Overnight Markets

Today’s Must-Know News

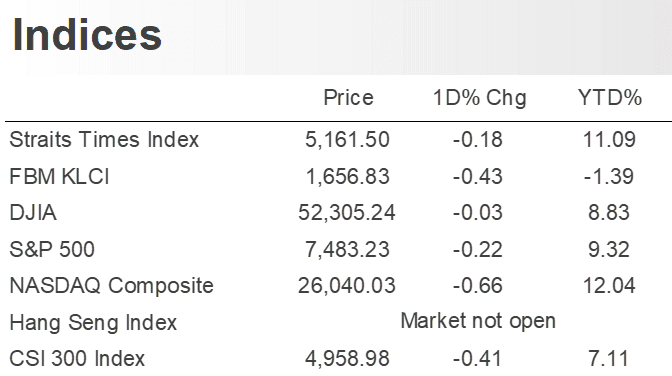

AI compute monetisation. S&P 500 fell 0.22% on Wednesday ahead of Friday’s Independence Day holiday, with gains in Meta (META +8.81%) limiting the decline after it announced plans for a cloud-infrastructure business to sell access to excess AI computing power (AMZN +1.41%, MSFT +3.02%, GOOGL +1.07%). The news weighed most directly on neocloud providers CoreWeave (CRWV -13.92%) & Nebius (NBIS -17.01%) on concerns Meta could add GPU-compute supply and intensify AI workload competition, while chipmakers (SOXX -6.41%, TSM -6.98%, NVDA -1.25%, AMD -6.89%) also fell amid broader worries over AI-capacity overbuild. META, AMZN, MSFT, TSM & NVDA are our Core Recommendations; GOOGL & SOXX are our Trading Buys.

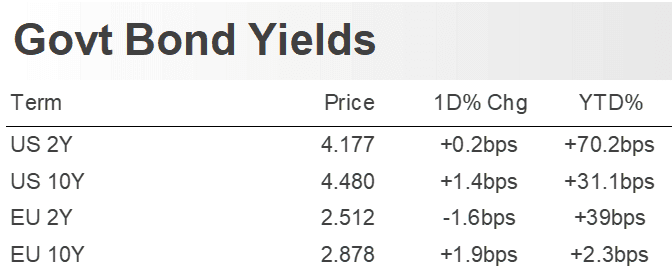

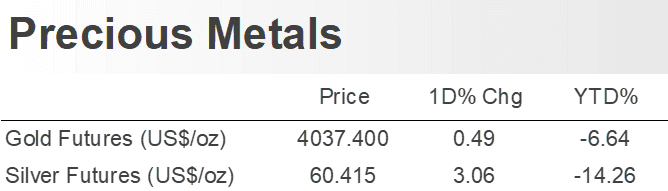

Warsh Goldilocks. Warsh’s softer inflation comments strengthened the lower-real-rate narrative. Gold (XAU +0.56%) gained Wednesday. The 10-year Treasury yields reversed earlier losses ahead of the June nonfarm payrolls report due Thursday.

Tariff-aided beat. Nike (NKE +4.9%) rose after 4QFY26 revenue of USD10.97bn and adjusted EPS of USD 0.20 beat consensus, even as Greater China sales fell 12% and management said the turnaround remains uneven. NKE is our Trading Buy.

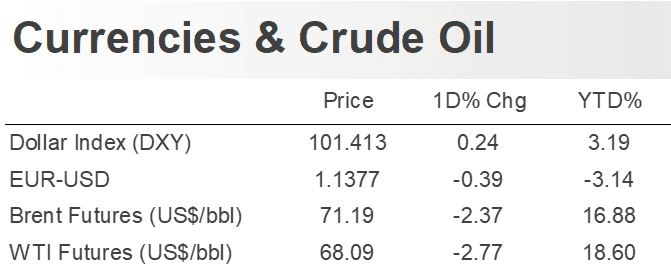

Hormuz risk premium fades. Commercial shipping through the Strait of Hormuz rose in recent weeks, with US military support helping lift oil flows above 10 mn bpd, while President Trump said indirect talks with Iran had made progress. Front month WTI crude futures fell for a third day early Thursday to near USD 68/bbl as easing supply-risk concerns reduced the geopolitical premium in oil, weighing on energy stocks (XLE -0.56%). (Bloomberg) XLE is our Core Recommendation.

