Chinese regulatory approval for its Hong Kong IPO, advancing a listing plan after failed attempts in New York and London and nearly three years of delays. The approval allows the fast-fashion retailer to begin investor roadshows and prepare for a listing committee hearing at Hong Kong Exchanges and Clearing (0388.HK -0.11%). (Reuters)

Tencent eyes control of Manus. Tencent (0700.HK -2.0%) is in talks to become AI startup Manus’ largest shareholder, joining existing investors to buy the company back from Meta (META +5.97%) for at least USD 2 bn after Beijing ordered Meta to unwind the acquisition. Manus develops autonomous AI agents and relocated its operations from China to Singapore last year. (Reuters) 0700.HK & META are our Core Recommendations.

Zhipu keeps frontier model open. Zhipu (2513.HK -19.29%) released GLM-5.2 under an open-source licence and said frontier AI should remain widely accessible rather than controlled by a small number of companies. The company does not plan to prioritise short-term application monetisation over the next two years, focusing instead on autonomous agents and long-duration tasks. (Bloomberg)

HKEX refreshes IPO listing panel. JPMorgan Chase’s (JPM +1.47%) Nelly Pai and Citigroup’s (C +1.59%) Alexander Schrantz will join Hong Kong Exchanges and Clearing’s (0388.HK -0.11%) Listing Committee, which reviews IPO applications and advises the exchange. They will replace two members stepping down after reaching the six-year term limit. (Bloomberg)

Rubin delay rumours hit PCB supplier. Victory Giant Technology (2476.HK -12.87%; 300476.SZ -8.32%) fell sharply after investors raised concerns over a possible delay to Nvidia’s (NVDA +4.03%) Rubin server platform and potential order cancellations. The firm said cooperation with key customers, capacity expansion and product deliveries remain on schedule. (Reuters) NVDA is our Core Recommendation.

NIO expands ES8 lineup. NIO (NIO flat; 9866.HK +1.63%) launched a five-seat ES8 priced RMB 382,800, or RMB 274,800 under its battery-rental plan, with deliveries starting on July 10. CEO William Li said higher raw-material costs raised per-vehicle expenses by nearly RMB 20,000, but the firm is working with suppliers to limit price increases. (Reuters)

KYEC expands US chip testing. King Yuan Electronics (2449.TT +0.98%) plans to invest up to USD 1.4 bn in a US facility to support growth and strengthen its global supply-chain position. The Nvidia (NVDA +4.03%) supplier did not disclose the site, construction timeline or customers to be served. (Reuters) NVDA is our Core Recommendation.

Asia ex. China

Japan policy supports yen. The yen and Japanese government bonds strengthened after Finance Minister Satsuki Katayama called for pension funds to allocate more capital to domestic assets. Japan’s producer-price growth also accelerated to its fastest pace since early 2023, supporting expectations for further Bank of Japan tightening. (Bloomberg)

SoftBank eyes Seven & i stake. SoftBank (9434 JP +0.61%) and PayPay are reportedly considering an investment in Seven & i Holdings (3382 JP -0.05%), with total funding potentially reaching JPY 300 bn, or USD 1.85 bn. Sumitomo Mitsui Card, owned by Sumitomo Mitsui Financial Group (8316 JP +0.0&%), may also participate. (Reuters)

Yen warning hits Fast Retailing. Fast Retailing (9983 JP -3.59%) fell despite raising its full-year operating-profit forecast to a record JPY 730 bn, as the weak yen threatens Uniqlo’s fourth-quarter sales and earnings in Japan. (Reuters)

EMEA and Others

Tech Selloff ends Europe’s winning streak. STOXX 600 rose 0.04% on Friday, while France’s CAC and UK’s FTSE edged up 0.15% and 0.24% respectively. Germany’s DAX declined 0.2% as investors rotated away from major AI beneficiaries and renewed US-Iran tensions lifted Brent crude. Technology stocks lost, with Soitec (SOI FP -5.86%) and ASML (ASML NA -2.11%) falling, while investors await earnings for fresh direction. (Reuters)

Niel becomes Vodafone’s largest shareholder. French billionaire Xavier Niel will acquire e&’s (EAND UH +5.29%) 16.2% stake in Vodafone (VOD LN +12.62%) for about GBP 4.4 bn, or nearly USD 6 bn, making him the British telecom group’s largest shareholder. (Reuters)

