Overnight Markets

S&P 500 (SPX -0.53%) & Nasdaq Composite (CCMP -1.61%) fell Thursday, while S&P 500 Equal Weight (SPW +1.00%) hit a record as investors rotated into consumer staples (XLP +2.8%) & health care (XLV +2.22%). TSMC (2330.TT +1.23%; TSM -2.32%) fell after raising its 2026 capex outlook to USD 60–64 bn from USD 52–56 bn, despite stronger-than-expected 2Q earnings. Semicon (SOXX -4.46%) was dragged lower by Nvidia (NVDA -2.4%), AMD (AMD -5.33%), Micron (MU -5.65%), Marvell (MRVL -8.71%) & Arm (ARM -5.41%). Alphabet (GOOGL -4.4%) fell after Gemini 3.5 Pro was delayed by several months as Google works to improve its coding performance. GOOGL reports 2Q earnings after-market July 22 (Wed) with options implying a 3.16% post-earnings move. SK Hynix US ADRs (SKHY -13.69%) fell to USD 152.31 (IPO price: USD149). South Korea ETF (EWY -4.82%) recorded inflows of more than USD 1.1 bn on Wed, the largest daily inflow on record, as investors sought cheaper indirect exposure to SK Hynix (000660 KS -9.5%). South Korea separately suspended new single-stock leveraged ETF listings to curb market volatility. CXMT’s Shanghai IPO retail tranche was 212 times subscribed after attracting 9.4 mn retail applications ahead of its July 27 debut. SpaceX (SPCX -3.08%) postponed its Starship test and traded below its USD 135 IPO price. HK-listed casino stocks may weaken (0027.HK +3.51%; 1928.HK +2.78%; 2282.HK +3.18%; 1128.HK +5.04%) after Macau’s VIP 2Q gaming revenue fell 2.6% yoy. Gold (XAU -2.07%) slipped to USD 3,976.5/oz challenging June intraday low, as escalating Middle East tensions drove oil higher and lifted US Treasury yields. The temporary 10% US global import tariff is set to expire on July 24 unless Congress moves to extend the measure. XLP, TSM & 0027.HK are our Core Recommendations; GOOGL, SOXX & SKHY are our Trading Buys.

Trader’s Corner (Details on Page 7-8)

Ticker | Name | Rec. | Support | Resistance |

9868.HK | Xpeng | - | HKD 49.80 / 48.60 | HKD 72.35 / 75.80 |

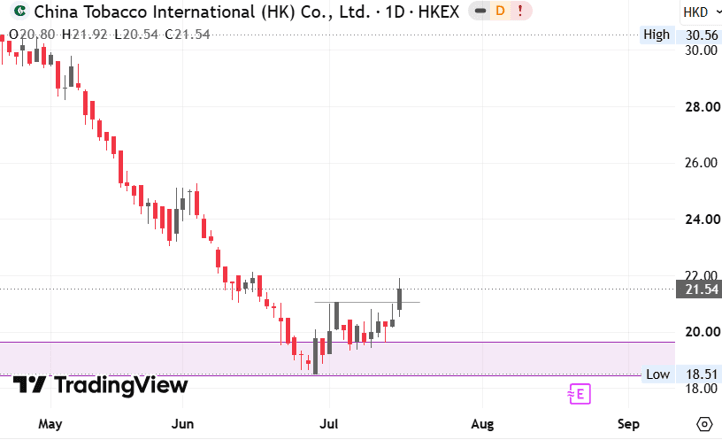

6055.HK | China Tobacco | - | HKD 19.62 / 18.52 | HKD 25.28 / 29.52 |

CR = Core Recommendation; TB = Trading Buy

Hong Kong IPO Calendar

No upcoming IPOs.

Americas

- Netflix guidance disappoints again. Netflix (NFLX +0.91%; -8.7% after hours) forecast 3Q revenue of USD 12.86 bn and EPS of USD 0.82, below estimates of USD 13 bn and USD 0.84, while 2Q results were broadly in line. The firm maintained its USD 3 bn advertising-revenue target but will reduce viewing-hours disclosures to annually from January 2027.

- Trump returns focus to election security. President Trump planned a prime-time address ahead of November’s midterms as the White House considered releasing intelligence on China’s intentions or capacity to interfere in the 2020 election. The intelligence reportedly showed no evidence that Beijing changed votes, while Republicans face voter concerns over high living and energy costs.