Microsoft layoffs may widen. Microsoft (MSFT +3.02%) is planning to cut less than 2.5% of its workforce as early as next week, with thousands of roles potentially affected across sales, consulting and Xbox. (Reuters) MSFT is our Core Recommendation.

Auto memory lock-up. Micron (MU -10.57%) signed a long-term supply agreement with General Motors (GM -2.02%) covering LPDRAM, NOR and UFS NAND for future vehicle platforms, supported by Micron’s USD 2 bn Manassas, Virginia fab expansion. (Reuters) MU is our Trading Buy.

Trader’s Corner (Details on Page 6-7) | ||||

Ticker | Name | Rec. | Support Levels | Resistance Levels |

9903.HK | Shanghai Iluvatar CoreX | - | HK$656.00/$614.00 | HK$887.50/$1050.00 |

0669.HK | Techtronic Industries | - | HK$125.60/$121.30 | HK$147.00/$156.80 |

CR = Core Recommendation; TB = Trading Buy | ||||

Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 2667.HK | Tong Ren Tang Care | Healthcare | Jul 7 |

| 1770.HK | DKE | Technology | Jul 8 |

| 6880.HK | Momenta-W | Technology | Jul 8 |

| 7656.HK | Reconova | Technology | Jul 8 |

| 7687.HK | Eacon | Consumer Disc. | Jul 8 |

| 8090.HK | Baogai | Industrials | Jul 8 |

| 9971.HK | Basic Semi | Technology | Jul 8 |

| 0537.HK | Rigol | Industrials | Jul 9 |

| 1377.HK | Dtech | Industrials | Jul 9 |

| 2475.HK | Luxshare ICT | Technology | Jul 9 |

| 2249.HK | Nexchip | Technology | Jul 10 |

| 6745.HK | Befar Group | Materials | Jul 10 |

| 2523.HK | EKH | Industrials | Jul 13 |

Americas

Crypto drives Trump's income. President Trump reported more than USD 1.4 bn in income from his family's crypto ventures last year, with digital assets accounting for most of his earnings, according to his latest financial disclosures. The businesses have benefited from policies supporting the crypto sector. (Reuters)

Musk device denial. Elon Musk denied a Wall Street Journal report that SpaceX had shown investors and stakeholders a prototype AI-focused handset ahead of its IPO. The denial reduces near-term speculation about a SpaceX consumer-device push, though investor attention remains high around potential AI and connectivity adjacencies. (Reuters)

Anthropic export controls lifted. Anthropic said the US Commerce Department lifted export controls on its most advanced Fable and Mythos AI models, less than three weeks after ordering access suspended over national security risks. The firm said new safeguards are in place and it is working with partners and the US government on standards to assess and fix jailbreaks, though Fable 5 users may see more benign requests blocked. (Reuters)

Software relief rally. Software stocks rose after Guggenheim said AI will not be the sector’s “death knell” and upgraded Salesforce (CRM +4.19%), ServiceNow (NOW +5.57%) and Check Point Software (CHKP +2.18%) to Buy from Neutral. The firm said valuations already imply a long-term AI-driven decline that is too pessimistic, helping lift the Software ETF (IGV +3.02%). (Bloomberg)

Apple refresh cycle. Apple (AAPL +1.73%) is reportedly preparing a new iPad Pro, redesigned MacBook Pro and other products for the iPhone’s 20th anniversary next year. The company is also said to be negotiating with Pentagon-blacklisted Chinese memory suppliers ChangXin Memory Technologies and Yangtze Memory Technologies to ease a global memory shortage that has forced price increases, raising potential US policy and supply-chain scrutiny. (Bloomberg)

EV crown shift. BYD (1211.HK) delivered 557,090 battery-electric vehicles in 2Q, likely enough to overtake Tesla (TSLA +1.12%) as the world’s top BEV seller as overseas shipments expand. Tesla reports next week, but Bloomberg-compiled estimates suggest its 2Q deliveries may fall short of BYD’s total. Meanwhile, Tesla June registrations rose in most major European EV markets, more than doubling in France and rising 56% in Sweden, 43% in Portugal and Italy, 39% in Denmark and 5.6% in Spain. Norway was the key outlier, with registrations down 43%. (Bloomberg)

North America trade limbo. The US decided not to renew USMCA with Canada and Mexico, shifting the pact into annual reviews while keeping it in force until 2036. The move adds tariff and rules-of-origin uncertainty for North American supply chains, especially autos and industrial goods, and could weigh on investment planning across roughly USD 1.6 tn of regional trade. (Bloomberg)