China slump weighs on Volkswagen deliveries. Volkswagen (VOW GR -2.16%) reported an 8.6% decline in 2Q global deliveries to 2.077 mn vehicles, its steepest quarterly drop in four years, as China deliveries plunged 36.6%. Gains of 7.7% in North America, 1.8% in Western Europe and 6.7% in Central and Eastern Europe failed to offset the weakness. (Reuters)

Apollo funding strengthens Bayer’s balance sheet. Bayer (BAYN GR -0.39%) secured EUR 3 bn (USD 3.4 bn) from Apollo-managed funds (APO +0.42%) in exchange for a minority stake in a new entity holding its contraceptives business, while retaining majority ownership and full operational control. The deal, expected to close in 3Q26, will support bond repayments and litigation-related liquidity needs. (Reuters)

TRADERS’ CORNER

Source: TradingView |

| Hang Seng Index

|

Our Technical View

Weekly Chart: The index’s recent relief rally has met definitive exhaustion, having been rejected directly at the former support level that is now functioning as a structural overhead resistance. This structural failure is validated by the RSI remaining firmly underneath the 50 midline to confirm a persistent sellers' regime. Consequently, the technical framework strongly points to an immediate downward continuation out of this supply zone.

Daily Chart: The corrective recovery has halted precisely at a dual-layered resistance cluster, where the former support floor aligns directly with an open gap window. The printing of a Doji at this intersection, coupled with an RSI neutralising around the 50 midline, indicates a complete exhaustion of buying pressure. Hence, the structural framework points towards a continuation of the dominant bearish trend, which is contingent upon a confirmed bearish candle to validate the downward reversal.

Source: TradingView |

| Hang Seng Tech Index

|

Our Technical View

Weekly Chart: Price has executed a technical bounce, printing a weekly bullish Harami candlestick pattern following a successful defence of its previous low support zone. The RSI remains suppressed below its 50-neutral baseline. This positions the index for a tactical rally toward its overhead resistance target at 5,230, where the market will seek its next directional resolution vector.

Daily Chart: The index’s upward advance has paused at a gap window, which is currently functioning as active overhead resistance. Failure to clear this structural ceiling will likely shift the near-term trajectory back toward a test of the 4,229 horizontal support floor. The RSI is holding just above the 50 midline. The market requires a confirmed daily close above the gap boundary to validate a sustainable continuation higher.

Today’s Must-Know News

S&P 500 and Nasdaq-100 futures fell 0.3% and 0.5% Sunday as renewed US-Iran strikes pushed front-month WTI 3.1% higher, while S&P 500 cash gained 0.42% Friday & for a second straight weekly rise of 1.23%. This week’s key earnings include Bank of America (BAC +0.71%) & JPMorgan (JPM +0.3%) on Jul 14, J&J (JNJ -0.82%) on Jul 15 and TSMC (TSM -0.65%; 2330.TT -2.03%) on Jul 16. SK Hynix US ADRs (SKHYV +12.76%) jumped above its USD 149 offer price Friday and may issue more shares, while warning memory shortages could persist beyond 2030 - regular trading begins under ticker SKHY later today (Jul 13). The US 10% Section 122 import surcharge is scheduled to expire on Jul 24, with any extension posing renewed inflation and market risks. The Trump administration plans to ease UAE export controls, expanding access to AI chips from Nvidia (NVDA +4.03%) and AMD (AMD +2.04%). Meta (META +5.97%) outperformed after SemiAnalysis projected that its AI-compute capacity could exceed OpenAI and Anthropic combined by year-end. Tencent (0700.HK +2.0%) is in talks to become Manus’ largest external shareholder after Chinese regulators blocked Meta’s planned acquisition of the agentic-AI developer. Healthcare (XLV -0.82%) lagged as Moderna (MRNA -10.83%) posted its worst session in over a year after JPMorgan reportedly recommended shorting the stock. Shein is targeting a Hong Kong IPO in Sep-Oct 2026 after securing CSRC approval, marking its third listing attempt. JNJ, TSM, NVDA, META, 0700.HK are our Core Recommendations.

