Overnight Markets

Today’s Must-Know News

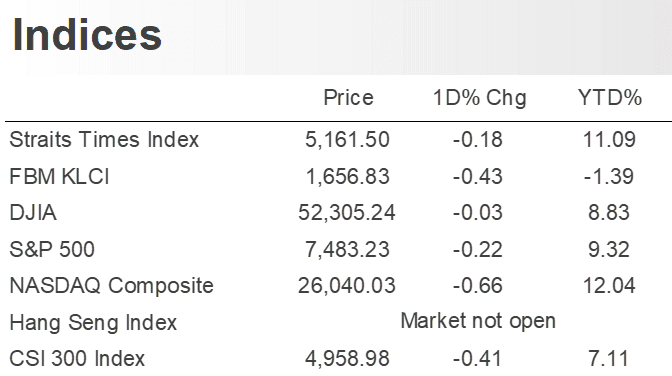

Wall Street rallies as Iran risk eases. S&P 500 futures were little changed, while S&P 500 gained 1.18% Monday as US-Iran hostilities eased. SpaceX (SPCX +7.15%) gained on Nasdaq 100 inclusion. Alphabet (GOOGL +4.82%) advanced on its first day as a Dow component, replacing Verizon (VZ -5.24%). Semis (SOXX +4.14%) rebounded alongside AI-chip investment headlines from Samsung Electronics (005930 KS -4.13%) and SK Hynix (000660 KS -2.89%), while Honeywell Aerospace (HONA -0.37%) slipped in its Nasdaq debut after spinning off from Honeywell (HON -6.41%). SOXX is our Trading Buy.

Lilly gets faster FDA review. Eli Lilly (LLY +1.81%) is among the firms that are selected for an FDA pilot to speed reviews of new US drug plants, lowering onshoring execution risk. The program also helps reduce tariff exposure as drugmakers expand domestic manufacturing. LLY is our Core Recommendation.

Nike earnings focus on China and tariffs. Nike (NKE +1.79%) reports after-market today (Tuesday), with investors watching China demand, tariff refunds and a 7.923% earnings-related implied move. Investors will also look for turnaround progress and reports Nike may halt partner online sales in China. NKE is our Trading Buy.

There will be no Wealth Daily July 1 (HK public holiday).

Trader’s Corner (Details on Page 7-8) | ||||

Ticker | Name | Rec. | Support Levels | Resistance Levels |

2228.HK | XtalPi | - | HK$6.68/$6.30 | HK$9.76/$10.51 |

9660.HK | Horizon Robotics | - | HK$3.60/$3.32 | HK$5.52/$6.20 |

CR = Core Recommendation; TB = Trading Buy | ||||

Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 0668.HK | Anker | Technology | Jul 2 |

| 2667.HK | Tong Ren Tang Care | Healthcare | Jul 7 |

| 1770.HK | DKE | Technology | Jul 8 |

| 6880.HK | Momenta-W | Technology | Jul 8 |

| 7656.HK | Reconova | Technology | Jul 8 |

| 7687.HK | Eacon | Consumer Disc. | Jul 8 |

| 8090.HK | Baogai | Industrials | Jul 8 |

| 9971.HK | Basic Semi | Technology | Jul 8 |

| 0537.HK | Rigol | Industrials | Jul 9 |

| 1377.HK | Dtech | Industrials | Jul 9 |

| 2475.HK | Luxshare ICT | Technology | Jul 9 |

| 2249.HK | Nexchip | Technology | Jul 10 |

| 2523.HK | EKH | Industrials | Jul 13 |

Americas

Supreme Court protects Fed independence. The US Supreme Court rejected President Trump’s bid to fire Fed Governor Lisa Cook, ruling she was not given required procedural protections and reinforcing that Fed governors can only be removed “for cause.” The court separately expanded presidential power to dismiss leaders of other agencies, raising broader executive-authority risk while leaving Fed independence intact. (Reuters)

Memory makers face DRAM lawsuit. Samsung (005930 KS -4.13%), SK Hynix (000660 KS -2.89%) and Micron (MU +1.14%) were sued in California over claims they restricted commodity DRAM supply during the shift to HBM, lifting prices about 700% over four years. Plaintiffs seek class-action status and treble damages. (Yahoo Finance) MU is our Trading Buy.