Bloom AI power funding expands. Bloom Energy (BE -4.36%) and Brookfield (BAM +1.23%) expanded their AI infrastructure power partnership, increasing the funding framework fivefold to USD 25 bn to accelerate global deployment of Bloom’s fuel cells. (Reuters)

Lime IPO lift. Uber-backed Lime (LIME +4.0%) rose in its Nasdaq debut Wednesday, valuing the e-scooter and bike operator at about USD 1.7 bn. The listing points to firmer investor appetite for mobility-platform IPOs, helped by Lime’s urban micromobility model and Uber’s strategic backing. (Reuters)

Greater China

China factory data lifts sentiment. China stocks rose Wednesday as June manufacturing activity expanded for a seventh month and President Xi Jinping reiterated support for high-quality development, though the CSI 300 fell 0.41% on concerns over uneven growth. Tech shares outperformed traditional sectors, while Goldman Sachs said local investors remain more cautious on China’s near-term momentum and a bifurcated growth mix. (Reuters) HK market was closed for holiday.

US legal overhang. Alibaba (BABA +2.09%; 9988.HK) and its US-based payment processor agreed to pay USD 600 mn to resolve US Justice Department allegations that they failed to prevent illegal drug sale. (Reuters) 9988.HK is our Core Recommendation.

EU targets low-value parcels. The EU imposed a EUR 3 fee on low-value e-commerce imports from China, targeting duty-free parcels used by platforms such as Shein, PDD's (PDD +8.18%) Temu and Alibaba’s AliExpress (BABA +2.09%; 9988.HK). The measure raises cross-border fulfilment costs and adds a tariff-related headwind for ultra-low-cost online retail models in Europe. (Reuters) 9988.HK is our Core Recommendation.

Xiaomi frames cars as AI partners. Xiaomi (1810.HK) said its move into autos is aimed at building an AI-enabled “human-car-home” ecosystem rather than adding another screen, with chief designer Li Tianyuan saying cars can become partners that understand drivers. The firm said its YU7 SUV drew 200,000 confirmed orders within three minutes of launch in China, underscoring early traction for its auto strategy. (Reuters) 1810.HK is our Core Recommendation.

Syngenta names new CEO. Syngenta appointed Hengde Qin as CEO, effective Aug. 1, succeeding Jeff Rowe, as the Chinese-owned seed and pesticide giant prepares for a Hong Kong IPO. The listing could raise up to USD 10 bn and is expected around end-2026 or early 2027. (Reuters)

Taiwan probes chip smuggling. Taiwan detained two Super Micro Computer (SMCI -5.73%) employees as part of a probe into alleged shipments of Nvidia (NVDA -1.25%) chips to China. Prosecutors are investigating four employees over alleged document falsification and breach of trust, following raids on the company's local offices. (Reuters) NVDA is our Core Recommendation.

ByteDance expands AI infrastructure. ByteDance is building its largest data center outside China in Brazil's Ceará state, with an initial computing capacity of 200MW that could eventually expand to 1GW. The project supports the firm's global AI expansion, leveraging Brazil's renewable energy and strategic telecom location. (Reuters)

Asia ex. China

Memory price-fixing probe. Samsung (005930 KS -3.54%), SK Hynix (000660 KS -3.37%) and Micron (MU -10.57%) face a California class-action lawsuit alleging collusion and price-fixing during a global memory-chip shortage. The complaint, filed by 17 individual and small-business plaintiffs, adds legal risk as tight DRAM/NAND supply continues to lift prices for manufacturers and consumers. (Bloomberg) MU is our Trading Buy.

AI stake backs margin loan. SoftBank (9984 JP +0.62%) has reopened talks for a USD 10 bn margin loan backed by its OpenAI stake, offering a corporate guarantee to address lender concerns over valuing and liquidating private-company collateral. (Reuters)

Cargo growth stays strong. SATS (SATS SP -0.88%) expects nearly 10% YoY cargo volume growth in 1QFY27, driven by industry recovery and new contract wins, while ground handling remains resilient despite softer food volumes. We raise FY27-29 earnings by 4-5%, maintain BUY, and increase our target price to SGD 5. (UOB Kay Hian Institutional Research)

