Overnight Markets

Today’s Must-Know News

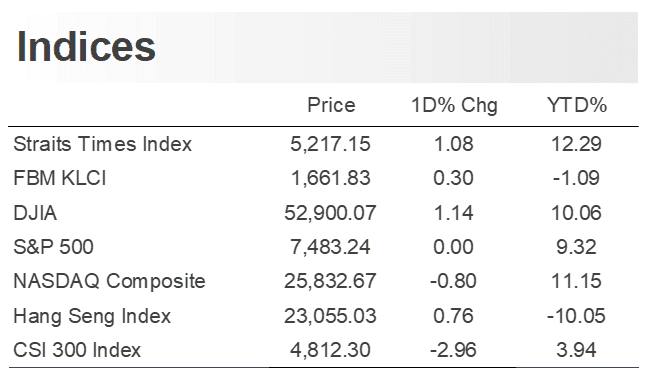

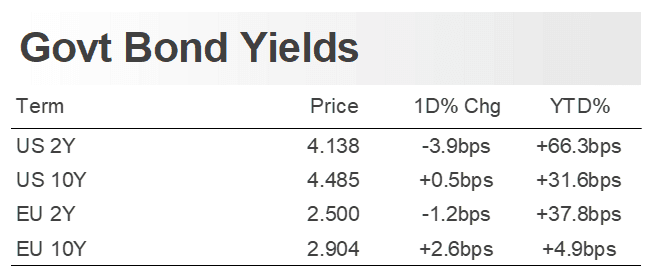

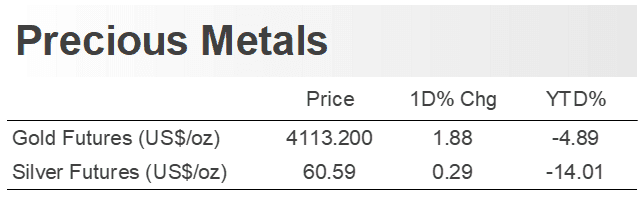

Defensive bid offsets AI-chip unwind. S&P 500 was flat Thursday as the broader market rotated into healthcare (XLV +2.63%), staples (XLP +2.03%) & utilities (XLU +2.21%). Nasdaq fell 0.8% with Semis (SOXX -5.57%) down for a second day as Anthropic held talks with Samsung (005930 KS -9.06%) as a potential manufacturing partner for a custom AI chip. Meta (META -4.9%) also weighed after Zuckerberg told employees AI agent development had not accelerated as expected over the past four months. DJIA gained 1.14% to a record high; top gainers include Apple (AAPL +4.84%), McDonald’s (MCD +4.16%) & Disney (DIS +3.96%). SpaceX (SPCX +2.83%) will join the Nasdaq 100 before market open on July 7. Weak June payrolls of 57,000 and downward revisions lifted short-dated Treasuries and gold (XAU +2.28%), cutting July Fed 25-bps hike odds to 17.6% from 32.1% last week. META & XLP are our Core Recommendations; SOXX & XLV are our trading Buys.

OpenAI floats state stake. OpenAI has reportedly held preliminary talks on giving the US government a 5% stake, with CEO Sam Altman proposing a broader framework that could apply to other major US AI developers.

Burry targets memory cycle. Michael Burry shorted Micron (MU -5.49%), citing the memory maker’s cyclical earnings risk and tendency to overshoot in cycles, one day after disclosing shorts in Caterpillar (CAT -2.81%); Tesla (TSLA -7.49%) & Semis (SOXX -5.57%). MU is our Trading Buy.