Taiwan chip-smuggling probe widens. Super Micro Computer (SMCI -8.1%) plunged Monday after Taiwan authorities raided the firm’s local office as part of an investigation into alleged smuggling of Nvidia (NVDA +1.27%) chips into China using Super Micro servers. Taiwan considering tougher export controls and potential criminal penalties to align more closely with US restrictions. (Bloomberg) NVDA is our Core Recommendation.

Banks expand funding channels for AI debt. AI-related borrowing is approaching 15% of US investment-grade issuance this year as Amazon (AMZN +3.2%) and Alphabet (GOOGL +4.82%) tap global bond markets to fund chips, cloud and data-center spending. Hyperscaler capex is estimated at about USD 725 bn this year, while bankers are using structures such as data-center lease-backed notes to broaden demand and reduce market-saturation risk. (Reuters) AMZN is our Core Recommendation; GOOGL is our Trading Buy.

Rocket Lab takes on SpaceX with Iridium deal. Rocket Lab (RKLB +15.93%) agreed to buy Iridium (IRDM +25.44%) for USD8bn, adding licensed spectrum, a global satellite network and over 2.5 mn subscribers to expand beyond launch services. Iridium holders will receive USD27 cash plus Rocket Lab shares, while Deutsche Bank (DBK GR +0.59%) and Wells Fargo (WFC -0.42%) have committed a USD 3.6 bn bridge loan for the cash portion. (Reuters)

Uber resets Phoenix robotaxi strategy. Uber (UBER -0.92%) and Alphabet’s Waymo (GOOGL +4.82%) ended their limited Phoenix robotaxi pilot of just over a dozen vehicles, with Waymo moving the cars back to its own app fleet while remaining on Uber in Austin and Atlanta. Uber is preparing a new Phoenix autonomous-vehicle partnership as Waymo faces scrutiny after recalling nearly 3,900 US robotaxis over software risk around closed freeway construction zones. (Reuters) GOOGL is our Trading Buy.

Tesla deliveries eyed as FSD update boosts shares. Tesla (TSLA +8.46%) is expected to report its 2Q vehicle deliveries around July 2, with Bloomberg consensus at 396,466 vehicles, compared with Tesla IR consensus estimates of 406,024 (average) and 408,609 (median). Shares jumped Monday, its biggest one-day gain in more than a year, after the firm began early access to version 14 "lite" of its Full Self-Driving software for select older vehicles equipped with Hardware 3. (Reuters)

Applied Materials leads chip rebound. Applied Materials (AMAT +10.82%) shares jumped Monday as analysts lifted price targets. KeyBanc raised its target to USD750 from USD 550 and Cantor Fitzgerald lifted its target to USD 850 from USD 650, though the stock’s move above key trend gauges points to late-stage momentum rather than an early breakout. (Benzinga)

Verizon and BT combine enterprise assets. Verizon (VZ -5.24%) and BT (BT/A LN +0.62%) agreed to merge their international enterprise operations into a 50:50 JV with USD 4 bn of combined annual revenue, with Verizon paying BT USD 625 mn to equalise the transaction. The venture will serve over 3,000 multinational customers across more than 180 countries. (Reuters)

Comcast rallies on NBCUniversal spinoff. Comcast (CMCSA +4.53%) will split into two listed companies via a spinoff of NBCUniversal and Sky, separating its broadband, wireless and business-services arm from its media, studios, Peacock and theme-parks assets. Mike Cavanagh will lead NBCUniversal, former CFO Michael Angelakis will return as Comcast CEO and analysts see NBCUniversal as a potential takeover target. (Reuters)