EMEA and Others

Europe markets turn mixed. European shares were mixed after a strong 2Q rally, with the STOXX 600 down 0.38% as tech fell on valuation concerns and higher-for-longer US rate risks, while London’s FTSE 100 and France’s CAC 40 slipped 0.18% and 0.79% respectively. However, Germany's DAX edged up 0.18%. (Reuters)

Saab Ukraine fighter deal lifts defence focus. Saab (SAABB SS +3.32%) signed a SEK 24.6 bn, or USD 2.54 bn, contract to deliver 16 Gripen E fighter jets to Ukraine, with the agreement also including technical support. Ukrainian President Volodymyr Zelenskiy said the deal was reached with Swedish Prime Minister Ulf Kristersson, reinforcing Ukraine’s long-term air-defence procurement push. (Reuters)

Volkswagen autonomy reset deepens. Volkswagen’s (VOW GR +1.04%) software unit Cariad and Bosch ended their autonomous-driving tie-up, adding another setback to the automaker’s push to simplify and accelerate its software roadmap. The move underscores continued execution challenges as legacy automakers shift toward in-house software and advanced driver-assistance systems. (Reuters)

TRADERS’ CORNER

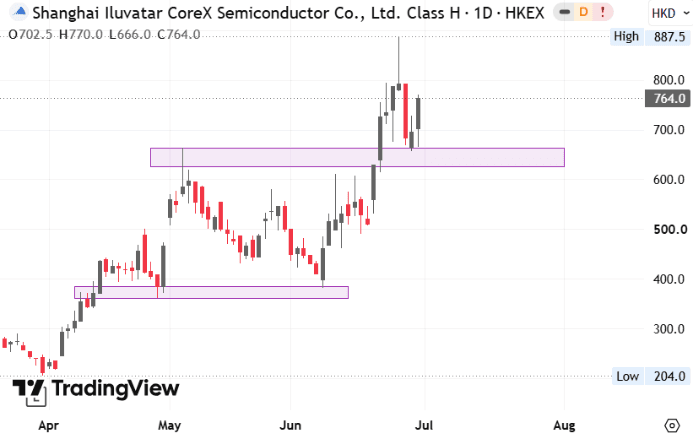

Source: TradingView Source: TradingView | Shanghai Iluvatar CoreX (9903.HK)

Last Price: HK$764.00 Support Levels: HK$656.00 (-14.1%)/ HK$614.00 (-19.6%) Resistance Levels: HK$887.50 (+16.2%)/ HK$1050.00 (+37.4%) |

Our Technical View

Following a clean breakout, the price stayed above the resistance-turned-support zone, keeping its primary upward structure intact.

The MACD remains exceptionally strong and entrenched in a bullish zone.

With the breakout successfully insulated against structural failure and momentum indicators displaying zero signs of exhaustion, the technical setup firmly favours a near-term continuous move higher.

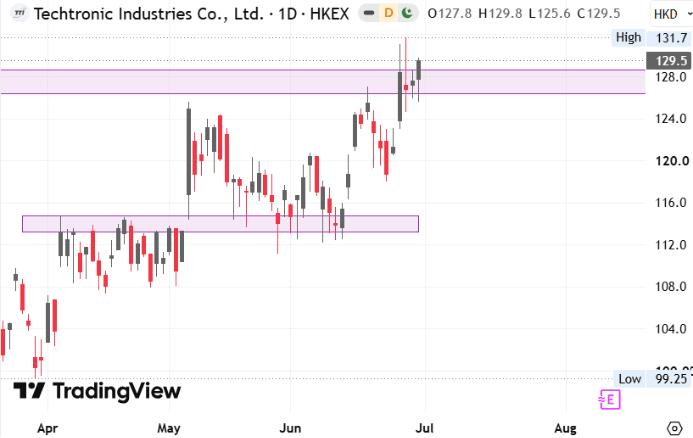

Source: TradingView Source: TradingView | Techtronic Industries (0669.HK)

Last Price: HK$129.50 Support Levels: HK$125.60 (-3.0%)/ HK$121.30 (-6.5%) Resistance Levels: HK$147.00(+13.5%)/ HK$156.80 (+20.9%) |

Our Technical View

- The price has successfully confirmed a breakout-and-retest sequence, holding steady above the resistance-turned-support floor.

- This shows that buyers are stepping in to defend this new, higher price tier.

- Underlying market strength is expanding in real-time, as the MACD remains bullish and is actively curling upward.