Trader’s Corner (Details on Page 6-7) | ||||

Ticker | Name | Rec. | Support Levels | Resistance Levels |

3692.HK | Hansoh Pharmaceutical Group | - | HK$29.16/$28.14 | HK$34.56/$38.40 |

3808.HK | Sinotruk HK | - | HK$37.42/$35.54 | HK$45.24/HK$48.40 |

CR = Core Recommendation; TB = Trading Buy | ||||

Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 2667.HK | Tong Ren Tang Care | Healthcare | Jul 7 |

| 1770.HK | DKE | Technology | Jul 8 |

| 6880.HK | Momenta-W | Technology | Jul 8 |

| 7656.HK | Reconova | Technology | Jul 8 |

| 7687.HK | Eacon | Consumer Disc. | Jul 8 |

| 8090.HK | Baogai | Industrials | Jul 8 |

| 9971.HK | Basic Semi | Technology | Jul 8 |

| 0537.HK | Rigol | Industrials | Jul 9 |

| 1377.HK | Dtech | Industrials | Jul 9 |

| 2475.HK | Luxshare ICT | Technology | Jul 9 |

| 2249.HK | Nexchip | Technology | Jul 10 |

| 6745.HK | Befar Group | Materials | Jul 10 |

| 2523.HK | EKH | Industrials | Jul 13 |

Americas

Anthropic stake talks denied. Anthropic has not discussed the US government taking a stake in the firm, after reports that OpenAI had discussed a potential 5% government stake. The update keeps Anthropic separate from the OpenAI proposal for now, but Washington’s scrutiny of advanced AI models, export controls and public participation in AI-sector profits remains a rising policy overhang. (Reuters)

Tesla China output rebounds. Tesla’s (TSLA -7.49%) China-made EV sales rose 24.4% yoy in June to 89,091 units, marking an eighth straight monthly increase, while 2Q China sales and exports from Shanghai rose 32.8% yoy. The rebound in Europe and resilient China demand helped offset North America softness, though BYD (1211.HK +8.07%) sold 557,090 BEVs globally in 2Q and remains a key volume threat. Separately, Tesla (TSLA -7.49%) launched the six-seater long-wheelbase Model Y L in the US, with the launch version starting at USD 61,990, after the same format helped support sales in China. (Reuters)

Nvidia widens AI monetisation. Nvidia (NVDA -1.39%) is offering token credits to AI developers in exchange for a share of future sales, aiming to turn access to its AI hardware into a recurring usage-linked earnings stream. The DSX AI factory model targets startups and researchers that lack capital for large-scale compute, potentially expanding Nvidia’s ecosystem beyond upfront GPU sales. (Bloomberg) NVDA is our Core Recommendation.

Microsoft turns AI into services. Microsoft (MSFT +1.62%) is forming a 6,000-person AI deployment organization to help enterprise customers with technical, strategic and industry-specific implementation work. The push responds to customer concerns over AI costs and mirrors a broader vendor shift toward embedded engineering support as companies seek faster ROI from model deployment. (Bloomberg) MSFT is our Core Recommendation.

Model-agnostic AI services expand. Microsoft (MSFT +1.62%) will launch Microsoft Frontier Company with USD 2.5 bn in funding to help clients such as Unilever (xx LN) and Novo Nordisk (NVO +3.4%; NOVOB DC +2.47%) choose and integrate Microsoft, third-party and open-source AI models using internal data. (Reuters) MSFT is our Core Recommendation.

Satellite internet launch edges closer, but rocket bottlenecks remain. Amazon (AMZN +0.4%) said its Leo broadband network has reached 394 satellites and is ready for initial internet service later this year, though it remains well behind SpaceX’s roughly 10,000-satellite Starlink fleet. Execution risk remains tied to launch capacity, with Blue Origin’s New Glenn and ULA’s Vulcan grounded despite Amazon booking roughly 100 launches worth at least USD 82 bn to build out more than 3,200 satellites. (Reuters) AMZN is our Core Recommendation.

Regulatory drag, cyber win. Alphabet’s Google (GOOGL -0.36%) lost its EU Android antitrust appeal, confirming a EUR 4.1 bn fine tied to agreements that favoured Search, Chrome and Play Store, raising follow-on litigation risk and adding DMA scrutiny despite the fine being less than 3% of Alphabet’s annual profit. Separately, Google said coordinated action with the FBI, Lumen (LUMN -10.07%) and other partners weakened the NetNut/Popa residential proxy network by millions of devices, while parent Alarum Technologies (ALAR IT -1.23%) said it will cooperate with law enforcement. (Reuters) GOOGL is our Trading Buy.

