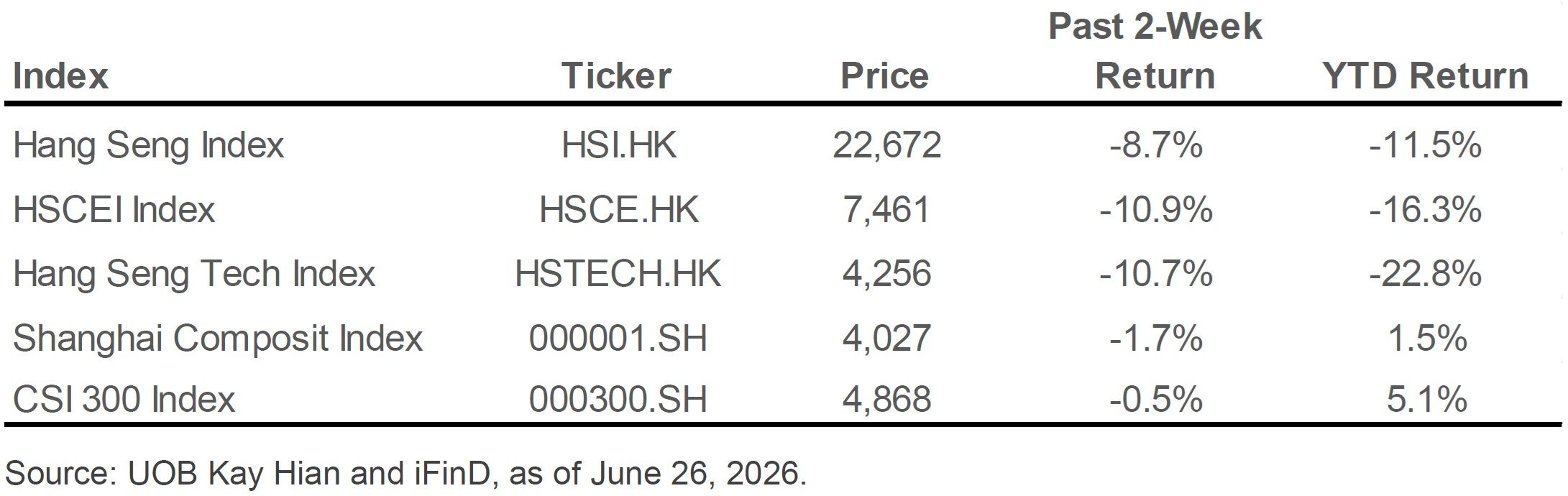

Key China Market Indices

China’s Growing Pains. Retail sales (-0.6% yoy) and fixed asset investment (-4.1% yoy) both contracted in May, reflecting the diminishing stimulus of China's consumer trade-in program and a persistent drag from macro weakness. However, exports continued to surge (+19% yoy), fueling industrial production growth (+4.5%) and resulting in a monthly trade surplus of over USD 100 bn. Divergence between a weakening domestic economy and inflationary, silicon-driven exports forms a sharp contrast and sets the macro narrative for China.

Big Tech losing shine. The Hang Seng Index retreated 8.7% over the past two weeks, extending its YTD loss to 11.5%, while the Hang Seng Tech was down sharply by 10.7%, with YTD loss widening to 22.8%. Concerns grew over intensifying AI competition and returns on investment (ROI) for Big Tech’s AI spending. A notable exception was the semiconductor industry, which outperformed under our "silicon inflation" thesis and amid the escalating US-China AI arms race.

A-shares relatively resilient. The Shanghai Composite Index declined by a relatively modest 1.7%, while the CSI 300 Index was nearly flat at -0.5%, leaving its YTD gain at a healthy 5.1%. The outperformance of A-shares reflects low foreign participation, low onshore interest rates and ongoing support from the National Team.