Trader’s Corner (Details on Page 5-6)

| Last Close | Support | Resistance |

Hang Seng Index | 24,175.12 | 22,520 / 21,565 | 24,565 / 25,045 |

Hang Seng Tech Index | 4,499.00 | 4,230/ 3,765 | 4,870 / 5,040 |

Hong Kong IPO Calendar

No upcoming IPOs.

Americas

Iran strikes, earnings optimism. The US launched its fourth round of strikes on Iran within a week as Washington and Tehran disputed whether the Strait of Hormuz remained open, while gold (XAU -1.2%) fell to USD 4,069.47/oz on early Sunday. S&P 500 cash rose 0.42% in the regular trading session as 2Q earnings are projected to grow 23.7% yoy per LSEG, with materials leading on higher fertilizer prices and Moderna (MRNA -10.83%) driving health care lower after JPMorgan named it a short idea. (Bloomberg)

Memory competition broadens. Samsung’s (005930 KS +1.42%) weaker-than-expected earnings response weighed on Micron (MU -1.24%), although SK Hynix’s successful listing restored confidence in the AI-memory cycle. China’s CXMT is also expanding rapidly, increasing competitive pressure on Samsung, SK Hynix (000660 KS -2.31%) and Micron. (Bloomberg)

AI developers compete on cost. OpenAI, Meta (META +5.97%) and SpaceXAI released new models focused on lowering customer costs as businesses scrutinise usage-based AI bills. OpenAI said GPT-5.6 can complete more work with fewer tokens, while Meta indicated it is prepared to price its developer offering aggressively. (Bloomberg) META is our Core Recommendation.

Meta reverses image launch. Meta (META +5.97%) withdrew its newly launched Muse Image feature following criticism that public Instagram photos were automatically available for AI image generation without clear consent. (Reuters) META is our Core Recommendation.

SpaceX AI returns stay earthbound. SpaceX (SPCX -4.51%) could generate over USD 28 bn annually from terrestrial AI deals with Anthropic, Alphabet (GOOGL -0.48%) and Reflection AI, while orbital data centres remain constrained by launch costs and technology. (Reuters) GOOGL is our Trading Buy.

Amazon settlement shifts liability. Amazon (AMZN -0.69%) agreed to a USD 201 mn judgment over alleged illegal gambling transactions through social-casino apps, but class members would pursue payment from third-party developers rather than Amazon. The settlement, which requires court approval, follows earlier developer agreements that returned more than USD 650 mn to consumers. (Reuters) AMZN is our Core Recommendation.

Apple escalates OpenAI rivalry. Apple (AAPL -0.28%) sued OpenAI and two former employees, alleging they transferred confidential designs, supplier data and manufacturing processes. Apple said 400+ former employees now work at OpenAI, which denied seeking trade secrets. (Reuters)

Delta signals resilient pricing power. Delta Air Lines (DAL -1.81%) reaffirmed its 2026 profit forecast and issued a stronger-than-expected 3Q outlook, saying fare increases helped recover about 60% of the quarterly fuel-cost rise. The airline expects its annual fuel bill to increase by USD 4 bn and warned that fuel-price volatility remains a key risk. (Reuters)

JPMorgan tests investing agents. JPMorgan (JPM +1.47%) developed an AI asset-allocation system that outperformed a traditional 60/40 portfolio by 0.7 percentage point annually in historical simulations, with lower volatility. The bank cautioned that backtested results do not establish that AI can consistently outperform in live markets. (Bloomberg)

Circle secures bank charter. Circle Internet (CRCL +4.97%) received final approval to establish Circle National Trust, allowing it to provide institutional digital-asset custody under federal oversight. The charter does not permit Circle to accept cash deposits or extend loans, limiting its near-term revenue contribution. (Bloomberg)

Netflix considers broader content mix. Netflix (NFLX -2.78%) is considering live television, streaming bundles, additional sports and short-form video to strengthen engagement and advertising growth. Its US television-viewing share fell to 7.8% in April from 9% at end-2025, although TF1’s linear-channel launch increased viewing by 16% within three weeks. (Bloomberg)

Altera accelerates growth before IPO. Altera, spun out of Intel (INTC -2.4%), is growing about 20% annually and more than doubling operating income as it prepares for an eventual listing, with mid-20% growth expected this year. Silver Lake owns 51% after a USD 4.46 bn investment valuing Altera at USD 8.75 bn, while Intel retains 49%. (Reuters)