- Micron secures automotive memory demand. Micron (MU -5.65%) signed long-term supply agreements with Qualcomm (QCOM -4.14%), Visteon (VC +0.66%), Denso (6902 JP +1.13%) and Hyundai Mobis (012330.KS -0.31%) to provide memory and storage for AI-enabled vehicles. The deals aim to secure supply and pricing as demand from advanced driver-assistance systems and digital cockpits expands. MU is our Trading Buy.

- Nvidia expands Japan robotics partnerships. Nvidia (NVDA -2.4%) is partnering with Fanuc (6954 JP +0.17%) and Yaskawa Electric (6506 JP +0.07%) to accelerate robotics and AI development, with CEO Jensen Huang saying AI will make robots more adaptable and accessible. (Reuters) NVDA is our Core Recommendation.

- AI demand supports Csquare’s IPO. Csquare (CSQR -1.57%) raised USD 1.05 bn after pricing 50 mn shares at USD 21 each, below its marketed range, valuing the data-centre operator at about USD 3.25 bn. Brookfield (BN -0.38%) will retain roughly 67% voting control, with trading set to begin on July 16. (Reuters)

- Trading and dealmaking drive bank earnings beats. All six major US banks exceeded 2Q profit forecasts as investment-banking revenue surpassed USD 60 bn in 1H26 and trading desks benefited from volatility: Goldman (GS -4.91%); JPMorgan (JPM -1.08%); Bank of America (BAC -0.16%); Citigroup (C -2.36%); Wells Fargo (WFC +0.64%), while Morgan Stanley (MS -4.45%) also reported record revenue. (Reuters)

- Lilly expands into psychedelic treatments. Eli Lilly (LLY +1.08%) agreed to acquire AtaiBeckley (ATAI +30%) for up to USD 3.8 bn, including USD 2.8 bn upfront and USD 1 bn in milestones, gaining late-stage depression treatment BPL-003. The deal is expected to close in 3Q26, with analysts estimating potential peak sales of USD 1-2 bn. (Reuters) LLY is our Core Recommendation.

- Apple prepares major iPad mini upgrade. Apple (AAPL +1.76%) plans to launch an OLED-equipped iPad mini by October, followed by refreshed entry-level iPads and iPad Air models in 2027 (Bloomberg)

- PayPal rejects USD 53 bn bid as inadequate. PayPal’s (PYPL +2.18%) board views Stripe and Advent’s USD 60.50-a-share proposal as undervaluing the firm and carrying financing and antitrust risks, although it has not formally responded. JPMorgan (JPM -1.08%) and Morgan Stanley (MS -4.45%) have arranged about USD 50 bn of financing, while Stripe and Advent would contribute USD 17 bn of equity (Reuters)

- Google faces regulatory setbacks and Gemini delay. Alphabet (GOOGL -4.44%) must open 11 Android functions andanonymised search data to AI rivals under EU rules, while an EU court said YouTube lacks automatic liability protection for commercial-partner videos. Separately, Gemini 3.5 Pro is reportedly months behind schedule after its coding performance fell short of internal targets (Reuters) GOOGL is our Trading Buy.

- Uber agrees USD 14.8 bn Delivery Hero takeover. Uber (UBER +1.89%) offered EUR 41.50 a share for Delivery Hero (DHER Gr -2.34%), a 34% premium to its three-month average, creating a delivery platform across 99 countries. Completion is targeted for 2H27, subject to an extended antitrust review and asset sales in 14 markets (Reuters)

- Meta ordered to release youth-wellbeing records. Meta (META -2.46%) failed to block the disclosure of four internal research communications in Washington, D.C.’s consumer-protection case over alleged harm to young Facebook and Instagram users. The firm has already provided more than 2.5 mn documents and faces a separate August trial in which several states are seeking USD 1.4 tn in penalties (Reuters) META is our Core Recommendation.

- Citadel Securities backs Crypto.com at USD 20 bn valuation. Citadel Securities invested USD 400 mn in Crypto.com’s first institutional funding round as the exchange expands beyond digital assets. The investment comes despite Bitcoin falling nearly 27% YTD and the broader cryptocurrency market declining to about USD 2.3 tn (Reuters)

- Samsung faces US memory-chip patent investigation. US regulators opened a probe into Samsung (005930 KS -7.31%) and products from Alphabet (GOOGL -4.44%); Nvidia (NVDA -2.4%); Broadcom (AVGO -5.03%); Super Micro Computer (SMCI -8.22%) following Netlist’s patent complaint. Netlist is seeking import and sales restrictions on disputed memory chips used in AI servers (Reuters) NVDA & AVGO are our Core Recommendations; GOOGL is our Trading Buy.