7-Eleven seeks to block Air Max launch. 7-Eleven sued Nike (NKE +2.39%) in Texas, alleging the planned Air Max 95 launch uses a confusingly similar orange, green and red stripe design tied to 7-Eleven’s brand and its July 11 “7-Eleven Day” promotion. The retailer is seeking to block sales, recall distributed products and recover damages and profits. (Reuters) NKE is our Trading Buy.

Redemption pressure easing but still above cap. Blue Owl Capital (OWL +4.63%%) kept a 5% quarterly withdrawal cap on two private-credit funds after investors sought USD 4.7 bn of redemptions in 2Q, down from USD 5.4 bn in 1Q. Requests remain elevated at 38.1% for OTIC and 18.8% for OCIC, but the decline supported hopes that redemption stress in non-traded BDCs may have peaked. (Reuters)

Greater China

China chip selloff drives rotation. Chinese stocks fell to a three-week low Thursday as the CSI 300 dropped 2.96%, with semiconductors leading the fall. HSI gained 0.76% as Hong Kong shares rebounded on internet strength and China Resources New Energy tripled on its listing debut. (Reuters)

US drug-sales probe ends with USD 600 mn payment. Alibaba (BABA -1.89%; 9988.HK +1.78%) and its US-based payment processor agreed to pay USD 600 mn under non-prosecution agreements over allegations they failed to prevent illegal drug, chemical and pill-press sales into the US from 2016 to 2024. The Justice Department said the transactions involved about 80k product sales and more than USD 200 mn in merchandise value, while Alibaba said the settlement reflected cooperation and improved compliance. (Reuters) 9988.HK is our Core Recommendation.

Europe comeback leans on multi-energy lineup. Great Wall Motor (601633 CH -0.4%; 2333.HK -4.88%) targets 3% to 5% European market share by 2030, supported by at least 10 new models over two years and a pivot from EV-only to petrol, hybrid and electric offerings. The firm is also assessing European manufacturing investment, while the Ora 5 compact SUV will start at EUR 26,950 and is expected to be its main volume product. (Reuters)

Kling AI secures major funding. Kling AI raised an initial USD 2 bn in venture funding to expand its AI video business, with the round potentially reaching USD 3 bn, reducing parent Kuaishou (1024 HK +2.5%) stake to about 68%. The AI video startup, valued at about USD 15 bn before the fundraising, is expanding globally to compete with ByteDance and other AI video rivals. (Reuters)

China Resources New Energy surges. China Resources New Energy (001248.SZ +136.89%) more than doubled on its Shenzhen debut after raising USD 3.6 bn in Asia’s biggest IPO this year, closing at CNY 23.95, up 137% from its CNY 10.11 offer price. The wind and solar firm’s retail tranche was 683 times subscribed, reinforcing improving risk appetite for large A-share strategic listings in renewables, semiconductors and AI infrastructure. (Reuters)

Raw material supply takes priority. CATL (300750.SZ -0.39%) said securing battery raw materials has become a key priority, with mining rather than refining now the industry's main bottleneck. The firm plans to establish a new mining unit while advancing sodium-ion batteries to reduce risks from lithium price volatility. (Reuters)

Asia ex. China

AI-capacity fears trigger sharp chip unwind. South Korea’s KOSPI fell 7.89% to 7,648.09, its lowest close since June 8, as Meta’s (META -4.9%) plan to sell excess AI computing capacity fuelled concerns about oversupply and profit-taking in chipmakers. Foreigners sold KRW 4.37 tn of shares, with Samsung (005930 KS -8.07%) and SK Hynix (000660 KS -12.62%) leading the decline. (Reuters) META is our Core Recommendation.