Greater China

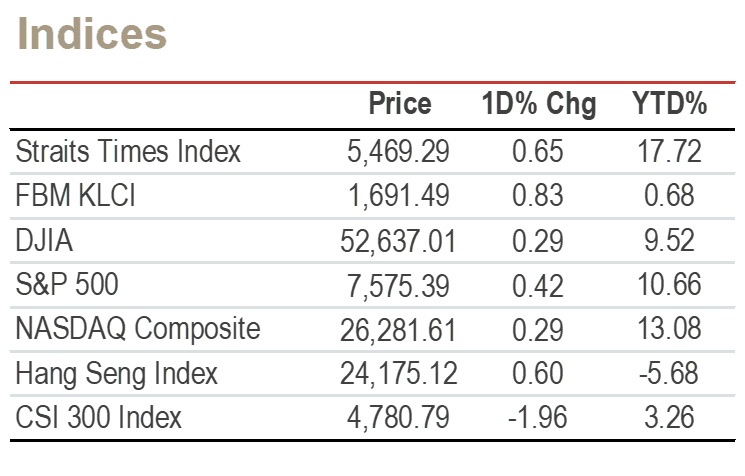

China tech rotation lifts Hong Kong. HSI rose 0.6% on Friday and had its strongest weekly gain since March 2025, as investors rotated into internet stocks; Alibaba (9988.HK +2.04%) gained while Tencent (0700.HK -2.0%) fell. Mainland shares also advanced, with the CSI 300 down 1.96%, as investors took profits ahead of Changxin Memory Technologies’ anticipated listing. UBS said further internet-sector gains may require stronger earnings confirmation. (Reuters).

Shein clears key Hong Kong hurdle. Shein won Chinese regulatory approval for its Hong Kong IPO, advancing a listing plan after failed attempts in New York and London and nearly three years of delays. The approval allows the fast-fashion retailer to begin investor roadshows and prepare for a listing committee hearing at Hong Kong Exchanges and Clearing (0388.HK -0.11%). (Reuters)

Tencent eyes control of Manus. Tencent (0700.HK -2.0%) is in talks to become AI startup Manus’ largest shareholder, joining existing investors to buy the company back from Meta (META +5.97%) for at least USD 2 bn after Beijing ordered Meta to unwind the acquisition. Manus develops autonomous AI agents and relocated its operations from China to Singapore last year. (Reuters) 0700.HK & META are our Core Recommendations.

Zhipu keeps frontier model open. Zhipu (2513.HK -19.29%) released GLM-5.2 under an open-source licence and said frontier AI should remain widely accessible rather than controlled by a small number of companies. The company does not plan to prioritise short-term application monetisation over the next two years, focusing instead on autonomous agents and long-duration tasks. (Bloomberg)

HKEX refreshes IPO listing panel. JPMorgan Chase’s (JPM +1.47%) Nelly Pai and Citigroup’s (C +1.59%) Alexander Schrantz will join Hong Kong Exchanges and Clearing’s (0388.HK -0.11%) Listing Committee, which reviews IPO applications and advises the exchange. They will replace two members stepping down after reaching the six-year term limit. (Bloomberg)

Rubin delay rumours hit PCB supplier. Victory Giant Technology (2476.HK -12.87%; 300476.SZ -8.32%) fell sharply after investors raised concerns over a possible delay to Nvidia’s (NVDA +4.03%) Rubin server platform and potential order cancellations. The firm said cooperation with key customers, capacity expansion and product deliveries remain on schedule. (Reuters) NVDA is our Core Recommendation.

NIO expands ES8 lineup. NIO (NIO flat; 9866.HK +1.63%) launched a five-seat ES8 priced RMB 382,800, or RMB 274,800 under its battery-rental plan, with deliveries starting on July 10. CEO William Li said higher raw-material costs raised per-vehicle expenses by nearly RMB 20,000, but the firm is working with suppliers to limit price increases. (Reuters)

KYEC expands US chip testing. King Yuan Electronics (2449.TT +0.98%) plans to invest up to USD 1.4 bn in a US facility to support growth and strengthen its global supply-chain position. The Nvidia (NVDA +4.03%) supplier did not disclose the site, construction timeline or customers to be served. (Reuters) NVDA is our Core Recommendation.