- As long as the price stays above this critical support zone, the technical setup strongly favours a continuous move higher.

Today’s Must-Know News

AI compute monetisation. S&P 500 fell 0.22% on Wednesday ahead of Friday’s Independence Day holiday, with gains in Meta (META +8.81%) limiting the decline after it announced plans for a cloud-infrastructure business to sell access to excess AI computing power (AMZN +1.41%, MSFT +3.02%, GOOGL +1.07%). The news weighed most directly on neocloud providers CoreWeave (CRWV -13.92%) & Nebius (NBIS -17.01%) on concerns Meta could add GPU-compute supply and intensify AI workload competition, while chipmakers (SOXX -6.41%, TSM -6.98%, NVDA -1.25%, AMD -6.89%) also fell amid broader worries over AI-capacity overbuild. META, AMZN, MSFT, TSM & NVDA are our Core Recommendations; GOOGL & SOXX are our Trading Buys.

Warsh Goldilocks. Warsh’s softer inflation comments strengthened the lower-real-rate narrative. Gold (XAU +0.56%) gained Wednesday. The 10-year Treasury yields reversed earlier losses ahead of the June nonfarm payrolls report due Thursday.

Tariff-aided beat. Nike (NKE +4.9%) rose after 4QFY26 revenue of USD10.97bn and adjusted EPS of USD 0.20 beat consensus, even as Greater China sales fell 12% and management said the turnaround remains uneven. NKE is our Trading Buy.

Hormuz risk premium fades. Commercial shipping through the Strait of Hormuz rose in recent weeks, with US military support helping lift oil flows above 10 mn bpd, while President Trump said indirect talks with Iran had made progress. Front month WTI crude futures fell for a third day early Thursday to near USD 68/bbl as easing supply-risk concerns reduced the geopolitical premium in oil, weighing on energy stocks (XLE -0.56%). (Bloomberg) XLE is our Core Recommendation.

Microsoft layoffs may widen. Microsoft (MSFT +3.02%) is planning to cut less than 2.5% of its workforce as early as next week, with thousands of roles potentially affected across sales, consulting and Xbox. (Reuters) MSFT is our Core Recommendation.

Auto memory lock-up. Micron (MU -10.57%) signed a long-term supply agreement with General Motors (GM -2.02%) covering LPDRAM, NOR and UFS NAND for future vehicle platforms, supported by Micron’s USD 2 bn Manassas, Virginia fab expansion. (Reuters) MU is our Trading Buy.

Trader’s Corner (Details on Page 6-7) | ||||

Ticker | Name | Rec. | Support Levels | Resistance Levels |

9903.HK | Shanghai Iluvatar CoreX | - | HK$656.00/$614.00 | HK$887.50/$1050.00 |

0669.HK | Techtronic Industries | - | HK$125.60/$121.30 | HK$147.00/$156.80 |

CR = Core Recommendation; TB = Trading Buy | ||||

Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 2667.HK | Tong Ren Tang Care | Healthcare | Jul 7 |

| 1770.HK | DKE | Technology | Jul 8 |

| 6880.HK | Momenta-W | Technology | Jul 8 |

| 7656.HK | Reconova | Technology | Jul 8 |

| 7687.HK | Eacon | Consumer Disc. | Jul 8 |

| 8090.HK | Baogai | Industrials | Jul 8 |

| 9971.HK | Basic Semi | Technology | Jul 8 |

| 0537.HK | Rigol | Industrials | Jul 9 |

| 1377.HK | Dtech | Industrials | Jul 9 |

| 2475.HK | Luxshare ICT | Technology | Jul 9 |

| 2249.HK | Nexchip | Technology | Jul 10 |

| 6745.HK | Befar Group | Materials | Jul 10 |

| 2523.HK | EKH | Industrials | Jul 13 |

Americas

Crypto drives Trump's income. President Trump reported more than USD 1.4 bn in income from his family's crypto ventures last year, with digital assets accounting for most of his earnings, according to his latest financial disclosures. The businesses have benefited from policies supporting the crypto sector. (Reuters)

Musk device denial. Elon Musk denied a Wall Street Journal report that SpaceX had shown investors and stakeholders a prototype AI-focused handset ahead of its IPO. The denial reduces near-term speculation about a SpaceX consumer-device push, though investor attention remains high around potential AI and connectivity adjacencies. (Reuters)