AI memory capex accelerates as cycle concerns rise. SK Hynix (000660 KS -12.62%) will invest KRW 100 tn, or about USD 64.4 bn, in Cheongju chip plants, including KRW 80 tn for NAND by 2029 and KRW 20 tn for advanced packaging by late 2027. The investment supports South Korea’s AI memory expansion plan, but shares sold off with Samsung (005930 KS -8.07%) as investors questioned whether AI capex can generate adequate returns. (Reuters)

Korea AI supply chain spending broadens beyond memory. Samsung Group detailed KRW 140 tn, or about USD 90 bn, of investment in South Korea’s Chungcheong region across displays, HBM packaging, batteries and advanced chip-packaging materials. Samsung (005930 KS -8.07) will invest KRW 56 tn in HBM packaging facilities, while Samsung Display, Samsung SDI (006400 KS -4.46%) and Samsung Electro-Mechanics (009150 KS -11.65%) add capacity through 2040. (Reuters)

Singapore listing priced at bottom of range. Foundation Healthcare will raise about SGD 242 mn, or USD 186.7 mn, through a Singapore IPO priced at SGD 0.76 per share, the bottom of the indicated SGD 0.76-0.92 range. The private healthcare group reported pro forma 2025 revenue of SGD 265.9 mn and adjusted core profit of SGD 51.4 mn, with trading expected to start on July 8. (Reuters)

EMEA and Others

Record high as defensives offset AI selloff. The STOXX 600 closed 1.41% higher Thursday at a record high as softer US jobs data reduced Fed-hike fears, with healthcare, food and household goods outperforming while technology fell. London’s FTSE 100, France’s CAC 40 and Germany's DAX gained 1.67%, 1.65%, and 2.16% respectively. Bayer (BAYN GR +8.9%) and Sodexo (SW FP +7.4%) led gains, while AI-linked Soitec (SOI FP -4.2%) and Aixtron (AIXA GR -10%) sold off. (Reuters)

Capital relief hopes face supervisory resistance. The ECB pushed back against bank-industry calls to lower capital requirements, arguing that current buffers support safety and have not constrained lending. ECB supervisory chief Claudia Buch said eurozone banks still have enough capital headroom to maintain payout ratios around 50%, although calculation methods and buffer structures could be simplified. (Reuters)

SNB says reform buffer is already covered. The Swiss National Bank said UBS (UBSG SW +1.96%) has sufficient capital to meet proposed tougher rules after Credit Suisse’s collapse, including a planned requirement that could add about USD 20 bn of CET1 capital. UBS pushed back that the measures are excessive and could hurt competitiveness, but the SNB said the seven-year transition and expected profits should still allow shareholder distributions. (Reuters)

Roundup separation fuels break-up optionality. Bayer (BAYN GR +8.25%) created Ruveon as a separate unit for its US Roundup business, less than a week after a legal win that blocked thousands of state-court glyphosate lawsuits. Investors and analysts viewed the move as a potential first step toward structural change or asset separation, with shares reaching their highest level since August 2023. (Reuters)

TRADERS’ CORNER

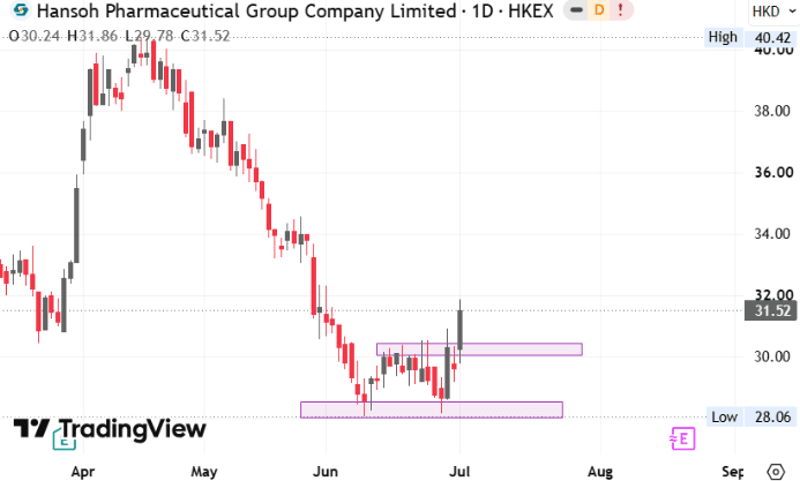

Source: TradingView | Hansoh Pharmaceutical Group (3692.HK)

