Overnight Markets

Today’s Must-Know News

AI selloff weighs on Wall Street. S&P 500 slipped 0.05% Friday as semiconductor stocks (SOXX -5.64%) fell on AI spending concerns, offsetting gains in Apple (AAPL +3.14%) and Moderna (MRNA +12.59%). S&P 500 equal weight index (SPW +0.88%) rose. SpaceX (SPCX +0.15%) edged higher ahead of its Russell index inclusion, with Nasdaq 100 entry on July 7 expected to drive USD4.3bn of passive ETF inflows. S&P Global said Samsung (005930 KS -5.70%) & SK Hynix (000660 KS -8.13%) will unveil AI investment plans today, with Samsung expected to pledge KRW1,000tn (USD648bn) for domestic investment over the next decade. SOXX is our Trading Buy.

Prime Day spending tops expectations. US online spending across all retailers (WMT -0.08%; TGT +0.59%) reached a record USD26.4bn during Amazon's (AMZN +2.5%) four-day Prime Day event, beating Adobe's USD26.3bn forecast and rising 9.3% yoy. AMZN & WMT are our Core Recommendations.

China remains Nike's key overhang in 4Q earnings (Jun 30). Nike (NKE -0.37%) previously guided for a roughly 20% yoy decline in Greater China 4QFY26 sales with weakness expected to persist into FY2027 as it cuts shipments and clears inventory. NKE is our Trading Buy.

Trader's Corner (Details on Page 6-7) | |||

Last Close | Support | Resistance | |

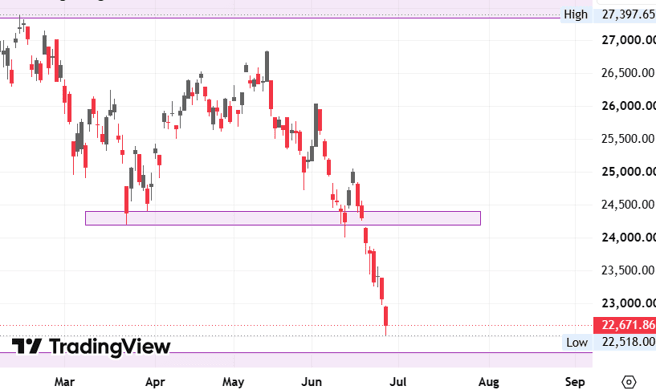

| Hang Seng Index | 22,671.86 | 21,710 / 19,740 | 23,565 / 24,310 |

| Hang Seng Tech Index | 4,255.59 | 4,170 / 3,615 | 4,500 / 4,620 |

Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 2697.HK | TH Medical-B | Healthcare | Jun 30 |

| 3952.HK | Laifual | Industrials | Jun 30 |

| 6715.HK | XunLong Scitech | Consumer Staples | Jun 30 |

| 6915.HK | Jiangxi Bio | Healthcare | Jun 30 |

| 0668.HK | Anker | Technology | Jul 2 |

| 2667.HK | Tong Ren Tang Care | Healthcare | Jul 7 |

| 1770.HK | DKE | Technology | Jul 8 |

| 6880.HK | Momenta-W | Technology | Jul 8 |

| 7656.HK | Reconova | Technology | Jul 8 |

| 7687.HK | Eacon | Consumer Disc. | Jul 8 |

| 8090.HK | Baogai | Industrials | Jul 8 |

| 9971.HK | Basic Semi | Technology | Jul 8 |

Americas

Trump escalates tariff threat. President Trump threatened a 100% tariff on imports from any country that imposes a digital services tax on US companies, saying the measure would override existing trade agreements, as France refused to scrap its levy on US tech firms. The warning comes despite the EU cutting tariffs on US goods to meet Trump's July 4 deadline under the US-EU trade deal. Separately, the US Supreme Court is set to rule this week on whether Trump can temporarily remove Fed Governor Lisa Cook. (Reuters / Bloomberg)