Digital Realty expands Northern Virginia stake. Digital Realty (DLR -1.25%) will buy larger stakes in three Northern Virginia data centers from Blackstone (BX -0.45%) in a USD 3.5 bn cash-and-stock deal, strengthening its position in the world’s largest data-center market. The deal includes USD 1.2 bn cash and USD 2.3 bn in shares, and is expected to lift Core FFO per share in 2027 and 2028 as development completes and rents begin. (Reuters)

Greater China

China and Hong Kong stocks broaden rally. CSI300 rose 1.21% and HSI gained 1.57% on Monday, led by healthcare, consumer and chip shares as investors rotated beyond AI supply-chain names. The HSTech Index gained 3.23%, with sentiment helped by CXMT’s reported RMB 20 bn-plus memory supply deal with Tencent (0700.HK +2.04%). (Reuters)

CXMT secures Tencent memory deal. China’s ChangXin Memory Technologies signed a multi-year DRAM supply agreement with Tencent (0700.HK +2.04%) worth more than RMB 20 bn, or about USD 2.94 bn, ahead of its planned RMB 29.5 bn Shanghai STAR Market IPO. UBS estimates contract prices rose about 95% qoq in 1Q26 and the global memory upcycle could last until at least late 2027. (Reuters) 0700.HK is our Core Recommendation.

PBOC easing lifts hopes for lower borrowing costs. China's central bank set the rate on its new overnight liquidity tool at 1.25%, below market expectations and the policy rate, after injecting RMB 300 bn via overnight reverse repos to ease half-year funding conditions. The move signalled a more accommodative policy stance and raised expectations for a potential Loan Prime Rate cut as early as next month, supporting lower market borrowing costs. (Reuters)

EU-China trade reset targeted. The EU and China set an October deadline to make progress on trade disputes covering the EU’s widening deficit, Chinese export controls, intellectual property and WTO reforms. Brussels said it remains open for business but needs to defend its industrial base and secure a more level playing field, with both sides also planning a joint platform to monitor trade flows. (Bloomberg)

Baidu chip unit eyes USD 50 bn IPO. Baidu’s (BIDU +7.64%; 9888.HK +5.62%) AI chip unit Kunlunxin is reportedly targeting a Hong Kong IPO at a USD 50 bn valuation, supporting China’s tech self-reliance push. Kunlunxin mainly supplies Baidu, while Tencent (0700.HK +2.04%) is reportedly a customer and ByteDance is considering its chips. (Reuters) 0700.HK is our Core Recommendation.

Nexchip taps Hong Kong market. China’s Nexchip Semiconductor (688249 SZ +7.64%; 2249 HK) is seeking to raise up to HKD 6.98 bn, or about USD 890 mn, through a Hong Kong share sale. The deal adds to China’s semiconductor capital-raising pipeline as domestic chipmakers continue to fund capacity expansion. (Reuters)

Luxshare taps Hong Kong market. Apple supplier Luxshare Precision Industry (002475.SZ -3.97%; 2475.HK), best known for assembling AirPods, is seeking to raise up to USD 3.1 bn through a Hong Kong share sale, according to an exchange filing. The deal would add to Hong Kong’s equity fundraising pipeline. (Reuters)

China expands export curbs, deepens Japan trade tensions. China's Ministry of Commerce added 20 Japanese organisations, including Mitsubishi Heavy Industries (7011 JP +2.35%), Mitsubishi Electric (6503 JP +0.03%) and Kawasaki Heavy Industries (7012 JP +2.56%), to its export-control list, expanding restrictions on dual-use goods. The measures deepen trade tensions with Prime Minister Sanae Takaichi's government and bar overseas entities from supplying listed firms with China-origin dual-use technology. (Reuters)

Asia ex. China

Australia targets Amazon Prime terms. Australia’s competition regulator sued Amazon’s local unit (AMZN +3.2%) over Prime subscription terms it says unfairly allowed the firm to add advertising to Prime Video. The case raises regulatory risk around subscription contract changes and streaming monetisation practices in Australia. (Reuters) AMZN is our Core Recommendation.