Last Price: HK$31.52 Support Levels: HK$29.16 (-7.5%)/ HK$28.14 (-10.7%) Resistance Levels: HK$34.56 (+9.6%)/ HK$38.40 (+21.8%) |

Our Technical View

The price has been bottoming out and has formed a double bottom chart pattern.

Immediate buying urgency is confirmed by a successful penetration of the intermediate pivot neckline, accompanied by the RSI crossing above its 50-neutral baseline.

With the primary structural accumulation phase concluded and momentum shifting back to the long side, the technical framework favours a near-term continuous move higher.

Source: TradingView | Sinotruk Hong Kong (3808.HK)

Last Price: HK$40.26 Support Levels: HK$37.42 (-7.0%)/ HK$35.54 (-11.7%) Resistance Levels: HK$45.24 (+12.4%)/ HK$48.40 (+20.2%) |

Our Technical View

The price has successfully defended its previous low support floor.

Near-term buying urgency is expanding at this inflection point, highlighted by the RSI curling upward toward neutral territory.

With selling pressure thoroughly neutralised at the previous baseline and momentum parameters actively shifting back to the long side, the technical framework favours a near-term extension higher.

Today’s Must-Know News

Defensive bid offsets AI-chip unwind. S&P 500 was flat Thursday as the broader market rotated into healthcare (XLV +2.63%), staples (XLP +2.03%) & utilities (XLU +2.21%). Nasdaq fell 0.8% with Semis (SOXX -5.57%) down for a second day as Anthropic held talks with Samsung (005930 KS -9.06%) as a potential manufacturing partner for a custom AI chip. Meta (META -4.9%) also weighed after Zuckerberg told employees AI agent development had not accelerated as expected over the past four months. DJIA gained 1.14% to a record high; top gainers include Apple (AAPL +4.84%), McDonald’s (MCD +4.16%) & Disney (DIS +3.96%). SpaceX (SPCX +2.83%) will join the Nasdaq 100 before market open on July 7. Weak June payrolls of 57,000 and downward revisions lifted short-dated Treasuries and gold (XAU +2.28%), cutting July Fed 25-bps hike odds to 17.6% from 32.1% last week. META & XLP are our Core Recommendations; SOXX & XLV are our trading Buys.

OpenAI floats state stake. OpenAI has reportedly held preliminary talks on giving the US government a 5% stake, with CEO Sam Altman proposing a broader framework that could apply to other major US AI developers.

Burry targets memory cycle. Michael Burry shorted Micron (MU -5.49%), citing the memory maker’s cyclical earnings risk and tendency to overshoot in cycles, one day after disclosing shorts in Caterpillar (CAT -2.81%); Tesla (TSLA -7.49%) & Semis (SOXX -5.57%). MU is our Trading Buy.