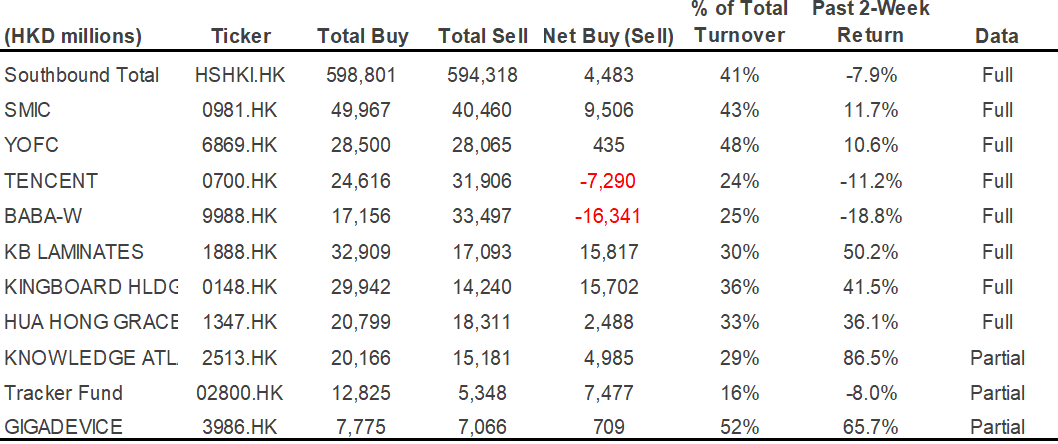

Southbound trading inflows slowed to HKD 4.5 bn but remained positive despite the broad market correction. Investors rotated decisively out of Big Tech names and into semiconductor stocks. SMIC (0981.HK) attracted a staggering HKD 9.5 bn in net buying, while Alibaba (9988.HK) suffered a record HKD 16.3 bn in net outflows.