Apple supplier leak exposes iPhone 18 Pro details. Apple (AAPL -0.72%) supplier Tata Electronics suffered a dark-web data leak exposing iPhone 18 Pro supplier lists, component mappings and drop-test photos, potentially aiding rivals and counterfeiters. Counterpoint estimates India will produce 26% of global iPhones in 2026. (Reuters)

AirTrunk nears Singapore IPO filing. Blackstone (BX -0.45%) -backed AirTrunk is reportedly close to filing confidentially for a Singapore REIT IPO that could raise about USD 1.5 bn, potentially the city’s biggest listing since Netlink NBN Trust’s USD 1.7 bn deal in 2017. (Bloomberg)

Data centre pipeline strengthens Keppel DC REIT growth. Keppel DC REIT (KDCREIT SP +0.44%) said sponsor Keppel has built a 1.0GW data centre pipeline across Singapore, Japan, South Korea and Australia, with potential acquisitions from 2028 supporting long-term growth. The termination of the SGD 79.2 mn M1 NetCo bond divestment will also preserve a stable SGD 11 mn annual income stream, implying an IRR of 9%. (Reuters)

EMEA and Others

European equities edge higher on tech rebound. STOXX Europe 600 gained 0.04% Monday, supported by technology and energy as AI-linked names recovered from last week’s selloff. UK's FTSE 100, France's CAC 40 and while Germany's DAX retreated by 0.23%, 0.21% and 0.18% respectively. ASML (ASML NA +2.14%) and Prosus (PRX NA +2.43%) shares rose, while banks lagged as sovereign yields rebounded ahead of the ECB forum. (Reuters)

Maersk lifts 2026 outlook. Maersk (MAESKB DC -0.28%) raised its 2026 EBITDA guidance to USD 8-10 bn from USD 4.5-7 bn, citing stronger container-market demand, particularly in Asia. The shipping group also lifted adjusted EBIT guidance to USD 2-4 bn, pointing to a firmer freight backdrop after a volatile cycle for global container carriers. (Reuters)

LVMH and Accor target AI wealth boom. LVMH (MC FP -0.7%) and Accor’s (AC FP -0.08%) Orient Express venture is targeting AI-created ultra-rich customers through luxury experiences, led by its first giant yacht. Accor said high-end experience spending may grow 9-11% this year vs. 1-4% for personal luxury goods, with Orient Express assets estimated at about EUR1bn. (Reuters)

Prosus profit jumps on M&A. Prosus (PRX NA +2.43%) reported FY adjusted EBITDA up 84% to USD 1.3 bn and revenue up 57% to USD 9.7 bn after about USD 8.5 bn of acquisitions. The group plans to use Just Eat Takeaway.com to expand in Europe across food delivery, groceries and fintech, while developing an AI shopping assistant. (Reuters)

TRADERS’ CORNER

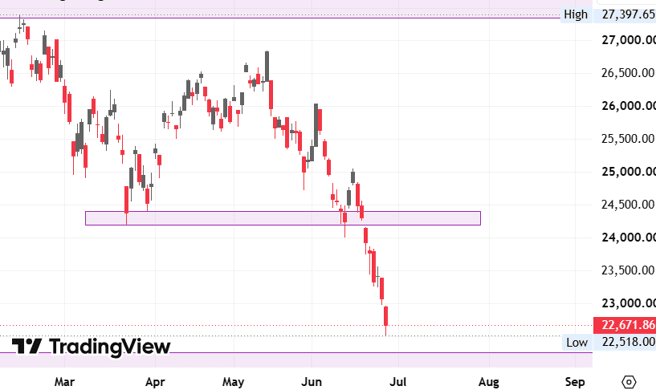

Source: TradingView Source: TradingView | XtalPi (2228.HK)

Last Price: HK$7.74 Support Levels: HK$6.68 (-13.7%)/ HK$6.30 (-18.6%) Resistance Levels: HK$12.37 (+26.1%)/ HK$13.98 (+35.8%) |

Our Technical View

The price has concluded a one-month consolidation phase at its previous support zone, executing a decisive directional pivot via a bullish candle.