Trader’s Corner (Details on Page 6-7) | ||||

Ticker | Name | Rec. | Support Levels | Resistance Levels |

3692.HK | Hansoh Pharmaceutical Group | - | HK$29.16/$28.14 | HK$34.56/$38.40 |

3808.HK | Sinotruk HK | - | HK$37.42/$35.54 | HK$45.24/HK$48.40 |

CR = Core Recommendation; TB = Trading Buy | ||||

Hong Kong IPO Calendar | |||

| Ticker | Company Name | Sector | IPO date |

| 2667.HK | Tong Ren Tang Care | Healthcare | Jul 7 |

| 1770.HK | DKE | Technology | Jul 8 |

| 6880.HK | Momenta-W | Technology | Jul 8 |

| 7656.HK | Reconova | Technology | Jul 8 |

| 7687.HK | Eacon | Consumer Disc. | Jul 8 |

| 8090.HK | Baogai | Industrials | Jul 8 |

| 9971.HK | Basic Semi | Technology | Jul 8 |

| 0537.HK | Rigol | Industrials | Jul 9 |

| 1377.HK | Dtech | Industrials | Jul 9 |

| 2475.HK | Luxshare ICT | Technology | Jul 9 |

| 2249.HK | Nexchip | Technology | Jul 10 |

| 6745.HK | Befar Group | Materials | Jul 10 |

| 2523.HK | EKH | Industrials | Jul 13 |

Americas

Anthropic stake talks denied. Anthropic has not discussed the US government taking a stake in the firm, after reports that OpenAI had discussed a potential 5% government stake. The update keeps Anthropic separate from the OpenAI proposal for now, but Washington’s scrutiny of advanced AI models, export controls and public participation in AI-sector profits remains a rising policy overhang. (Reuters)

Tesla China output rebounds. Tesla’s (TSLA -7.49%) China-made EV sales rose 24.4% yoy in June to 89,091 units, marking an eighth straight monthly increase, while 2Q China sales and exports from Shanghai rose 32.8% yoy. The rebound in Europe and resilient China demand helped offset North America softness, though BYD (1211.HK +8.07%) sold 557,090 BEVs globally in 2Q and remains a key volume threat. Separately, Tesla (TSLA -7.49%) launched the six-seater long-wheelbase Model Y L in the US, with the launch version starting at USD 61,990, after the same format helped support sales in China. (Reuters)

Nvidia widens AI monetisation. Nvidia (NVDA -1.39%) is offering token credits to AI developers in exchange for a share of future sales, aiming to turn access to its AI hardware into a recurring usage-linked earnings stream. The DSX AI factory model targets startups and researchers that lack capital for large-scale compute, potentially expanding Nvidia’s ecosystem beyond upfront GPU sales. (Bloomberg) NVDA is our Core Recommendation.

Microsoft turns AI into services. Microsoft (MSFT +1.62%) is forming a 6,000-person AI deployment organization to help enterprise customers with technical, strategic and industry-specific implementation work. The push responds to customer concerns over AI costs and mirrors a broader vendor shift toward embedded engineering support as companies seek faster ROI from model deployment. (Bloomberg) MSFT is our Core Recommendation.

Model-agnostic AI services expand. Microsoft (MSFT +1.62%) will launch Microsoft Frontier Company with USD 2.5 bn in funding to help clients such as Unilever (xx LN) and Novo Nordisk (NVO +3.4%; NOVOB DC +2.47%) choose and integrate Microsoft, third-party and open-source AI models using internal data. (Reuters) MSFT is our Core Recommendation.

Satellite internet launch edges closer, but rocket bottlenecks remain. Amazon (AMZN +0.4%) said its Leo broadband network has reached 394 satellites and is ready for initial internet service later this year, though it remains well behind SpaceX’s roughly 10,000-satellite Starlink fleet. Execution risk remains tied to launch capacity, with Blue Origin’s New Glenn and ULA’s Vulcan grounded despite Amazon booking roughly 100 launches worth at least USD 82 bn to build out more than 3,200 satellites. (Reuters) AMZN is our Core Recommendation.

Regulatory drag, cyber win. Alphabet’s Google (GOOGL -0.36%) lost its EU Android antitrust appeal, confirming a EUR 4.1 bn fine tied to agreements that favoured Search, Chrome and Play Store, raising follow-on litigation risk and adding DMA scrutiny despite the fine being less than 3% of Alphabet’s annual profit. Separately, Google said coordinated action with the FBI, Lumen (LUMN -10.07%) and other partners weakened the NetNut/Popa residential proxy network by millions of devices, while parent Alarum Technologies (ALAR IT -1.23%) said it will cooperate with law enforcement. (Reuters) GOOGL is our Trading Buy.