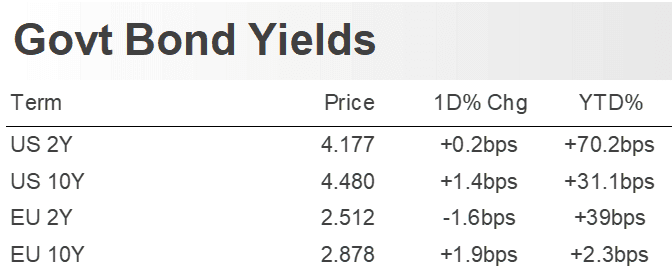

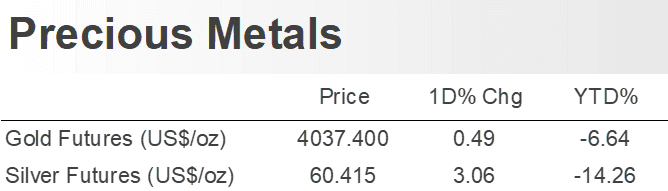

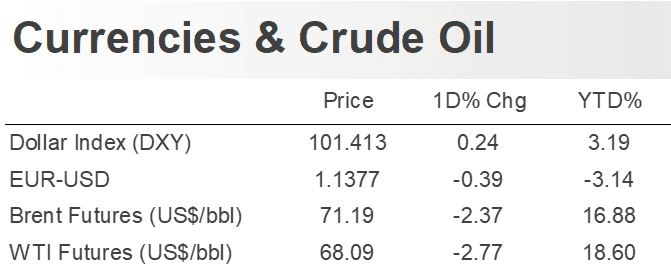

Fed and jobs data in focus. Most economists expect the Fed to keep rates unchanged through end-2026 despite markets pricing in two hikes, with investors now focused on Thursday's June payrolls report for clues on whether a strong labour market could reinforce expectations for higher rates. However, easing oil prices have reduced inflation concerns tied to the Middle East conflict. Energy (XLE -0.46%) shares fell Friday. Gold (XAU +1.54%) gained as the dollar (DXY -0.07%) weakened. (Reuters) XLE is our Core Recommendation.

SpaceX eyes mobile partnership. SpaceX (SPCX +0.15%) and Charter Communications (CHTR +3.08%) have reportedly held executive-level talks on a consumer mobile service partnership that could help SpaceX expand into direct-to-consumer wireless offerings by leveraging Charter's ground-based network infrastructure. (Bloomberg)

Meta eyes prediction markets. Meta (META +1.36%) is exploring partnerships with Polymarket and Kalshi as it develops its Arena prediction app, which is being tested internally and could be integrated into Facebook and Messenger. (Bloomberg) META is our Core Recommendation.

AI capacity constraints hit Meta. Alphabet (GOOGL -1.84%) as reportedly capped Meta's (META +1.36%) access to Gemini AI models due to capacity constraints, prompting Meta to ration AI usage & accelerate deployment of its Muse Spark model. (Bloomberg) META is our Core Recommendation; GOOGL is our Trading Buy.

Chevron expands AI power push. Chevron (CVX -0.69%) is exploring additional US data center power projects with Microsoft (MSFT +5.71%) and other customers after signing its 2.67GW Project Kilby in West Texas. Project Kilby is due for a final investment decision by year-end. (Bloomberg) MSFT is our Core Recommendation; CVX is our Trading Buy.

Microsoft faces Italy probe. Microsoft (MSFT +5.71%) is under investigation by Italy's antitrust regulator over alleged unfair practices tied to higher-priced Microsoft 365 subscriptions after integrating AI tools Copilot and Designer, with regulators alleging consumers were not adequately informed before being moved to costlier plans. (Reuters) MSFT is our Core Recommendation.