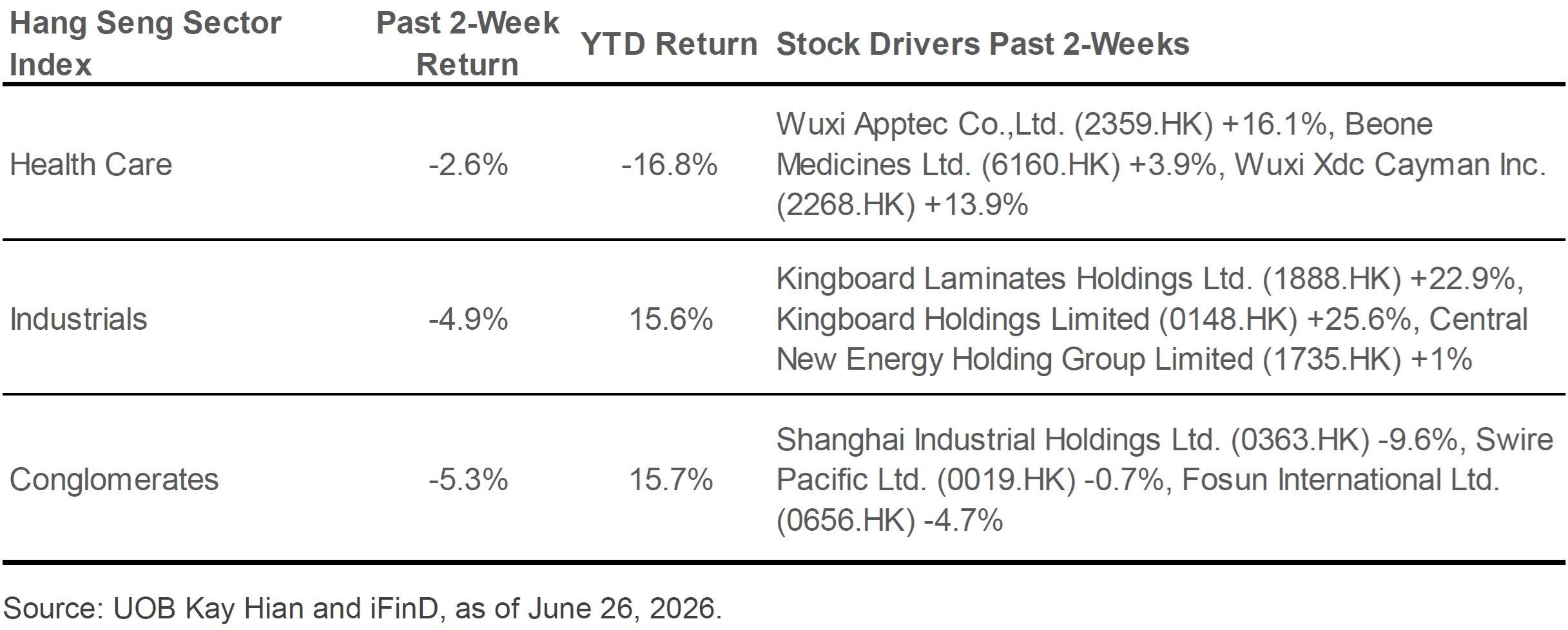

Best-performing sectors: Health Care (e.g., 2359.HK, 2268.HK) fell by a comparatively modest 2.6%; Industrials (e.g., 1888.HK, 0148.HK) fell 4.9%; Conglomerates (e.g., 0019.HK) shed 5.3%.

Potential movers and shakers:

Positive | - |

Neutral | COLI (0688.HK), CR Land (1109.HK), Longfor (0960.HK) |

Negative | Anta Sports (2020.HK), Galaxy Entertainment (0027.HK), Li Ning (2331.HK), Sands China (1928.HK), Shenzhou (2313.HK), Xtep (1368.HK) |

Must-watch events: Warsh panel appearance with Lagarde (Jul 1), Geely (0175.HK), Xiaomi (1810.HK) Jun Vehicle Sales (Jul 1), EU Trade Deal Deadline (Jul 4), FOMC June Minutes (Jul 8), China Jun CPI/PPI (Jul 9), TSM Jun Monthly Sales (Jul 10), China 2Q GDP, Jun Retail Sales (Jul 15). Earnings: None. Details below.

Date | Macro Data | Sector / Company Events |

Jun 30 | China Jun NBS PMI | China's Top 100 Developer Real Estate Sales (CIRC/CIH) |

Jul 1 | Warsh panel appearance with Lagarde, China Jun Rating Dog PMI-Mfg | Macau Jun Casino Revenue, Geely (0175.HK), Xiaomi (1810.HK) Jun Vehicle Sales est. |

Jul 3 | China Jun Rating Dog PMI-Svcs |

|

Jul 4 |

| EU Trade Deal Deadline |

Jul 7 | China Jun FX Reserves |

|

Jul 8 | FOMC June Minutes |

|

Jul 9 | China Jun CPI/PPI | Taiwan Jun Exports. |

Jul 10 |

| TSM Jun Monthly Sales, China Jun Vehicle Sales |

Jul 14 | China Jun Exports, China Jun M2 Money Supply, New Yuan Loans, Outstanding Loan Growth, Total Social Financing |

|

Jul 15 | China 2Q GDP, Jun Retail Sales, Industrial Production, Fixed Asset Investment (YTD), Unemployment rate | China Jun House Prices

|

Southbound Trading Summary (Past 2 Weeks)

Source: UOB Kay Hian and iFinD, as of June 26, 2026.

Note: Based on the two-week period from June 15 to June 26, 2026. For Stock Connect Southbound trading, only the top 10 most actively traded securities are disclosed. “Full data” means the stock appeared on the top 10 list for each of the past few trading days. “Partial data” means otherwise.