The structural bottoming signature is highly synchronised with a shifting momentum profile, as the RSI climbs back above its 50-neutral baseline.

These strongly support a sustained upward expansion.

Source: TradingView Source: TradingView | Horizon Robotics (9660.HK)

Last Price: HK$4.14 Support Levels: HK$3.60 (-13.0%)/ HK$3.32 (-19.8%) Resistance Levels: HK$5.52 (+33.3%)/ HK$6.20 (+49.8%) |

Our Technical View

The price has held its previous horizontal support floor, triggering a localised price rebound.

Underlying momentum is showing signs of deceleration on the downside, as highlighted by the RSI turning upward out of deep oversold territory.

With the sellers temporarily exhausted at this proven structural boundary, the technical setup strongly favours an immediate upward expansion.

Today’s Must-Know News

Wall Street rallies as Iran risk eases. S&P 500 futures were little changed, while S&P 500 gained 1.18% Monday as US-Iran hostilities eased. SpaceX (SPCX +7.15%) gained on Nasdaq 100 inclusion. Alphabet (GOOGL +4.82%) advanced on its first day as a Dow component, replacing Verizon (VZ -5.24%). Semis (SOXX +4.14%) rebounded alongside AI-chip investment headlines from Samsung Electronics (005930 KS -4.13%) and SK Hynix (000660 KS -2.89%), while Honeywell Aerospace (HONA -0.37%) slipped in its Nasdaq debut after spinning off from Honeywell (HON -6.41%). SOXX is our Trading Buy.

Lilly gets faster FDA review. Eli Lilly (LLY +1.81%) is among the firms that are selected for an FDA pilot to speed reviews of new US drug plants, lowering onshoring execution risk. The program also helps reduce tariff exposure as drugmakers expand domestic manufacturing. LLY is our Core Recommendation.

Nike earnings focus on China and tariffs. Nike (NKE +1.79%) reports after-market today (Tuesday), with investors watching China demand, tariff refunds and a 7.923% earnings-related implied move. Investors will also look for turnaround progress and reports Nike may halt partner online sales in China. NKE is our Trading Buy.

There will be no Wealth Daily July 1 (HK public holiday).

Trader’s Corner (Details on Page 7-8) | ||||

Ticker | Name | Rec. | Support Levels | Resistance Levels |

2228.HK | XtalPi | - | HK$6.68/$6.30 | HK$9.76/$10.51 |

9660.HK | Horizon Robotics | - | HK$3.60/$3.32 | HK$5.52/$6.20 |

CR = Core Recommendation; TB = Trading Buy | ||||

Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 0668.HK | Anker | Technology | Jul 2 |

| 2667.HK | Tong Ren Tang Care | Healthcare | Jul 7 |

| 1770.HK | DKE | Technology | Jul 8 |

| 6880.HK | Momenta-W | Technology | Jul 8 |

| 7656.HK | Reconova | Technology | Jul 8 |

| 7687.HK | Eacon | Consumer Disc. | Jul 8 |

| 8090.HK | Baogai | Industrials | Jul 8 |

| 9971.HK | Basic Semi | Technology | Jul 8 |

| 0537.HK | Rigol | Industrials | Jul 9 |

| 1377.HK | Dtech | Industrials | Jul 9 |

| 2475.HK | Luxshare ICT | Technology | Jul 9 |

| 2249.HK | Nexchip | Technology | Jul 10 |

| 2523.HK | EKH | Industrials | Jul 13 |

Americas

Supreme Court protects Fed independence. The US Supreme Court rejected President Trump’s bid to fire Fed Governor Lisa Cook, ruling she was not given required procedural protections and reinforcing that Fed governors can only be removed “for cause.” The court separately expanded presidential power to dismiss leaders of other agencies, raising broader executive-authority risk while leaving Fed independence intact. (Reuters)

Memory makers face DRAM lawsuit. Samsung (005930 KS -4.13%), SK Hynix (000660 KS -2.89%) and Micron (MU +1.14%) were sued in California over claims they restricted commodity DRAM supply during the shift to HBM, lifting prices about 700% over four years. Plaintiffs seek class-action status and treble damages. (Yahoo Finance) MU is our Trading Buy.