US delays GPT-5.6. OpenAI postponed GPT-5.6's public launch after the US requested early access, limiting initial availability to vetted partners while officials review security risks. OpenAI expects the delay to be temporary as it works on an AI release framework with the Trump administration. (Reuters)

US eases Anthropic restrictions. Anthropic will restore access to its Claude Mythos 5 AI model for more than 100 trusted US organizations after the government partially reversed an earlier suspension over national security concerns. Meanwhile, the broader public releases of Anthropic's Fable 5 and OpenAI's GPT-5.6 remain restricted. (Reuters)

Board fight ends. Lululemon (LULU +4.92%) shareholders approved the firm’s board slate, completing a settlement with founder Chip Wilson that adds three independent directors and clears the way for incoming CEO Heidi O'Neill to lead the brand's turnaround. The truce comes as Lululemon faces weaker sales, margin pressure from tariffs and discounting, and intensifying competition. (Reuters)

Verizon dominates FCC spectrum auction. Verizon (VZ +1.02%) bid nearly USD 3.2 bn to secure most wireless spectrum licenses in an FCC auction that raised about USD 3.5 bn, while T-Mobile (TMUS +0.61%) bid USD 278 mn, AT&T (T +1.34%) USD 121 mn and SpaceX (SPCX +0.15%) USD 8.5 mn. (Reuters)

Greater China

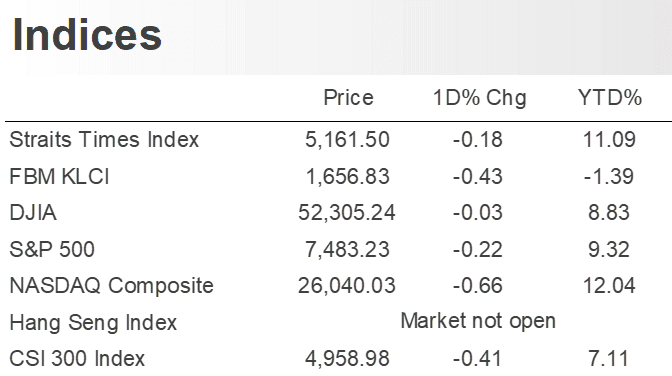

AI selloff hits China and Hong Kong. HSI fell by 1.76% and CSI 300 decreased by 3.03% slumped as the global AI selloff intensified, with the Hang Seng Index posting its worst weekly decline since April 2025, led by Alibaba (9988.HK -5.79%), Tencent (0700.HK -2.28%) and other AI-related technology stocks. Investors cited concerns over AI valuations, the Fed's hawkish stance and weak Chinese consumer demand weighing on earnings outlook. (SCMP)

China May industrial profit growth slows. China's May industrial profits rose 21.1% yoy, easing from April's 24.7% gain and marking the first slowdown since November, as weak domestic demand offset stronger exports and higher producer prices. (Bloomberg)

Tencent targets overseas visitors. Tencent (0700.HK -2.28%) is testing TenPayGo, a one-stop app for overseas visitors that integrates mobile payments, travel, dining and shopping services, as China seeks to capitalize on rising inbound travel. (Bloomberg) 0700.HK is our Core Recommendation.

Chinese EVs enter Canada under trade deal. Geely (0175.HK -0.93%) will ship its first Lotus EVs to Canada in July under a Carney-Xi agreement allowing up to 49,000 Chinese EVs annually at reduced tariffs, while BYD (1211.HK -4.47%) and Chery (9973.HK +2.01%) are expected to complete entry procedures later this year. China's ambassador also said bilateral trade could more than double. (Reuters) 0175.HK is our Core Recommendation.

Apple seeks CXMT chip approval. Apple (AAPL +3.14%) is reportedly lobbying the Trump administration for approval to buy memory chips from blacklisted Chinese chipmaker ChangXin Memory Technologies to ease rising component costs, while seeking assurances the firm will not face stricter US export restrictions. (Bloomberg/FT)

BYD deepens provincial ties. BYD (1211.HK -4.47%) Chairman Wang Chuanfu has met leaders from at least five Chinese provinces since March, strengthening ties with regions that host the firm’s vehicle manufacturing and supply chain operations. (Bloomberg)

China warns EU on trade ties. China said it could withstand a further deterioration or even a freeze in trade relations with the EU if negotiations are treated as a formality, ahead of trade talks in Brussels this week over tariffs and the bloc's widening trade imbalance with Beijing. China also argued European influence is waning as Chinese firms increasingly prioritize other markets. (Bloomberg)