- Boeing approaches approval for 737 MAX fix. Boeing (BA -1.73%) is nearing certification of an engine anti-ice redesign needed for the MAX 7 and MAX 10, potentially enabling deliveries of about 39 completed aircraft. The MAX 10 has completed 98% of certification flight testing, while existing MAX aircraft will eventually require retrofits (Reuters)

- Cost controls lift UnitedHealth outlook. UnitedHealth (UNH +1.16%) beat 2Q profit estimates and raised its 2026 forecast as its medical cost ratio improved to 86.7%, supported by tighter Medicare cost management and higher Medicaid reimbursements. Progress across insurance and Optum strengthened confidence in its turnaround. (Reuters)

- Starbucks defeats shareholder sales lawsuit. A US judge dismissed allegations that Starbucks (SBUX +3.1%) concealed deteriorating US and China sales before its May 2024 forecast cut and 16% share-price decline. The ruling supports management’s explanation that its previous comments reflected the completed quarter rather than current trading (Reuters)

- Cyberattack halts Fairlife’s US production. Coca-Cola’s (KO +3.0%) Fairlife subsidiary temporarily suspended US production after unauthorised access affected operating systems. Coca-Cola said product safety was unaffected and Fairlife’s Canadian facilities remain operational (Reuters)

- Core US spending remains firm despite tariffs. June retail sales increased 0.2%, while the core measure rose 0.5%, prompting economists to raise Q2 GDP-growth estimates to as high as 2.4%. Sales were up 6.7% year on year despite higher prices linked to import tariffs and the Middle East conflict, although spending remained concentrated among wealthier households (Reuters)

Greater China

Alibaba shields Hong Kong from regional chip rout. The CSI300 fell 1.85% Thursday as regional semiconductor weakness weighed on mainland technology stocks, while the Hang Seng Index rose 1.33%. Alibaba (9988.HK +3.09%) led gains after saying its Qwen model will be integrated into Apple Intelligence products in China. (Reuters)

Xi promotes China’s open-source AI model. President Xi Jinping is expected to position China’s open-source AI as a global public good at the World Artificial Intelligence Conference, while Huawei debuts its Atlas 950 SuperPoD cluster built without Nvidia’s (NVDA -2.4%) most advanced chips. DeepSeek’s V4 model has also been adapted to run entirely on Huawei Ascend processors, highlighting China’s push for technological self-reliance. NVDA is our Core Recommendation.

CXMT IPO draws exceptional retail demand. ChangXin Memory Technologies attracted more than 200 times the shares available to retail investors for its USD 8.6 bn Shanghai IPO, potentially Asia’s largest listing this year. Six Chinese banks will earn at least USD 41 mn in fees, equivalent to 0.48% of proceeds (Reuters)

AI demand drives record TSMC profit. TSMC (2330.TT +1.23%; TSM -2.32%) reported a 77% jump in 2Q net profit to a record TWD 706.6 bn, or USD 22 bn, beating forecasts of TWD 632.6 bn, and raised 2026 capex guidance to USD 60-64 bn. The Nvidia (NVDA -2.4%) supplier also pledged a further USD 100 bn investment in Arizona as AI-chip demand remains robust, and lifted full-year USD revenue-growth guidance to slightly above 40%. (Reuters) TSM & NVDA are our Core Recommendations.

DeepSeek funding implies USD 52 bn valuation. Anhui Korrun’s (300577.SZ -2.86%) fund invested RMB 2.9 bn for an indirect 0.8265% stake in DeepSeek, valuing the AI developer at RMB 350.88 bn. DeepSeek is reportedly preparing another funding round of up to RMB 50 bn at a roughly RMB 500 bn valuation and aims to file for a Shanghai IPO this year (Reuters)

Xiaomi advances its robotics platform. Xiaomi (1810.HK +6.34%) released Xiaomi-Robotics-1, a foundation model designed to execute mobile manipulation tasks in unfamiliar environments using natural-language instructions (Bloomberg)

Baidu seeks mainland investor access. Baidu (9888.HK +2.6%; BIDU +1.2%) plans to upgrade its Hong Kong listing to primary status, creating a dual-primary structure with the US and paving the way for inclusion in Stock Connect. The move would broaden access to mainland capital, following a similar step by NetEase (9999.HK +0.99%; NTES -0.21%). (Bloomberg)

Sector volatility delays Syngenta IPO. Syngenta’s planned Hong Kong listing, expected to raise about USD 5 bn, may slip to 2027 as Middle East disruptions weigh on crop and fertilizer markets and regulatory scrutiny of its seeds business extends the approval process. The Sinochem-controlled firm had previously considered raising up to USD 10 bn. (Reuters)