Taiwan chip-smuggling probe widens. Super Micro Computer (SMCI -8.1%) plunged Monday after Taiwan authorities raided the firm’s local office as part of an investigation into alleged smuggling of Nvidia (NVDA +1.27%) chips into China using Super Micro servers. Taiwan considering tougher export controls and potential criminal penalties to align more closely with US restrictions. (Bloomberg) NVDA is our Core Recommendation.

Banks expand funding channels for AI debt. AI-related borrowing is approaching 15% of US investment-grade issuance this year as Amazon (AMZN +3.2%) and Alphabet (GOOGL +4.82%) tap global bond markets to fund chips, cloud and data-center spending. Hyperscaler capex is estimated at about USD 725 bn this year, while bankers are using structures such as data-center lease-backed notes to broaden demand and reduce market-saturation risk. (Reuters) AMZN is our Core Recommendation; GOOGL is our Trading Buy.

Rocket Lab takes on SpaceX with Iridium deal. Rocket Lab (RKLB +15.93%) agreed to buy Iridium (IRDM +25.44%) for USD8bn, adding licensed spectrum, a global satellite network and over 2.5 mn subscribers to expand beyond launch services. Iridium holders will receive USD27 cash plus Rocket Lab shares, while Deutsche Bank (DBK GR +0.59%) and Wells Fargo (WFC -0.42%) have committed a USD 3.6 bn bridge loan for the cash portion. (Reuters)

Uber resets Phoenix robotaxi strategy. Uber (UBER -0.92%) and Alphabet’s Waymo (GOOGL +4.82%) ended their limited Phoenix robotaxi pilot of just over a dozen vehicles, with Waymo moving the cars back to its own app fleet while remaining on Uber in Austin and Atlanta. Uber is preparing a new Phoenix autonomous-vehicle partnership as Waymo faces scrutiny after recalling nearly 3,900 US robotaxis over software risk around closed freeway construction zones. (Reuters) GOOGL is our Trading Buy.

Tesla deliveries eyed as FSD update boosts shares. Tesla (TSLA +8.46%) is expected to report its 2Q vehicle deliveries around July 2, with Bloomberg consensus at 396,466 vehicles, compared with Tesla IR consensus estimates of 406,024 (average) and 408,609 (median). Shares jumped Monday, its biggest one-day gain in more than a year, after the firm began early access to version 14 "lite" of its Full Self-Driving software for select older vehicles equipped with Hardware 3. (Reuters)

Applied Materials leads chip rebound. Applied Materials (AMAT +10.82%) shares jumped Monday as analysts lifted price targets. KeyBanc raised its target to USD750 from USD 550 and Cantor Fitzgerald lifted its target to USD 850 from USD 650, though the stock’s move above key trend gauges points to late-stage momentum rather than an early breakout. (Benzinga)

Verizon and BT combine enterprise assets. Verizon (VZ -5.24%) and BT (BT/A LN +0.62%) agreed to merge their international enterprise operations into a 50:50 JV with USD 4 bn of combined annual revenue, with Verizon paying BT USD 625 mn to equalise the transaction. The venture will serve over 3,000 multinational customers across more than 180 countries. (Reuters)

Comcast rallies on NBCUniversal spinoff. Comcast (CMCSA +4.53%) will split into two listed companies via a spinoff of NBCUniversal and Sky, separating its broadband, wireless and business-services arm from its media, studios, Peacock and theme-parks assets. Mike Cavanagh will lead NBCUniversal, former CFO Michael Angelakis will return as Comcast CEO and analysts see NBCUniversal as a potential takeover target. (Reuters)