Anthropic export controls lifted. Anthropic said the US Commerce Department lifted export controls on its most advanced Fable and Mythos AI models, less than three weeks after ordering access suspended over national security risks. The firm said new safeguards are in place and it is working with partners and the US government on standards to assess and fix jailbreaks, though Fable 5 users may see more benign requests blocked. (Reuters)

Software relief rally. Software stocks rose after Guggenheim said AI will not be the sector’s “death knell” and upgraded Salesforce (CRM +4.19%), ServiceNow (NOW +5.57%) and Check Point Software (CHKP +2.18%) to Buy from Neutral. The firm said valuations already imply a long-term AI-driven decline that is too pessimistic, helping lift the Software ETF (IGV +3.02%). (Bloomberg)

Apple refresh cycle. Apple (AAPL +1.73%) is reportedly preparing a new iPad Pro, redesigned MacBook Pro and other products for the iPhone’s 20th anniversary next year. The company is also said to be negotiating with Pentagon-blacklisted Chinese memory suppliers ChangXin Memory Technologies and Yangtze Memory Technologies to ease a global memory shortage that has forced price increases, raising potential US policy and supply-chain scrutiny. (Bloomberg)

EV crown shift. BYD (1211.HK) delivered 557,090 battery-electric vehicles in 2Q, likely enough to overtake Tesla (TSLA +1.12%) as the world’s top BEV seller as overseas shipments expand. Tesla reports next week, but Bloomberg-compiled estimates suggest its 2Q deliveries may fall short of BYD’s total. Meanwhile, Tesla June registrations rose in most major European EV markets, more than doubling in France and rising 56% in Sweden, 43% in Portugal and Italy, 39% in Denmark and 5.6% in Spain. Norway was the key outlier, with registrations down 43%. (Bloomberg)

North America trade limbo. The US decided not to renew USMCA with Canada and Mexico, shifting the pact into annual reviews while keeping it in force until 2036. The move adds tariff and rules-of-origin uncertainty for North American supply chains, especially autos and industrial goods, and could weigh on investment planning across roughly USD 1.6 tn of regional trade. (Bloomberg)

Bloom AI power funding expands. Bloom Energy (BE -4.36%) and Brookfield (BAM +1.23%) expanded their AI infrastructure power partnership, increasing the funding framework fivefold to USD 25 bn to accelerate global deployment of Bloom’s fuel cells. (Reuters)

Lime IPO lift. Uber-backed Lime (LIME +4.0%) rose in its Nasdaq debut Wednesday, valuing the e-scooter and bike operator at about USD 1.7 bn. The listing points to firmer investor appetite for mobility-platform IPOs, helped by Lime’s urban micromobility model and Uber’s strategic backing. (Reuters)

Greater China

China factory data lifts sentiment. China stocks rose Wednesday as June manufacturing activity expanded for a seventh month and President Xi Jinping reiterated support for high-quality development, though the CSI 300 fell 0.41% on concerns over uneven growth. Tech shares outperformed traditional sectors, while Goldman Sachs said local investors remain more cautious on China’s near-term momentum and a bifurcated growth mix. (Reuters) HK market was closed for holiday.

US legal overhang. Alibaba (BABA +2.09%; 9988.HK) and its US-based payment processor agreed to pay USD 600 mn to resolve US Justice Department allegations that they failed to prevent illegal drug sale. (Reuters) 9988.HK is our Core Recommendation.

EU targets low-value parcels. The EU imposed a EUR 3 fee on low-value e-commerce imports from China, targeting duty-free parcels used by platforms such as Shein, PDD's (PDD +8.18%) Temu and Alibaba’s AliExpress (BABA +2.09%; 9988.HK). The measure raises cross-border fulfilment costs and adds a tariff-related headwind for ultra-low-cost online retail models in Europe. (Reuters) 9988.HK is our Core Recommendation.

Xiaomi frames cars as AI partners. Xiaomi (1810.HK) said its move into autos is aimed at building an AI-enabled “human-car-home” ecosystem rather than adding another screen, with chief designer Li Tianyuan saying cars can become partners that understand drivers. The firm said its YU7 SUV drew 200,000 confirmed orders within three minutes of launch in China, underscoring early traction for its auto strategy. (Reuters) 1810.HK is our Core Recommendation.