Southbound trading registered a mild net inflow of HKD 4.5 bn over the past 2 weeks, down from HKD 27.1 bn in the prior period – the weakest reading in over two months. The tepid buying came as the Hang Seng Index dropped 8.7%, against a perfect storm of macro headwinds and earning shocks rattling investor confidence. Mainland investors were not afraid to buy selected stocks on dips, as it seems.

The frenzied rotation into semiconductors and the advanced manufacturing supply chain has now overtaken the Big Tech trade. SMIC (0981.HK) headed the leaderboard with HKD 9.5 bn in net inflows as investors viewed domestic chipmakers as the primary beneficiaries of US-China tech decoupling. The semiconductor fervor spilled across the value chain: Hua Hong Semiconductor (1347.HK) attracted HKD 2.5 bn in net buying; KB Laminates (1888.HK) and Kingboard Holdings (0148.HK) each attracted inflows of HKD 15.8 bn and HKD 15.7 bn respectively, with their shares skyrocketing 50.2% and 41.5%. Knowledge Atlas (2513.HK), a domestic LLM play, was the single best-performing stock on the southbound roster – soaring 86.5%. The Tracker Fund (02800.HK) also saw net inflows of HKD 7.5 bn, indicating notable interest by mainland investors in the broader market.

Flight from Big Tech names: Alibaba (9988.HK) suffered a staggering HKD 16.3 bn in net outflows, the largest single-stock southbound outflow on record. Tencent (0700.HK) also saw heavy net outflows of HKD 7.3 bn, reversing the post-earnings optimism that had driven strong inflows in the prior period. The rotation out of internet into semiconductors signals a possible inflection: mainland investors no longer view Big Tech as their default HK allocation but instead pivot towards hardware names at the heart of the US-China AI race.

Best 3 Hang Seng Sectors (Past 2 Weeks)

Health Care was an outperformer, despite a modest overall 2.6% decline over the past two weeks. The relative resilience was driven by a sharp rebound in select CXO (contract research and manufacturing) names that had been deeply oversold previously. WuXi AppTec (2359.HK) surged 16.1% and WuXi XDC (2268.HK) rallied 13.9%, likely due to bargain hunting and short-covering post US-China biotech tensions. BeiGene (6160.HK) also edged up 3.9%. Despite this relative outperformance, the sector's YTD return remains deeply negative at -16.8%, reflecting the structural overhang of geopolitical risks on the China biotech complex.

Industrials fell 4.9% on the back of momentum in electronics supply chains and advanced manufacturing names. Kingboard Holdings (0148.HK) gained 25.6% and Kingboard Laminates (1888.HK) surged 22.9%, as investors continued to pile into PCB and laminate suppliers. These stocks have emerged as the strongest momentum trade in the Hong Kong market, with southbound investors leading the charge.

Conglomerates rounded out the top three with a 5.3% decline as the sector's diversified revenue streams and relatively robust balance sheets offered a defensive shelter. Swire Pacific (0019.HK) was nearly flat at -0.7%. The YTD return remains healthy at 15.7% for investors seeking shelter in a risk-off environment.

Worst 3 Hang Seng Sectors (Past 2 Weeks)