7-Eleven seeks to block Air Max launch. 7-Eleven sued Nike (NKE +2.39%) in Texas, alleging the planned Air Max 95 launch uses a confusingly similar orange, green and red stripe design tied to 7-Eleven’s brand and its July 11 “7-Eleven Day” promotion. The retailer is seeking to block sales, recall distributed products and recover damages and profits. (Reuters) NKE is our Trading Buy.

Redemption pressure easing but still above cap. Blue Owl Capital (OWL +4.63%%) kept a 5% quarterly withdrawal cap on two private-credit funds after investors sought USD 4.7 bn of redemptions in 2Q, down from USD 5.4 bn in 1Q. Requests remain elevated at 38.1% for OTIC and 18.8% for OCIC, but the decline supported hopes that redemption stress in non-traded BDCs may have peaked. (Reuters)

Greater China

China chip selloff drives rotation. Chinese stocks fell to a three-week low Thursday as the CSI 300 dropped 2.96%, with semiconductors leading the fall. HSI gained 0.76% as Hong Kong shares rebounded on internet strength and China Resources New Energy tripled on its listing debut. (Reuters)

US drug-sales probe ends with USD 600 mn payment. Alibaba (BABA -1.89%; 9988.HK +1.78%) and its US-based payment processor agreed to pay USD 600 mn under non-prosecution agreements over allegations they failed to prevent illegal drug, chemical and pill-press sales into the US from 2016 to 2024. The Justice Department said the transactions involved about 80k product sales and more than USD 200 mn in merchandise value, while Alibaba said the settlement reflected cooperation and improved compliance. (Reuters) 9988.HK is our Core Recommendation.

Europe comeback leans on multi-energy lineup. Great Wall Motor (601633 CH -0.4%; 2333.HK -4.88%) targets 3% to 5% European market share by 2030, supported by at least 10 new models over two years and a pivot from EV-only to petrol, hybrid and electric offerings. The firm is also assessing European manufacturing investment, while the Ora 5 compact SUV will start at EUR 26,950 and is expected to be its main volume product. (Reuters)

Kling AI secures major funding. Kling AI raised an initial USD 2 bn in venture funding to expand its AI video business, with the round potentially reaching USD 3 bn, reducing parent Kuaishou (1024 HK +2.5%) stake to about 68%. The AI video startup, valued at about USD 15 bn before the fundraising, is expanding globally to compete with ByteDance and other AI video rivals. (Reuters)

China Resources New Energy surges. China Resources New Energy (001248.SZ +136.89%) more than doubled on its Shenzhen debut after raising USD 3.6 bn in Asia’s biggest IPO this year, closing at CNY 23.95, up 137% from its CNY 10.11 offer price. The wind and solar firm’s retail tranche was 683 times subscribed, reinforcing improving risk appetite for large A-share strategic listings in renewables, semiconductors and AI infrastructure. (Reuters)

Raw material supply takes priority. CATL (300750.SZ -0.39%) said securing battery raw materials has become a key priority, with mining rather than refining now the industry's main bottleneck. The firm plans to establish a new mining unit while advancing sodium-ion batteries to reduce risks from lithium price volatility. (Reuters)

Asia ex. China

AI-capacity fears trigger sharp chip unwind. South Korea’s KOSPI fell 7.89% to 7,648.09, its lowest close since June 8, as Meta’s (META -4.9%) plan to sell excess AI computing capacity fuelled concerns about oversupply and profit-taking in chipmakers. Foreigners sold KRW 4.37 tn of shares, with Samsung (005930 KS -8.07%) and SK Hynix (000660 KS -12.62%) leading the decline. (Reuters) META is our Core Recommendation.