Record consumer defaults complicate China stimulus. Chinese household non-performing loans rose more than 20% to RMB 2.22 tn in 2025, equivalent to 1.6% of GDP, while short-term household lending contracted 7% in June. Banks are tightening credit standards despite Beijing’s efforts to promote borrowing, limiting the effectiveness of consumption stimulus (Reuters)

European import fees pressure Shein’s IPO valuation. Shein is targeting a USD 40-50 bn Hong Kong valuation, but investors may demand closer to USD 30 bn after the EU introduced a EUR 3 fee per customs category on low-value e-commerce parcels. Europe generates about one-third of Shein’s revenue, making the tariff-like charge a material risk to 2026 sales and margins (Reuters)

Asia ex. China

BOJ tightening hurts almost half of Japanese companies. A Reuters survey found 49% of companies reported negative effects from rate increases, while only 5% benefited after the BOJ lifted its policy rate to 1%. Yen weakness was negative for 55% of respondents, and most companies viewed a rate above 1.25%-1.5% as increasingly restrictive for investment (Reuters)

Bank of Korea begins tightening cycle. The BOK raised its policy rate by 25 bps to 2.75%, its first increase in three-and-a-half years, and signalled further tightening as semiconductor-led growth fuels inflation. The bank expects GDP growth to materially exceed its previous 2.6% forecast, with most analysts anticipating another hike this year (Reuters)

Korea curbs leveraged ETFs after chip selloff. South Korea will suspend new single-stock leveraged ETF listings, raise required deposits to KRW 30 mn from KRW 10 mn and increase the minimum trade to 20 shares after the products amplified volatility. The KOSPI fell 6.4% as SK Hynix (000660 KS -9.5%); Samsung Electronics (005930 KS -7.31%) sold off, while the won strengthened 0.7% following the BOK rate increase (Reuters)

BHP workers approve further strike action. Electrical workers at BHP’s (BHP LN -4.3%) Port Hedland operations voted 97.5% in favour of stoppages lasting from 30 minutes to 24 hours after wage and employment-condition talks stalled. The port handles approximately USD 80 mn of iron ore daily, raising potential export-disruption risks (Reuters)

EMEA and Others

Middle East caution caps European gains. The Stoxx 600 edged up 0.16%, while Germany’s DAX and France’s CAC 40 fell 0.34% and 0.05% respectively, while the UK’s FTSE 100 gained +0.54%, as strong earnings were offset by geopolitical concerns. ASML (ASML NA +3.16%) advanced after strong results, while STMicroelectronics (STMPA FP -4.91%) and BE Semiconductor (BESI BA -3.20%) declined. (Reuters)

Energy drives strongest European earnings growth in three years. STOXX 600 firms are expected to report 16.7% 2Q earnings growth, but the rate falls to 6.4% excluding energy, where profits are forecast to rise more than 125%. Higher oil and gas prices following Strait of Hormuz disruptions account for much of the upgrade. (Reuters)

BMW cost cuts deepen amid tariffs and weak margins. BMW (BMW GR -0.1%) appointed Dorothea von Boxberg as HR chief as it accelerates restructuring after cutting its profit outlook and forecasting margins as low as 1%. Chinese competition, the electric-vehicle transition, US tariffs and Iran-related uncertainty are increasing pressure on German automakers (Reuters)

Adidas wins World Cup visibility battle. Adidas (ADS GR -0.05%) supplies both finalists, Argentina and Spain, while none of Nike’s (NKE) 12 sponsored teams reached the final. Nike shares have lost nearly one-third YTD, while Adidas increased its footwear-market share to 19.2% in June from 16.0% a year earlier (Reuters)

Merck wins approval for oral cholesterol drug. Merck (MRK GR -1.58%) received FDA approval for Lipfendra, the first oral PCSK9 inhibitor, after trials showed an almost 60% reduction in LDL cholesterol. The USD 315-a-month treatment could generate peak sales of about USD 5 bn by 2034 (Reuters)

European electric-vehicle demand accelerates. Battery-electric registrations reached 1.24 mn in 1H26, up 33.7% year on year, while June sales increased 39.5% to 275,060 units. Fully electric vehicles captured 25.6% of the 17 tracked European markets as subsidies and higher petrol prices supported adoption (Reuters)

TRADERS’ CORNER

Source: TradingView |

| Xpeng (9868.HK)

|

Our Technical View

The upward movement has accelerated following a successful rebound off the horizontal support and a subsequent breach of the recent price high, solidifying a higher-high and higher-low configuration.