Hong Kong IPO momentum stays selective. Apple supplier Lingyi iTech (1688.HK -4.62%) fell below its IPO price on its Hong Kong debut despite raising HKD8.3bn, while smaller listings including SG Micro (3661.HK +47.07%), Circuit Fabology (9630.HK +103.77%), WengeAI (1956.HK +84.02%) and Keytop Parking (2272.HK +203.92%) surged. Hong Kong IPOs and secondary listings have raised USD21.6bn so far this year, up 51% yoy. (Reuters)

Asia ex. China

Firmus lands Nvidia AI data center deal. Australia's Firmus Technologies will build its first Indonesian data center with Nvidia (NVDA -1.64%) and Singapore-based DayOne, developing a 360MW AI campus in Batam, with the partnership expected to generate USD25bn-30bn of committed offtake agreements over its first six years. (Bloomberg) NVDA is our Core Recommendation.

SGX SMID buybacks signal value. SGX-listed SMID companies under coverage repurchased about SGD 5.6 million of shares in June, led by Food Empire (FEH SP -1.27%), which bought back SGD 2.2 mn worth of stock near multi-month lows. The aggressive buybacks suggest management sees intrinsic value above current market prices, with top SMID picks including Food Empire, ValueMax, Pan-United and UMS Integration. (UOB Kay Hian Institutional Research)

MISC's growth strategy remains intact. MISC (MISC MK +1.28%) continues to strengthen its petroleum segment through a higher term-charter mix while accelerating decarbonisation and expanding profitable new energy businesses. The sale of Seri Balhaf and Seri Balqis should cap downside risks for its LNG carrier business. Maintain BUY with a target price of MYR 9.50. (UOB Kay Hian Institutional Research)

EMEA and Others

European tech drags markets. STOXX Europe 600 fell 0.68% Friday as AI-related technology stocks tracked the global semiconductor selloff, with chipmakers and AI suppliers leading declines. The UK's FTSE 100 declined 0.21%, France's CAC 40 retreated 0.55% and while Germany's DAX fell 1.29%. Zalando (ZAL GR -6.74%) fell after Germany's BaFin launched an accounting probe. Volkswagen (VOW GR -3.94%) rose on reports it plans to cut up to 100,000 jobs over the next few years. (Reuters)

Volkswagen weighs China production shift. Volkswagen (VOW GR -3.94%) could shift production of China-developed models to Germany to improve plant utilization and protect jobs, Lower Saxony, the automaker's 20% voting shareholder, said. Volkswagen prepares to discuss plans on July 9 to cut up to 100,000 jobs and close four German plants, which is expected to face strong union and political opposition. (Reuters)

Mercedes steps up cost cuts. Mercedes-Benz (MBG GR -3.02%) plans longer working hours for the same pay, delayed bonus payments and some job relocations abroad as it intensifies cost-cutting amid weak demand, higher costs and US tariffs. (Reuters)

Adidas faces ball design challenge. Adidas (ADS GR +1.83%) is defending the design rights for its Trionda World Cup ball after a German designer challenged its EU registration, with the EU Intellectual Property Office set to receive Adidas' response by August. (FT)

TRADERS’ CORNER

Source: TradingView Source: TradingView | Hang Seng Index

Last Price: 22,671.86 Support: 21,710 (-4.3%)/ 19,740 (-12.9%) Resistance: 24,315 (+3.9%)/ 25,050 (+7.2%) |

Our Technical View

Weekly Chart: The price has decisively violated its previous low support zone, with a bearish candle confirming a structural breakdown. This downside expansion is reinforced by the MACD that remains firmly entrenched in a negative regime and accelerates lower. The HSI may experience a brief counter-trend relief rally in the coming week, which would likely serve as a mechanical retest of overhead supply before initiating the next primary wave of downward expansion.