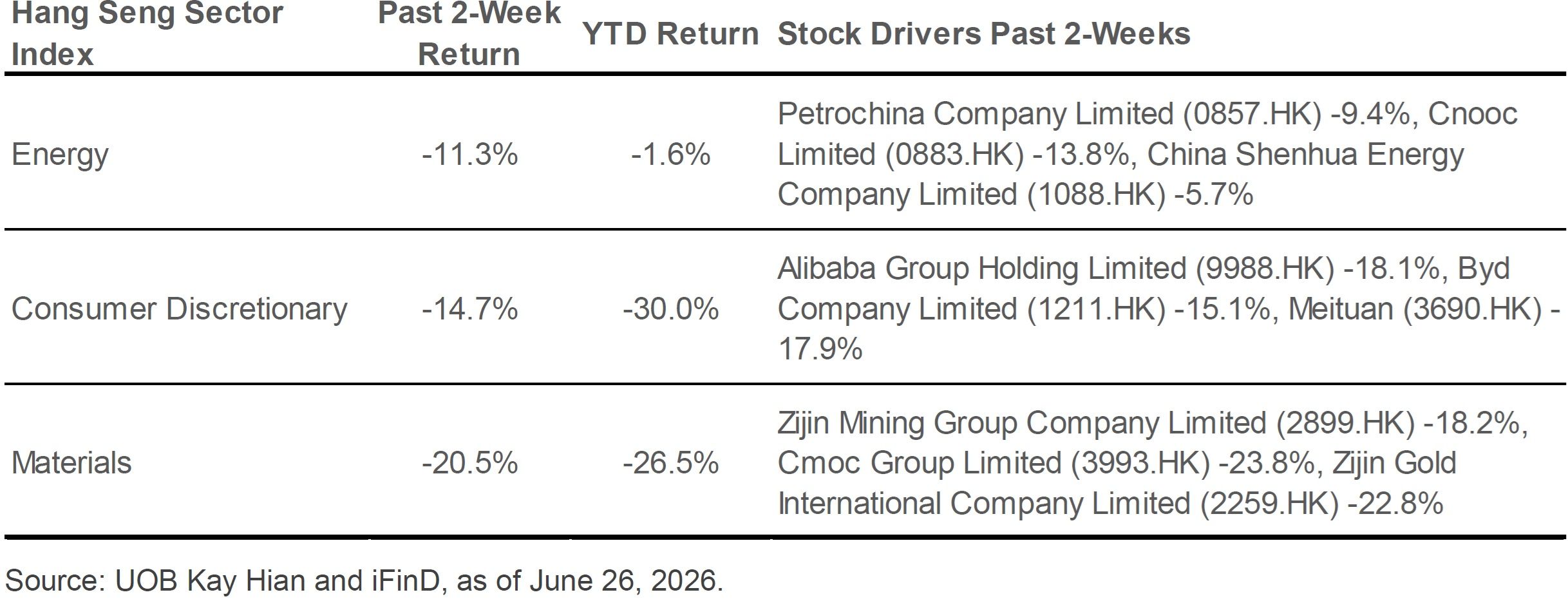

Energy slumped 11.3% as oil price declines accelerated amid the US-Iran negotiations. CNOOC (0883.HK) tumbled 13.8%, bearing the brunt of the crude price correction. PetroChina (0857.HK) fell 9.4%, and China Shenhua (1088.HK) declined 5.75%. The sector's YTD return has now slipped into negative territory at -1.6%. We maintain PetroChina as a Core Recommendation on its strong SOE moat and attractive dividend yield.

Consumer Discretionary fell 14.7%, extending its YTD loss to 30.0%. The sell-off was broad-based and unsparing. Alibaba (9988.HK) led the decline with an 18.1% retreat, hit by a perfect storm of record southbound outflows and deepening investor skepticism over the return on its AI investments. Meituan (3690.HK) tumbled 17.9% before the summer peak season of subsidy war. BYD (1211.HK) fell 15.1% amid intensified EV price wars and weakening consumer sentiment.

Materials suffered a 20.5% collapse, making it the worst-performing sector over the past two weeks. The carnage was led by a notable unwinding of precious metal names, as a sharp strengthening of the USD and a hawkish US Fed sparked a correction in commodity prices. CMOC Group (3993.HK) cratered 23.8%, Zijin Gold (2259.HK) tumbled 22.8%, and Zijin Mining (2899.HK) plunged 18.2%. The panic-selling suggests possible forced deleveraging and capitulation by momentum-driven investors.