Asia ex. China

Japan policy supports yen. The yen and Japanese government bonds strengthened after Finance Minister Satsuki Katayama called for pension funds to allocate more capital to domestic assets. Japan’s producer-price growth also accelerated to its fastest pace since early 2023, supporting expectations for further Bank of Japan tightening. (Bloomberg)

SoftBank eyes Seven & i stake. SoftBank (9434 JP +0.61%) and PayPay are reportedly considering an investment in Seven & i Holdings (3382 JP -0.05%), with total funding potentially reaching JPY 300 bn, or USD 1.85 bn. Sumitomo Mitsui Card, owned by Sumitomo Mitsui Financial Group (8316 JP +0.0&%), may also participate. (Reuters)

Yen warning hits Fast Retailing. Fast Retailing (9983 JP -3.59%) fell despite raising its full-year operating-profit forecast to a record JPY 730 bn, as the weak yen threatens Uniqlo’s fourth-quarter sales and earnings in Japan. (Reuters)

EMEA and Others

Tech Selloff ends Europe’s winning streak. STOXX 600 rose 0.04% on Friday, while France’s CAC and UK’s FTSE edged up 0.15% and 0.24% respectively. Germany’s DAX declined 0.2% as investors rotated away from major AI beneficiaries and renewed US-Iran tensions lifted Brent crude. Technology stocks lost, with Soitec (SOI FP -5.86%) and ASML (ASML NA -2.11%) falling, while investors await earnings for fresh direction. (Reuters)

Niel becomes Vodafone’s largest shareholder. French billionaire Xavier Niel will acquire e&’s (EAND UH +5.29%) 16.2% stake in Vodafone (VOD LN +12.62%) for about GBP 4.4 bn, or nearly USD 6 bn, making him the British telecom group’s largest shareholder. (Reuters)

China slump weighs on Volkswagen deliveries. Volkswagen (VOW GR -2.16%) reported an 8.6% decline in 2Q global deliveries to 2.077 mn vehicles, its steepest quarterly drop in four years, as China deliveries plunged 36.6%. Gains of 7.7% in North America, 1.8% in Western Europe and 6.7% in Central and Eastern Europe failed to offset the weakness. (Reuters)

Apollo funding strengthens Bayer’s balance sheet. Bayer (BAYN GR -0.39%) secured EUR 3 bn (USD 3.4 bn) from Apollo-managed funds (APO +0.42%) in exchange for a minority stake in a new entity holding its contraceptives business, while retaining majority ownership and full operational control. The deal, expected to close in 3Q26, will support bond repayments and litigation-related liquidity needs. (Reuters)

TRADERS’ CORNER

Source: TradingView |

| Hang Seng Index

|

Our Technical View

Weekly Chart: The index’s recent relief rally has met definitive exhaustion, having been rejected directly at the former support level that is now functioning as a structural overhead resistance. This structural failure is validated by the RSI remaining firmly underneath the 50 midline to confirm a persistent sellers' regime. Consequently, the technical framework strongly points to an immediate downward continuation out of this supply zone.

Daily Chart: The corrective recovery has halted precisely at a dual-layered resistance cluster, where the former support floor aligns directly with an open gap window. The printing of a Doji at this intersection, coupled with an RSI neutralising around the 50 midline, indicates a complete exhaustion of buying pressure. Hence, the structural framework points towards a continuation of the dominant bearish trend, which is contingent upon a confirmed bearish candle to validate the downward reversal.

Source: TradingView |

| Hang Seng Tech Index

|

Our Technical View

Weekly Chart: Price has executed a technical bounce, printing a weekly bullish Harami candlestick pattern following a successful defence of its previous low support zone. The RSI remains suppressed below its 50-neutral baseline. This positions the index for a tactical rally toward its overhead resistance target at 5,230, where the market will seek its next directional resolution vector.

Daily Chart: The index’s upward advance has paused at a gap window, which is currently functioning as active overhead resistance. Failure to clear this structural ceiling will likely shift the near-term trajectory back toward a test of the 4,229 horizontal support floor. The RSI is holding just above the 50 midline. The market requires a confirmed daily close above the gap boundary to validate a sustainable continuation higher.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.