Daily Chart: This index is approaching a support floor following a sharp vertical plunge that invalidated its previous low. With the RSI compressed within its oversold boundary, immediate selling momentum is stretched, setting the stage for a near-term technical bounce. Barring a major structural reversal, any corrective rebound in the coming week is expected to face heavy overhead supply at the support-turned-resistance zone, establishing a classic entry pivot for the next structural leg lower.

Source: TradingView Source: TradingView | Hang Seng Tech Index

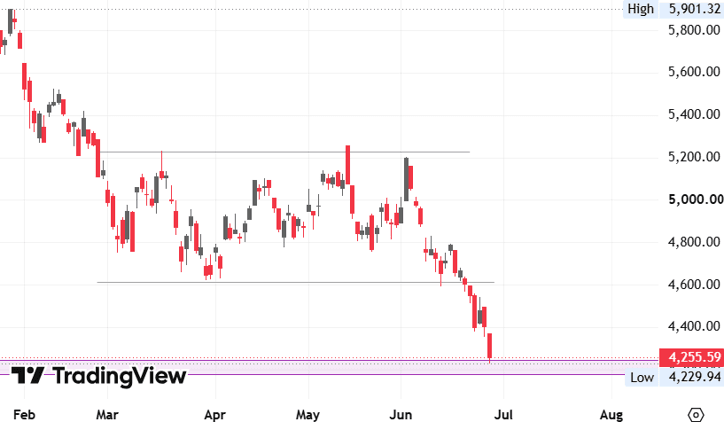

Last Price: 4,255.59 Support: 4,170 (-2.0%)/ 3,615 (-15.0%) Resistance: 4,500 (+5.7%)/ 4,620 (+8.6%) |

Our Technical View

Weekly Chart: This index has finally breached the lower boundary of its multi-week consolidation flag. Underlying liquidation pressure is accelerating, heavily reinforced by a widening MACD within a strongly bearish regime. Backed by this macro structural shift, the technical framework firmly favours sustained downside extensions toward the weekly flagpole target in the weeks ahead.

Daily Chart: Monday’s structural breakdown of the flag pattern officially unlocked deep selling pressure, driving the MACD into heavily oversold territory far beneath its zero line. Given the velocity of this localised liquidation, this index is primed for a brief, technical bounce in the coming week. However, barring a structural reclamation of the breakout zone, any corrective rebound should be viewed as an entry window for sellers ahead of the next primary leg lower.

Today’s Must-Know News

AI selloff weighs on Wall Street. S&P 500 slipped 0.05% Friday as semiconductor stocks (SOXX -5.64%) fell on AI spending concerns, offsetting gains in Apple (AAPL +3.14%) and Moderna (MRNA +12.59%). S&P 500 equal weight index (SPW +0.88%) rose. SpaceX (SPCX +0.15%) edged higher ahead of its Russell index inclusion, with Nasdaq 100 entry on July 7 expected to drive USD4.3bn of passive ETF inflows. S&P Global said Samsung (005930 KS -5.70%) & SK Hynix (000660 KS -8.13%) will unveil AI investment plans today, with Samsung expected to pledge KRW1,000tn (USD648bn) for domestic investment over the next decade. SOXX is our Trading Buy.

Prime Day spending tops expectations. US online spending across all retailers (WMT -0.08%; TGT +0.59%) reached a record USD26.4bn during Amazon's (AMZN +2.5%) four-day Prime Day event, beating Adobe's USD26.3bn forecast and rising 9.3% yoy. AMZN & WMT are our Core Recommendations.

China remains Nike's key overhang in 4Q earnings (Jun 30). Nike (NKE -0.37%) previously guided for a roughly 20% yoy decline in Greater China 4QFY26 sales with weakness expected to persist into FY2027 as it cuts shipments and clears inventory. NKE is our Trading Buy.