Digital Realty expands Northern Virginia stake. Digital Realty (DLR -1.25%) will buy larger stakes in three Northern Virginia data centers from Blackstone (BX -0.45%) in a USD 3.5 bn cash-and-stock deal, strengthening its position in the world’s largest data-center market. The deal includes USD 1.2 bn cash and USD 2.3 bn in shares, and is expected to lift Core FFO per share in 2027 and 2028 as development completes and rents begin. (Reuters)

Greater China

China and Hong Kong stocks broaden rally. CSI300 rose 1.21% and HSI gained 1.57% on Monday, led by healthcare, consumer and chip shares as investors rotated beyond AI supply-chain names. The HSTech Index gained 3.23%, with sentiment helped by CXMT’s reported RMB 20 bn-plus memory supply deal with Tencent (0700.HK +2.04%). (Reuters)

CXMT secures Tencent memory deal. China’s ChangXin Memory Technologies signed a multi-year DRAM supply agreement with Tencent (0700.HK +2.04%) worth more than RMB 20 bn, or about USD 2.94 bn, ahead of its planned RMB 29.5 bn Shanghai STAR Market IPO. UBS estimates contract prices rose about 95% qoq in 1Q26 and the global memory upcycle could last until at least late 2027. (Reuters) 0700.HK is our Core Recommendation.

PBOC easing lifts hopes for lower borrowing costs. China's central bank set the rate on its new overnight liquidity tool at 1.25%, below market expectations and the policy rate, after injecting RMB 300 bn via overnight reverse repos to ease half-year funding conditions. The move signalled a more accommodative policy stance and raised expectations for a potential Loan Prime Rate cut as early as next month, supporting lower market borrowing costs. (Reuters)

EU-China trade reset targeted. The EU and China set an October deadline to make progress on trade disputes covering the EU’s widening deficit, Chinese export controls, intellectual property and WTO reforms. Brussels said it remains open for business but needs to defend its industrial base and secure a more level playing field, with both sides also planning a joint platform to monitor trade flows. (Bloomberg)

Baidu chip unit eyes USD 50 bn IPO. Baidu’s (BIDU +7.64%; 9888.HK +5.62%) AI chip unit Kunlunxin is reportedly targeting a Hong Kong IPO at a USD 50 bn valuation, supporting China’s tech self-reliance push. Kunlunxin mainly supplies Baidu, while Tencent (0700.HK +2.04%) is reportedly a customer and ByteDance is considering its chips. (Reuters) 0700.HK is our Core Recommendation.

Nexchip taps Hong Kong market. China’s Nexchip Semiconductor (688249 SZ +7.64%; 2249 HK) is seeking to raise up to HKD 6.98 bn, or about USD 890 mn, through a Hong Kong share sale. The deal adds to China’s semiconductor capital-raising pipeline as domestic chipmakers continue to fund capacity expansion. (Reuters)

Luxshare taps Hong Kong market. Apple supplier Luxshare Precision Industry (002475.SZ -3.97%; 2475.HK), best known for assembling AirPods, is seeking to raise up to USD 3.1 bn through a Hong Kong share sale, according to an exchange filing. The deal would add to Hong Kong’s equity fundraising pipeline. (Reuters)

China expands export curbs, deepens Japan trade tensions. China's Ministry of Commerce added 20 Japanese organisations, including Mitsubishi Heavy Industries (7011 JP +2.35%), Mitsubishi Electric (6503 JP +0.03%) and Kawasaki Heavy Industries (7012 JP +2.56%), to its export-control list, expanding restrictions on dual-use goods. The measures deepen trade tensions with Prime Minister Sanae Takaichi's government and bar overseas entities from supplying listed firms with China-origin dual-use technology. (Reuters)

Asia ex. China

Australia targets Amazon Prime terms. Australia’s competition regulator sued Amazon’s local unit (AMZN +3.2%) over Prime subscription terms it says unfairly allowed the firm to add advertising to Prime Video. The case raises regulatory risk around subscription contract changes and streaming monetisation practices in Australia. (Reuters) AMZN is our Core Recommendation.