The RSI is climbing steadily above its neutral threshold.

This indicates a strong technical probability for continued upward momentum.

Source: TradingView |

| China Tobacco (6055.HK)

|

Our Technical View

Price has successfully validated a baseline support and forced a breakout above its resistance peak.

The RSI is scaling steadily into the dominant buying regime above the 50 threshold.

Backed by this active demand insulation and institutional accumulation underneath the tape, the technical layout projects a high probability of a continuation higher.

S&P 500 (SPX -0.53%) & Nasdaq Composite (CCMP -1.61%) fell Thursday, while S&P 500 Equal Weight (SPW +1.00%) hit a record as investors rotated into consumer staples (XLP +2.8%) & health care (XLV +2.22%). TSMC (2330.TT +1.23%; TSM -2.32%) fell after raising its 2026 capex outlook to USD 60–64 bn from USD 52–56 bn, despite stronger-than-expected 2Q earnings. Semicon (SOXX -4.46%) was dragged lower by Nvidia (NVDA -2.4%), AMD (AMD -5.33%), Micron (MU -5.65%), Marvell (MRVL -8.71%) & Arm (ARM -5.41%). Alphabet (GOOGL -4.4%) fell after Gemini 3.5 Pro was delayed by several months as Google works to improve its coding performance. GOOGL reports 2Q earnings after-market July 22 (Wed) with options implying a 3.16% post-earnings move. SK Hynix US ADRs (SKHY -13.69%) fell to USD 152.31 (IPO price: USD149). South Korea ETF (EWY -4.82%) recorded inflows of more than USD 1.1 bn on Wed, the largest daily inflow on record, as investors sought cheaper indirect exposure to SK Hynix (000660 KS -9.5%). South Korea separately suspended new single-stock leveraged ETF listings to curb market volatility. CXMT’s Shanghai IPO retail tranche was 212 times subscribed after attracting 9.4 mn retail applications ahead of its July 27 debut. SpaceX (SPCX -3.08%) postponed its Starship test and traded below its USD 135 IPO price. HK-listed casino stocks may weaken (0027.HK +3.51%; 1928.HK +2.78%; 2282.HK +3.18%; 1128.HK +5.04%) after Macau’s VIP 2Q gaming revenue fell 2.6% yoy. Gold (XAU -2.07%) slipped to USD 3,976.5/oz challenging June intraday low, as escalating Middle East tensions drove oil higher and lifted US Treasury yields. The temporary 10% US global import tariff is set to expire on July 24 unless Congress moves to extend the measure. XLP, TSM & 0027.HK are our Core Recommendations; GOOGL, SOXX & SKHY are our Trading Buys.

Trader’s Corner (Details on Page 7-8)

Ticker | Name | Rec. | Support | Resistance |

9868.HK | Xpeng | - | HKD 49.80 / 48.60 | HKD 72.35 / 75.80 |

6055.HK | China Tobacco | - | HKD 19.62 / 18.52 | HKD 25.28 / 29.52 |

CR = Core Recommendation; TB = Trading Buy

Hong Kong IPO Calendar

No upcoming IPOs.

Americas

- Netflix guidance disappoints again. Netflix (NFLX +0.91%; -8.7% after hours) forecast 3Q revenue of USD 12.86 bn and EPS of USD 0.82, below estimates of USD 13 bn and USD 0.84, while 2Q results were broadly in line. The firm maintained its USD 3 bn advertising-revenue target but will reduce viewing-hours disclosures to annually from January 2027.

- Trump returns focus to election security. President Trump planned a prime-time address ahead of November’s midterms as the White House considered releasing intelligence on China’s intentions or capacity to interfere in the 2020 election. The intelligence reportedly showed no evidence that Beijing changed votes, while Republicans face voter concerns over high living and energy costs.

- Micron secures automotive memory demand. Micron (MU -5.65%) signed long-term supply agreements with Qualcomm (QCOM -4.14%), Visteon (VC +0.66%), Denso (6902 JP +1.13%) and Hyundai Mobis (012330.KS -0.31%) to provide memory and storage for AI-enabled vehicles. The deals aim to secure supply and pricing as demand from advanced driver-assistance systems and digital cockpits expands. MU is our Trading Buy.

- Nvidia expands Japan robotics partnerships. Nvidia (NVDA -2.4%) is partnering with Fanuc (6954 JP +0.17%) and Yaskawa Electric (6506 JP +0.07%) to accelerate robotics and AI development, with CEO Jensen Huang saying AI will make robots more adaptable and accessible. (Reuters) NVDA is our Core Recommendation.