Trader's Corner (Details on Page 6-7) | |||

Last Close | Support | Resistance | |

| Hang Seng Index | 22,671.86 | 21,710 / 19,740 | 23,565 / 24,310 |

| Hang Seng Tech Index | 4,255.59 | 4,170 / 3,615 | 4,500 / 4,620 |

Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 2697.HK | TH Medical-B | Healthcare | Jun 30 |

| 3952.HK | Laifual | Industrials | Jun 30 |

| 6715.HK | XunLong Scitech | Consumer Staples | Jun 30 |

| 6915.HK | Jiangxi Bio | Healthcare | Jun 30 |

| 0668.HK | Anker | Technology | Jul 2 |

| 2667.HK | Tong Ren Tang Care | Healthcare | Jul 7 |

| 1770.HK | DKE | Technology | Jul 8 |

| 6880.HK | Momenta-W | Technology | Jul 8 |

| 7656.HK | Reconova | Technology | Jul 8 |

| 7687.HK | Eacon | Consumer Disc. | Jul 8 |

| 8090.HK | Baogai | Industrials | Jul 8 |

| 9971.HK | Basic Semi | Technology | Jul 8 |

Americas

Trump escalates tariff threat. President Trump threatened a 100% tariff on imports from any country that imposes a digital services tax on US companies, saying the measure would override existing trade agreements, as France refused to scrap its levy on US tech firms. The warning comes despite the EU cutting tariffs on US goods to meet Trump's July 4 deadline under the US-EU trade deal. Separately, the US Supreme Court is set to rule this week on whether Trump can temporarily remove Fed Governor Lisa Cook. (Reuters / Bloomberg)

Fed and jobs data in focus. Most economists expect the Fed to keep rates unchanged through end-2026 despite markets pricing in two hikes, with investors now focused on Thursday's June payrolls report for clues on whether a strong labour market could reinforce expectations for higher rates. However, easing oil prices have reduced inflation concerns tied to the Middle East conflict. Energy (XLE -0.46%) shares fell Friday. Gold (XAU +1.54%) gained as the dollar (DXY -0.07%) weakened. (Reuters) XLE is our Core Recommendation.

SpaceX eyes mobile partnership. SpaceX (SPCX +0.15%) and Charter Communications (CHTR +3.08%) have reportedly held executive-level talks on a consumer mobile service partnership that could help SpaceX expand into direct-to-consumer wireless offerings by leveraging Charter's ground-based network infrastructure. (Bloomberg)

Meta eyes prediction markets. Meta (META +1.36%) is exploring partnerships with Polymarket and Kalshi as it develops its Arena prediction app, which is being tested internally and could be integrated into Facebook and Messenger. (Bloomberg) META is our Core Recommendation.

AI capacity constraints hit Meta. Alphabet (GOOGL -1.84%) as reportedly capped Meta's (META +1.36%) access to Gemini AI models due to capacity constraints, prompting Meta to ration AI usage & accelerate deployment of its Muse Spark model. (Bloomberg) META is our Core Recommendation; GOOGL is our Trading Buy.

Chevron expands AI power push. Chevron (CVX -0.69%) is exploring additional US data center power projects with Microsoft (MSFT +5.71%) and other customers after signing its 2.67GW Project Kilby in West Texas. Project Kilby is due for a final investment decision by year-end. (Bloomberg) MSFT is our Core Recommendation; CVX is our Trading Buy.

Microsoft faces Italy probe. Microsoft (MSFT +5.71%) is under investigation by Italy's antitrust regulator over alleged unfair practices tied to higher-priced Microsoft 365 subscriptions after integrating AI tools Copilot and Designer, with regulators alleging consumers were not adequately informed before being moved to costlier plans. (Reuters) MSFT is our Core Recommendation.

US delays GPT-5.6. OpenAI postponed GPT-5.6's public launch after the US requested early access, limiting initial availability to vetted partners while officials review security risks. OpenAI expects the delay to be temporary as it works on an AI release framework with the Trump administration. (Reuters)

US eases Anthropic restrictions. Anthropic will restore access to its Claude Mythos 5 AI model for more than 100 trusted US organizations after the government partially reversed an earlier suspension over national security concerns. Meanwhile, the broader public releases of Anthropic's Fable 5 and OpenAI's GPT-5.6 remain restricted. (Reuters)