Apple supplier leak exposes iPhone 18 Pro details. Apple (AAPL -0.72%) supplier Tata Electronics suffered a dark-web data leak exposing iPhone 18 Pro supplier lists, component mappings and drop-test photos, potentially aiding rivals and counterfeiters. Counterpoint estimates India will produce 26% of global iPhones in 2026. (Reuters)

AirTrunk nears Singapore IPO filing. Blackstone (BX -0.45%) -backed AirTrunk is reportedly close to filing confidentially for a Singapore REIT IPO that could raise about USD 1.5 bn, potentially the city’s biggest listing since Netlink NBN Trust’s USD 1.7 bn deal in 2017. (Bloomberg)

Data centre pipeline strengthens Keppel DC REIT growth. Keppel DC REIT (KDCREIT SP +0.44%) said sponsor Keppel has built a 1.0GW data centre pipeline across Singapore, Japan, South Korea and Australia, with potential acquisitions from 2028 supporting long-term growth. The termination of the SGD 79.2 mn M1 NetCo bond divestment will also preserve a stable SGD 11 mn annual income stream, implying an IRR of 9%. (Reuters)

EMEA and Others

European equities edge higher on tech rebound. STOXX Europe 600 gained 0.04% Monday, supported by technology and energy as AI-linked names recovered from last week’s selloff. UK's FTSE 100, France's CAC 40 and while Germany's DAX retreated by 0.23%, 0.21% and 0.18% respectively. ASML (ASML NA +2.14%) and Prosus (PRX NA +2.43%) shares rose, while banks lagged as sovereign yields rebounded ahead of the ECB forum. (Reuters)

Maersk lifts 2026 outlook. Maersk (MAESKB DC -0.28%) raised its 2026 EBITDA guidance to USD 8-10 bn from USD 4.5-7 bn, citing stronger container-market demand, particularly in Asia. The shipping group also lifted adjusted EBIT guidance to USD 2-4 bn, pointing to a firmer freight backdrop after a volatile cycle for global container carriers. (Reuters)

LVMH and Accor target AI wealth boom. LVMH (MC FP -0.7%) and Accor’s (AC FP -0.08%) Orient Express venture is targeting AI-created ultra-rich customers through luxury experiences, led by its first giant yacht. Accor said high-end experience spending may grow 9-11% this year vs. 1-4% for personal luxury goods, with Orient Express assets estimated at about EUR1bn. (Reuters)

Prosus profit jumps on M&A. Prosus (PRX NA +2.43%) reported FY adjusted EBITDA up 84% to USD 1.3 bn and revenue up 57% to USD 9.7 bn after about USD 8.5 bn of acquisitions. The group plans to use Just Eat Takeaway.com to expand in Europe across food delivery, groceries and fintech, while developing an AI shopping assistant. (Reuters)

TRADERS’ CORNER

| Source: TradingView | XtalPi (2228.HK)

Last Price: HK$7.74 Support Levels: HK$6.68 (-13.7%)/ HK$6.30 (-18.6%) Resistance Levels: HK$12.37 (+26.1%)/ HK$13.98 (+35.8%) |

Our Technical View

The price has concluded a one-month consolidation phase at its previous support zone, executing a decisive directional pivot via a bullish candle.

The structural bottoming signature is highly synchronised with a shifting momentum profile, as the RSI climbs back above its 50-neutral baseline.

These strongly support a sustained upward expansion.

| Source: TradingView | Horizon Robotics (9660.HK)

Last Price: HK$4.14 Support Levels: HK$3.60 (-13.0%)/ HK$3.32 (-19.8%) Resistance Levels: HK$5.52 (+33.3%)/ HK$6.20 (+49.8%) |

Our Technical View

The price has held its previous horizontal support floor, triggering a localised price rebound.

Underlying momentum is showing signs of deceleration on the downside, as highlighted by the RSI turning upward out of deep oversold territory.

With the sellers temporarily exhausted at this proven structural boundary, the technical setup strongly favours an immediate upward expansion.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.