- AI demand supports Csquare’s IPO. Csquare (CSQR -1.57%) raised USD 1.05 bn after pricing 50 mn shares at USD 21 each, below its marketed range, valuing the data-centre operator at about USD 3.25 bn. Brookfield (BN -0.38%) will retain roughly 67% voting control, with trading set to begin on July 16. (Reuters)

- Trading and dealmaking drive bank earnings beats. All six major US banks exceeded 2Q profit forecasts as investment-banking revenue surpassed USD 60 bn in 1H26 and trading desks benefited from volatility: Goldman (GS -4.91%); JPMorgan (JPM -1.08%); Bank of America (BAC -0.16%); Citigroup (C -2.36%); Wells Fargo (WFC +0.64%), while Morgan Stanley (MS -4.45%) also reported record revenue. (Reuters)

- Lilly expands into psychedelic treatments. Eli Lilly (LLY +1.08%) agreed to acquire AtaiBeckley (ATAI +30%) for up to USD 3.8 bn, including USD 2.8 bn upfront and USD 1 bn in milestones, gaining late-stage depression treatment BPL-003. The deal is expected to close in 3Q26, with analysts estimating potential peak sales of USD 1-2 bn. (Reuters) LLY is our Core Recommendation.

- Apple prepares major iPad mini upgrade. Apple (AAPL +1.76%) plans to launch an OLED-equipped iPad mini by October, followed by refreshed entry-level iPads and iPad Air models in 2027 (Bloomberg)

- PayPal rejects USD 53 bn bid as inadequate. PayPal’s (PYPL +2.18%) board views Stripe and Advent’s USD 60.50-a-share proposal as undervaluing the firm and carrying financing and antitrust risks, although it has not formally responded. JPMorgan (JPM -1.08%) and Morgan Stanley (MS -4.45%) have arranged about USD 50 bn of financing, while Stripe and Advent would contribute USD 17 bn of equity (Reuters)

- Google faces regulatory setbacks and Gemini delay. Alphabet (GOOGL -4.44%) must open 11 Android functions andanonymised search data to AI rivals under EU rules, while an EU court said YouTube lacks automatic liability protection for commercial-partner videos. Separately, Gemini 3.5 Pro is reportedly months behind schedule after its coding performance fell short of internal targets (Reuters) GOOGL is our Trading Buy.

- Uber agrees USD 14.8 bn Delivery Hero takeover. Uber (UBER +1.89%) offered EUR 41.50 a share for Delivery Hero (DHER Gr -2.34%), a 34% premium to its three-month average, creating a delivery platform across 99 countries. Completion is targeted for 2H27, subject to an extended antitrust review and asset sales in 14 markets (Reuters)

- Meta ordered to release youth-wellbeing records. Meta (META -2.46%) failed to block the disclosure of four internal research communications in Washington, D.C.’s consumer-protection case over alleged harm to young Facebook and Instagram users. The firm has already provided more than 2.5 mn documents and faces a separate August trial in which several states are seeking USD 1.4 tn in penalties (Reuters) META is our Core Recommendation.

- Citadel Securities backs Crypto.com at USD 20 bn valuation. Citadel Securities invested USD 400 mn in Crypto.com’s first institutional funding round as the exchange expands beyond digital assets. The investment comes despite Bitcoin falling nearly 27% YTD and the broader cryptocurrency market declining to about USD 2.3 tn (Reuters)

- Samsung faces US memory-chip patent investigation. US regulators opened a probe into Samsung (005930 KS -7.31%) and products from Alphabet (GOOGL -4.44%); Nvidia (NVDA -2.4%); Broadcom (AVGO -5.03%); Super Micro Computer (SMCI -8.22%) following Netlist’s patent complaint. Netlist is seeking import and sales restrictions on disputed memory chips used in AI servers (Reuters) NVDA & AVGO are our Core Recommendations; GOOGL is our Trading Buy.