AI memory capex accelerates as cycle concerns rise. SK Hynix (000660 KS -12.62%) will invest KRW 100 tn, or about USD 64.4 bn, in Cheongju chip plants, including KRW 80 tn for NAND by 2029 and KRW 20 tn for advanced packaging by late 2027. The investment supports South Korea’s AI memory expansion plan, but shares sold off with Samsung (005930 KS -8.07%) as investors questioned whether AI capex can generate adequate returns. (Reuters)

Korea AI supply chain spending broadens beyond memory. Samsung Group detailed KRW 140 tn, or about USD 90 bn, of investment in South Korea’s Chungcheong region across displays, HBM packaging, batteries and advanced chip-packaging materials. Samsung (005930 KS -8.07) will invest KRW 56 tn in HBM packaging facilities, while Samsung Display, Samsung SDI (006400 KS -4.46%) and Samsung Electro-Mechanics (009150 KS -11.65%) add capacity through 2040. (Reuters)

Singapore listing priced at bottom of range. Foundation Healthcare will raise about SGD 242 mn, or USD 186.7 mn, through a Singapore IPO priced at SGD 0.76 per share, the bottom of the indicated SGD 0.76-0.92 range. The private healthcare group reported pro forma 2025 revenue of SGD 265.9 mn and adjusted core profit of SGD 51.4 mn, with trading expected to start on July 8. (Reuters)

EMEA and Others

Record high as defensives offset AI selloff. The STOXX 600 closed 1.41% higher Thursday at a record high as softer US jobs data reduced Fed-hike fears, with healthcare, food and household goods outperforming while technology fell. London’s FTSE 100, France’s CAC 40 and Germany's DAX gained 1.67%, 1.65%, and 2.16% respectively. Bayer (BAYN GR +8.9%) and Sodexo (SW FP +7.4%) led gains, while AI-linked Soitec (SOI FP -4.2%) and Aixtron (AIXA GR -10%) sold off. (Reuters)

Capital relief hopes face supervisory resistance. The ECB pushed back against bank-industry calls to lower capital requirements, arguing that current buffers support safety and have not constrained lending. ECB supervisory chief Claudia Buch said eurozone banks still have enough capital headroom to maintain payout ratios around 50%, although calculation methods and buffer structures could be simplified. (Reuters)

SNB says reform buffer is already covered. The Swiss National Bank said UBS (UBSG SW +1.96%) has sufficient capital to meet proposed tougher rules after Credit Suisse’s collapse, including a planned requirement that could add about USD 20 bn of CET1 capital. UBS pushed back that the measures are excessive and could hurt competitiveness, but the SNB said the seven-year transition and expected profits should still allow shareholder distributions. (Reuters)

Roundup separation fuels break-up optionality. Bayer (BAYN GR +8.25%) created Ruveon as a separate unit for its US Roundup business, less than a week after a legal win that blocked thousands of state-court glyphosate lawsuits. Investors and analysts viewed the move as a potential first step toward structural change or asset separation, with shares reaching their highest level since August 2023. (Reuters)

TRADERS’ CORNER

Source: TradingView | Hansoh Pharmaceutical Group (3692.HK)

Last Price: HK$31.52 Support Levels: HK$29.16 (-7.5%)/ HK$28.14 (-10.7%) Resistance Levels: HK$34.56 (+9.6%)/ HK$38.40 (+21.8%) |

Our Technical View

The price has been bottoming out and has formed a double bottom chart pattern.

Immediate buying urgency is confirmed by a successful penetration of the intermediate pivot neckline, accompanied by the RSI crossing above its 50-neutral baseline.

With the primary structural accumulation phase concluded and momentum shifting back to the long side, the technical framework favours a near-term continuous move higher.

Source: TradingView | Sinotruk Hong Kong (3808.HK)

Last Price: HK$40.26 Support Levels: HK$37.42 (-7.0%)/ HK$35.54 (-11.7%) Resistance Levels: HK$45.24 (+12.4%)/ HK$48.40 (+20.2%) |

Our Technical View

The price has successfully defended its previous low support floor.

Near-term buying urgency is expanding at this inflection point, highlighted by the RSI curling upward toward neutral territory.

With selling pressure thoroughly neutralised at the previous baseline and momentum parameters actively shifting back to the long side, the technical framework favours a near-term extension higher.

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.