Board fight ends. Lululemon (LULU +4.92%) shareholders approved the firm’s board slate, completing a settlement with founder Chip Wilson that adds three independent directors and clears the way for incoming CEO Heidi O'Neill to lead the brand's turnaround. The truce comes as Lululemon faces weaker sales, margin pressure from tariffs and discounting, and intensifying competition. (Reuters)

Verizon dominates FCC spectrum auction. Verizon (VZ +1.02%) bid nearly USD 3.2 bn to secure most wireless spectrum licenses in an FCC auction that raised about USD 3.5 bn, while T-Mobile (TMUS +0.61%) bid USD 278 mn, AT&T (T +1.34%) USD 121 mn and SpaceX (SPCX +0.15%) USD 8.5 mn. (Reuters)

Greater China

AI selloff hits China and Hong Kong. HSI fell by 1.76% and CSI 300 decreased by 3.03% slumped as the global AI selloff intensified, with the Hang Seng Index posting its worst weekly decline since April 2025, led by Alibaba (9988.HK -5.79%), Tencent (0700.HK -2.28%) and other AI-related technology stocks. Investors cited concerns over AI valuations, the Fed's hawkish stance and weak Chinese consumer demand weighing on earnings outlook. (SCMP)

China May industrial profit growth slows. China's May industrial profits rose 21.1% yoy, easing from April's 24.7% gain and marking the first slowdown since November, as weak domestic demand offset stronger exports and higher producer prices. (Bloomberg)

Tencent targets overseas visitors. Tencent (0700.HK -2.28%) is testing TenPayGo, a one-stop app for overseas visitors that integrates mobile payments, travel, dining and shopping services, as China seeks to capitalize on rising inbound travel. (Bloomberg) 0700.HK is our Core Recommendation.

Chinese EVs enter Canada under trade deal. Geely (0175.HK -0.93%) will ship its first Lotus EVs to Canada in July under a Carney-Xi agreement allowing up to 49,000 Chinese EVs annually at reduced tariffs, while BYD (1211.HK -4.47%) and Chery (9973.HK +2.01%) are expected to complete entry procedures later this year. China's ambassador also said bilateral trade could more than double. (Reuters) 0175.HK is our Core Recommendation.

Apple seeks CXMT chip approval. Apple (AAPL +3.14%) is reportedly lobbying the Trump administration for approval to buy memory chips from blacklisted Chinese chipmaker ChangXin Memory Technologies to ease rising component costs, while seeking assurances the firm will not face stricter US export restrictions. (Bloomberg/FT)

BYD deepens provincial ties. BYD (1211.HK -4.47%) Chairman Wang Chuanfu has met leaders from at least five Chinese provinces since March, strengthening ties with regions that host the firm’s vehicle manufacturing and supply chain operations. (Bloomberg)

China warns EU on trade ties. China said it could withstand a further deterioration or even a freeze in trade relations with the EU if negotiations are treated as a formality, ahead of trade talks in Brussels this week over tariffs and the bloc's widening trade imbalance with Beijing. China also argued European influence is waning as Chinese firms increasingly prioritize other markets. (Bloomberg)

Hong Kong IPO momentum stays selective. Apple supplier Lingyi iTech (1688.HK -4.62%) fell below its IPO price on its Hong Kong debut despite raising HKD8.3bn, while smaller listings including SG Micro (3661.HK +47.07%), Circuit Fabology (9630.HK +103.77%), WengeAI (1956.HK +84.02%) and Keytop Parking (2272.HK +203.92%) surged. Hong Kong IPOs and secondary listings have raised USD21.6bn so far this year, up 51% yoy. (Reuters)

Asia ex. China

Firmus lands Nvidia AI data center deal. Australia's Firmus Technologies will build its first Indonesian data center with Nvidia (NVDA -1.64%) and Singapore-based DayOne, developing a 360MW AI campus in Batam, with the partnership expected to generate USD25bn-30bn of committed offtake agreements over its first six years. (Bloomberg) NVDA is our Core Recommendation.