- Boeing approaches approval for 737 MAX fix. Boeing (BA -1.73%) is nearing certification of an engine anti-ice redesign needed for the MAX 7 and MAX 10, potentially enabling deliveries of about 39 completed aircraft. The MAX 10 has completed 98% of certification flight testing, while existing MAX aircraft will eventually require retrofits (Reuters)

- Cost controls lift UnitedHealth outlook. UnitedHealth (UNH +1.16%) beat 2Q profit estimates and raised its 2026 forecast as its medical cost ratio improved to 86.7%, supported by tighter Medicare cost management and higher Medicaid reimbursements. Progress across insurance and Optum strengthened confidence in its turnaround. (Reuters)

- Starbucks defeats shareholder sales lawsuit. A US judge dismissed allegations that Starbucks (SBUX +3.1%) concealed deteriorating US and China sales before its May 2024 forecast cut and 16% share-price decline. The ruling supports management’s explanation that its previous comments reflected the completed quarter rather than current trading (Reuters)

- Cyberattack halts Fairlife’s US production. Coca-Cola’s (KO +3.0%) Fairlife subsidiary temporarily suspended US production after unauthorised access affected operating systems. Coca-Cola said product safety was unaffected and Fairlife’s Canadian facilities remain operational (Reuters)

- Core US spending remains firm despite tariffs. June retail sales increased 0.2%, while the core measure rose 0.5%, prompting economists to raise Q2 GDP-growth estimates to as high as 2.4%. Sales were up 6.7% year on year despite higher prices linked to import tariffs and the Middle East conflict, although spending remained concentrated among wealthier households (Reuters)

Greater China

Alibaba shields Hong Kong from regional chip rout. The CSI300 fell 1.85% Thursday as regional semiconductor weakness weighed on mainland technology stocks, while the Hang Seng Index rose 1.33%. Alibaba (9988.HK +3.09%) led gains after saying its Qwen model will be integrated into Apple Intelligence products in China. (Reuters)

Xi promotes China’s open-source AI model. President Xi Jinping is expected to position China’s open-source AI as a global public good at the World Artificial Intelligence Conference, while Huawei debuts its Atlas 950 SuperPoD cluster built without Nvidia’s (NVDA -2.4%) most advanced chips. DeepSeek’s V4 model has also been adapted to run entirely on Huawei Ascend processors, highlighting China’s push for technological self-reliance. NVDA is our Core Recommendation.

CXMT IPO draws exceptional retail demand. ChangXin Memory Technologies attracted more than 200 times the shares available to retail investors for its USD 8.6 bn Shanghai IPO, potentially Asia’s largest listing this year. Six Chinese banks will earn at least USD 41 mn in fees, equivalent to 0.48% of proceeds (Reuters)

AI demand drives record TSMC profit. TSMC (2330.TT +1.23%; TSM -2.32%) reported a 77% jump in 2Q net profit to a record TWD 706.6 bn, or USD 22 bn, beating forecasts of TWD 632.6 bn, and raised 2026 capex guidance to USD 60-64 bn. The Nvidia (NVDA -2.4%) supplier also pledged a further USD 100 bn investment in Arizona as AI-chip demand remains robust, and lifted full-year USD revenue-growth guidance to slightly above 40%. (Reuters) TSM & NVDA are our Core Recommendations.

DeepSeek funding implies USD 52 bn valuation. Anhui Korrun’s (300577.SZ -2.86%) fund invested RMB 2.9 bn for an indirect 0.8265% stake in DeepSeek, valuing the AI developer at RMB 350.88 bn. DeepSeek is reportedly preparing another funding round of up to RMB 50 bn at a roughly RMB 500 bn valuation and aims to file for a Shanghai IPO this year (Reuters)

Xiaomi advances its robotics platform. Xiaomi (1810.HK +6.34%) released Xiaomi-Robotics-1, a foundation model designed to execute mobile manipulation tasks in unfamiliar environments using natural-language instructions (Bloomberg)

Baidu seeks mainland investor access. Baidu (9888.HK +2.6%; BIDU +1.2%) plans to upgrade its Hong Kong listing to primary status, creating a dual-primary structure with the US and paving the way for inclusion in Stock Connect. The move would broaden access to mainland capital, following a similar step by NetEase (9999.HK +0.99%; NTES -0.21%). (Bloomberg)

Sector volatility delays Syngenta IPO. Syngenta’s planned Hong Kong listing, expected to raise about USD 5 bn, may slip to 2027 as Middle East disruptions weigh on crop and fertilizer markets and regulatory scrutiny of its seeds business extends the approval process. The Sinochem-controlled firm had previously considered raising up to USD 10 bn. (Reuters)

Record consumer defaults complicate China stimulus. Chinese household non-performing loans rose more than 20% to RMB 2.22 tn in 2025, equivalent to 1.6% of GDP, while short-term household lending contracted 7% in June. Banks are tightening credit standards despite Beijing’s efforts to promote borrowing, limiting the effectiveness of consumption stimulus (Reuters)