Syngenta names new CEO. Syngenta appointed Hengde Qin as CEO, effective Aug. 1, succeeding Jeff Rowe, as the Chinese-owned seed and pesticide giant prepares for a Hong Kong IPO. The listing could raise up to USD 10 bn and is expected around end-2026 or early 2027. (Reuters)

Taiwan probes chip smuggling. Taiwan detained two Super Micro Computer (SMCI -5.73%) employees as part of a probe into alleged shipments of Nvidia (NVDA -1.25%) chips to China. Prosecutors are investigating four employees over alleged document falsification and breach of trust, following raids on the company's local offices. (Reuters) NVDA is our Core Recommendation.

ByteDance expands AI infrastructure. ByteDance is building its largest data center outside China in Brazil's Ceará state, with an initial computing capacity of 200MW that could eventually expand to 1GW. The project supports the firm's global AI expansion, leveraging Brazil's renewable energy and strategic telecom location. (Reuters)

Asia ex. China

Memory price-fixing probe. Samsung (005930 KS -3.54%), SK Hynix (000660 KS -3.37%) and Micron (MU -10.57%) face a California class-action lawsuit alleging collusion and price-fixing during a global memory-chip shortage. The complaint, filed by 17 individual and small-business plaintiffs, adds legal risk as tight DRAM/NAND supply continues to lift prices for manufacturers and consumers. (Bloomberg) MU is our Trading Buy.

AI stake backs margin loan. SoftBank (9984 JP +0.62%) has reopened talks for a USD 10 bn margin loan backed by its OpenAI stake, offering a corporate guarantee to address lender concerns over valuing and liquidating private-company collateral. (Reuters)

Cargo growth stays strong. SATS (SATS SP -0.88%) expects nearly 10% YoY cargo volume growth in 1QFY27, driven by industry recovery and new contract wins, while ground handling remains resilient despite softer food volumes. We raise FY27-29 earnings by 4-5%, maintain BUY, and increase our target price to SGD 5. (UOB Kay Hian Institutional Research)

EMEA and Others

Europe markets turn mixed. European shares were mixed after a strong 2Q rally, with the STOXX 600 down 0.38% as tech fell on valuation concerns and higher-for-longer US rate risks, while London’s FTSE 100 and France’s CAC 40 slipped 0.18% and 0.79% respectively. However, Germany's DAX edged up 0.18%. (Reuters)

Saab Ukraine fighter deal lifts defence focus. Saab (SAABB SS +3.32%) signed a SEK 24.6 bn, or USD 2.54 bn, contract to deliver 16 Gripen E fighter jets to Ukraine, with the agreement also including technical support. Ukrainian President Volodymyr Zelenskiy said the deal was reached with Swedish Prime Minister Ulf Kristersson, reinforcing Ukraine’s long-term air-defence procurement push. (Reuters)

Volkswagen autonomy reset deepens. Volkswagen’s (VOW GR +1.04%) software unit Cariad and Bosch ended their autonomous-driving tie-up, adding another setback to the automaker’s push to simplify and accelerate its software roadmap. The move underscores continued execution challenges as legacy automakers shift toward in-house software and advanced driver-assistance systems. (Reuters)

TRADERS’ CORNER

| Source: TradingView | Shanghai Iluvatar CoreX (9903.HK)

Last Price: HK$764.00 Support Levels: HK$656.00 (-14.1%)/ HK$614.00 (-19.6%) Resistance Levels: HK$887.50 (+16.2%)/ HK$1050.00 (+37.4%) |

Our Technical View

Following a clean breakout, the price stayed above the resistance-turned-support zone, keeping its primary upward structure intact.

The MACD remains exceptionally strong and entrenched in a bullish zone.

With the breakout successfully insulated against structural failure and momentum indicators displaying zero signs of exhaustion, the technical setup firmly favours a near-term continuous move higher.

| Source: TradingView | Techtronic Industries (0669.HK)

Last Price: HK$129.50 Support Levels: HK$125.60 (-3.0%)/ HK$121.30 (-6.5%) Resistance Levels: HK$147.00(+13.5%)/ HK$156.80 (+20.9%) |

Our Technical View

- The price has successfully confirmed a breakout-and-retest sequence, holding steady above the resistance-turned-support floor.

- This shows that buyers are stepping in to defend this new, higher price tier.

- Underlying market strength is expanding in real-time, as the MACD remains bullish and is actively curling upward.

- As long as the price stays above this critical support zone, the technical setup strongly favours a continuous move higher.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.