SGX SMID buybacks signal value. SGX-listed SMID companies under coverage repurchased about SGD 5.6 million of shares in June, led by Food Empire (FEH SP -1.27%), which bought back SGD 2.2 mn worth of stock near multi-month lows. The aggressive buybacks suggest management sees intrinsic value above current market prices, with top SMID picks including Food Empire, ValueMax, Pan-United and UMS Integration. (UOB Kay Hian Institutional Research)

MISC's growth strategy remains intact. MISC (MISC MK +1.28%) continues to strengthen its petroleum segment through a higher term-charter mix while accelerating decarbonisation and expanding profitable new energy businesses. The sale of Seri Balhaf and Seri Balqis should cap downside risks for its LNG carrier business. Maintain BUY with a target price of MYR 9.50. (UOB Kay Hian Institutional Research)

EMEA and Others

European tech drags markets. STOXX Europe 600 fell 0.68% Friday as AI-related technology stocks tracked the global semiconductor selloff, with chipmakers and AI suppliers leading declines. The UK's FTSE 100 declined 0.21%, France's CAC 40 retreated 0.55% and while Germany's DAX fell 1.29%. Zalando (ZAL GR -6.74%) fell after Germany's BaFin launched an accounting probe. Volkswagen (VOW GR -3.94%) rose on reports it plans to cut up to 100,000 jobs over the next few years. (Reuters)

Volkswagen weighs China production shift. Volkswagen (VOW GR -3.94%) could shift production of China-developed models to Germany to improve plant utilization and protect jobs, Lower Saxony, the automaker's 20% voting shareholder, said. Volkswagen prepares to discuss plans on July 9 to cut up to 100,000 jobs and close four German plants, which is expected to face strong union and political opposition. (Reuters)

Mercedes steps up cost cuts. Mercedes-Benz (MBG GR -3.02%) plans longer working hours for the same pay, delayed bonus payments and some job relocations abroad as it intensifies cost-cutting amid weak demand, higher costs and US tariffs. (Reuters)

Adidas faces ball design challenge. Adidas (ADS GR +1.83%) is defending the design rights for its Trionda World Cup ball after a German designer challenged its EU registration, with the EU Intellectual Property Office set to receive Adidas' response by August. (FT)

TRADERS’ CORNER

| Source: TradingView | Hang Seng Index

Last Price: 22,671.86 Support: 21,710 (-4.3%)/ 19,740 (-12.9%) Resistance: 24,315 (+3.9%)/ 25,050 (+7.2%) |

Our Technical View

Weekly Chart: The price has decisively violated its previous low support zone, with a bearish candle confirming a structural breakdown. This downside expansion is reinforced by the MACD that remains firmly entrenched in a negative regime and accelerates lower. The HSI may experience a brief counter-trend relief rally in the coming week, which would likely serve as a mechanical retest of overhead supply before initiating the next primary wave of downward expansion.

Daily Chart: This index is approaching a support floor following a sharp vertical plunge that invalidated its previous low. With the RSI compressed within its oversold boundary, immediate selling momentum is stretched, setting the stage for a near-term technical bounce. Barring a major structural reversal, any corrective rebound in the coming week is expected to face heavy overhead supply at the support-turned-resistance zone, establishing a classic entry pivot for the next structural leg lower.

| Source: TradingView | Hang Seng Tech Index

Last Price: 4,255.59 Support: 4,170 (-2.0%)/ 3,615 (-15.0%) Resistance: 4,500 (+5.7%)/ 4,620 (+8.6%) |

Our Technical View

Weekly Chart: This index has finally breached the lower boundary of its multi-week consolidation flag. Underlying liquidation pressure is accelerating, heavily reinforced by a widening MACD within a strongly bearish regime. Backed by this macro structural shift, the technical framework firmly favours sustained downside extensions toward the weekly flagpole target in the weeks ahead.

Daily Chart: Monday’s structural breakdown of the flag pattern officially unlocked deep selling pressure, driving the MACD into heavily oversold territory far beneath its zero line. Given the velocity of this localised liquidation, this index is primed for a brief, technical bounce in the coming week. However, barring a structural reclamation of the breakout zone, any corrective rebound should be viewed as an entry window for sellers ahead of the next primary leg lower.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.