European import fees pressure Shein’s IPO valuation. Shein is targeting a USD 40-50 bn Hong Kong valuation, but investors may demand closer to USD 30 bn after the EU introduced a EUR 3 fee per customs category on low-value e-commerce parcels. Europe generates about one-third of Shein’s revenue, making the tariff-like charge a material risk to 2026 sales and margins (Reuters)

Asia ex. China

BOJ tightening hurts almost half of Japanese companies. A Reuters survey found 49% of companies reported negative effects from rate increases, while only 5% benefited after the BOJ lifted its policy rate to 1%. Yen weakness was negative for 55% of respondents, and most companies viewed a rate above 1.25%-1.5% as increasingly restrictive for investment (Reuters)

Bank of Korea begins tightening cycle. The BOK raised its policy rate by 25 bps to 2.75%, its first increase in three-and-a-half years, and signalled further tightening as semiconductor-led growth fuels inflation. The bank expects GDP growth to materially exceed its previous 2.6% forecast, with most analysts anticipating another hike this year (Reuters)

Korea curbs leveraged ETFs after chip selloff. South Korea will suspend new single-stock leveraged ETF listings, raise required deposits to KRW 30 mn from KRW 10 mn and increase the minimum trade to 20 shares after the products amplified volatility. The KOSPI fell 6.4% as SK Hynix (000660 KS -9.5%); Samsung Electronics (005930 KS -7.31%) sold off, while the won strengthened 0.7% following the BOK rate increase (Reuters)

BHP workers approve further strike action. Electrical workers at BHP’s (BHP LN -4.3%) Port Hedland operations voted 97.5% in favour of stoppages lasting from 30 minutes to 24 hours after wage and employment-condition talks stalled. The port handles approximately USD 80 mn of iron ore daily, raising potential export-disruption risks (Reuters)

EMEA and Others

Middle East caution caps European gains. The Stoxx 600 edged up 0.16%, while Germany’s DAX and France’s CAC 40 fell 0.34% and 0.05% respectively, while the UK’s FTSE 100 gained +0.54%, as strong earnings were offset by geopolitical concerns. ASML (ASML NA +3.16%) advanced after strong results, while STMicroelectronics (STMPA FP -4.91%) and BE Semiconductor (BESI BA -3.20%) declined. (Reuters)

Energy drives strongest European earnings growth in three years. STOXX 600 firms are expected to report 16.7% 2Q earnings growth, but the rate falls to 6.4% excluding energy, where profits are forecast to rise more than 125%. Higher oil and gas prices following Strait of Hormuz disruptions account for much of the upgrade. (Reuters)

BMW cost cuts deepen amid tariffs and weak margins. BMW (BMW GR -0.1%) appointed Dorothea von Boxberg as HR chief as it accelerates restructuring after cutting its profit outlook and forecasting margins as low as 1%. Chinese competition, the electric-vehicle transition, US tariffs and Iran-related uncertainty are increasing pressure on German automakers (Reuters)

Adidas wins World Cup visibility battle. Adidas (ADS GR -0.05%) supplies both finalists, Argentina and Spain, while none of Nike’s (NKE) 12 sponsored teams reached the final. Nike shares have lost nearly one-third YTD, while Adidas increased its footwear-market share to 19.2% in June from 16.0% a year earlier (Reuters)

Merck wins approval for oral cholesterol drug. Merck (MRK GR -1.58%) received FDA approval for Lipfendra, the first oral PCSK9 inhibitor, after trials showed an almost 60% reduction in LDL cholesterol. The USD 315-a-month treatment could generate peak sales of about USD 5 bn by 2034 (Reuters)

European electric-vehicle demand accelerates. Battery-electric registrations reached 1.24 mn in 1H26, up 33.7% year on year, while June sales increased 39.5% to 275,060 units. Fully electric vehicles captured 25.6% of the 17 tracked European markets as subsidies and higher petrol prices supported adoption (Reuters)

TRADERS’ CORNER

Source: TradingView |

| Xpeng (9868.HK)

|

Our Technical View

The upward movement has accelerated following a successful rebound off the horizontal support and a subsequent breach of the recent price high, solidifying a higher-high and higher-low configuration.

The RSI is climbing steadily above its neutral threshold.

This indicates a strong technical probability for continued upward momentum.

Source: TradingView |

| China Tobacco (6055.HK)

|

Our Technical View

Price has successfully validated a baseline support and forced a breakout above its resistance peak.

The RSI is scaling steadily into the dominant buying regime above the 50 threshold.

Backed by this active demand insulation and institutional accumulation underneath the tape, the technical layout projects a high probability of a continuation higher.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.