Stocks: Potential Movers and Shakers

Stock | Sector | Type of Events | Our Take |

CR Land (1109.HK) | Real Estate | Macro / Industry Data | Neutral |

New-home sales in 19 major cities rose 2% yoy but declined 1% mom in June 2026, with sales momentum weakening in late June. Average daily new-home sales in Tier 1/2/3 cities changed by +4%, -10%, and +16% yoy, respectively, while growth across all tiers moderated after mid-month. Among Tier-1 cities, Beijing, Shanghai, Guangzhou, and Shenzhen recorded yoy sales changes of -7%, +4%, -13%, and +84%, respectively.

Resales in core cities continued to post strong sales growth, even though overall price trends remained on a downward trajectory. Average daily sales of second-hand homes in three Tier-1 cities and nine Tier-2 cities rose 13% and 4% yoy, respectively. Beijing, Shanghai, and Shenzhen saw their average daily second-hand home sales up 5%, 19%, and 12% yoy, respectively, in June.

According to the ICE Index update on 28 June, average listing prices of second-hand homes in 100 major cities fell 0.1% wow, 0.4% mom. Among the four Tier-1 cities, the listing price index of Beijing, Shanghai, Guangzhou, Shenzhen fell by 0.1%, 0.0%, 0.1%, and 0.1% wow; and by -0.5%, +0.3%, -0.2%, and -0.1% mom, and by -2.0%, +1.4%, -2.3%, and -0.7% YTD respectively. Shanghai continues to lead in second-hand home listing prices.

Maintain UNDERWEIGHT on China’s property sector. We think that the recent stabilisation in the property markets of Tier-1 cities remains policy-driven. It is still a bit too early to assess if the market has already reached a definitive bottom. The unchanged five-year loan prime rates and continued tight fiscal policy for the property sector reinforce expectations that no additional broad-based policy easing is likely in the near term. (Liu Jieqi / Damon Shen).

Stock | Sector | Type of Events | Our Take |

Galaxy Entertainment (0027.HK) | Consumer Discretionary | Macro / Industry Data | Negative |

Macau visitations slightly lower. Macau welcomed approx. 380,000 visitor arrivals during the Dragon Boat Festival holiday, representing a 2.5% yoy decline.

Maintain OVERWEIGHT. Our preferred stocks include Mengniu, Midea, Yili and Yum China. (Stella Guo/Ejann Hiew)

Stock | Sector | Type of Events | Our Take |

Anta Sports (2020.HK) | Consumer Discretionary | Earnings | Negative |

Negative read from Topsports’ 1QFY2026/2027 updates. Topsports’ 1QFY2026/2027 total sales of retail and wholesale operations registered a yoy decline in the low teens.

Management’s observations. Overall industry sales pressure increased sequentially in 2Q2026 compared with 1Q2026, with demand weakening and marked by highly promotional offerings. Sales trends have deteriorated further from June 2026, slightly lagging that of 1QFY2026/2027 and falling short of internal expectations. The management has adopted a cautious outlook for 3Q2026.

We expect this to trigger a negative read across on China sportswear names in their 2Q2026 sales performance and full-year outlook commentary. China sportswear companies are scheduled to report 2Q2026 operational results in mid-July. (Stella Guo/Ejann Hiew)

Type of Events | Explanation |

Channel Checks | Industry-wide or supply chain news with implications to a particular sector or company |

Corporate Action | Dividends, special dividends, stock splits, share buybacks, equity / bond financing, M&As, spin-offs and restructuring etc. |

Earnings | Quarterly earnings for US-listed companies. Semi-annual earnings for Hong Kong-listed companies |

Insider Dealing | Company insiders’ buying / selling of stocks and derivatives of the company |

Investor Action | Lead investor buying / selling including activist investor actions |

Investor Roadshow | Deal and non-deal roadshows, reverse roadshows (analyst days), and company meetings at investment conferences |

Legal / Regulatory | Lawsuits, legislature/regulation changes, other regulatory events |

Macro / Industry Data | Regular economic or industry data related to the sector or stock |

Sales / Products | Sales or product related news, such as monthly sales or new product launches |

Public Event | Public speeches and appearances by companies in the media or industry conferences |

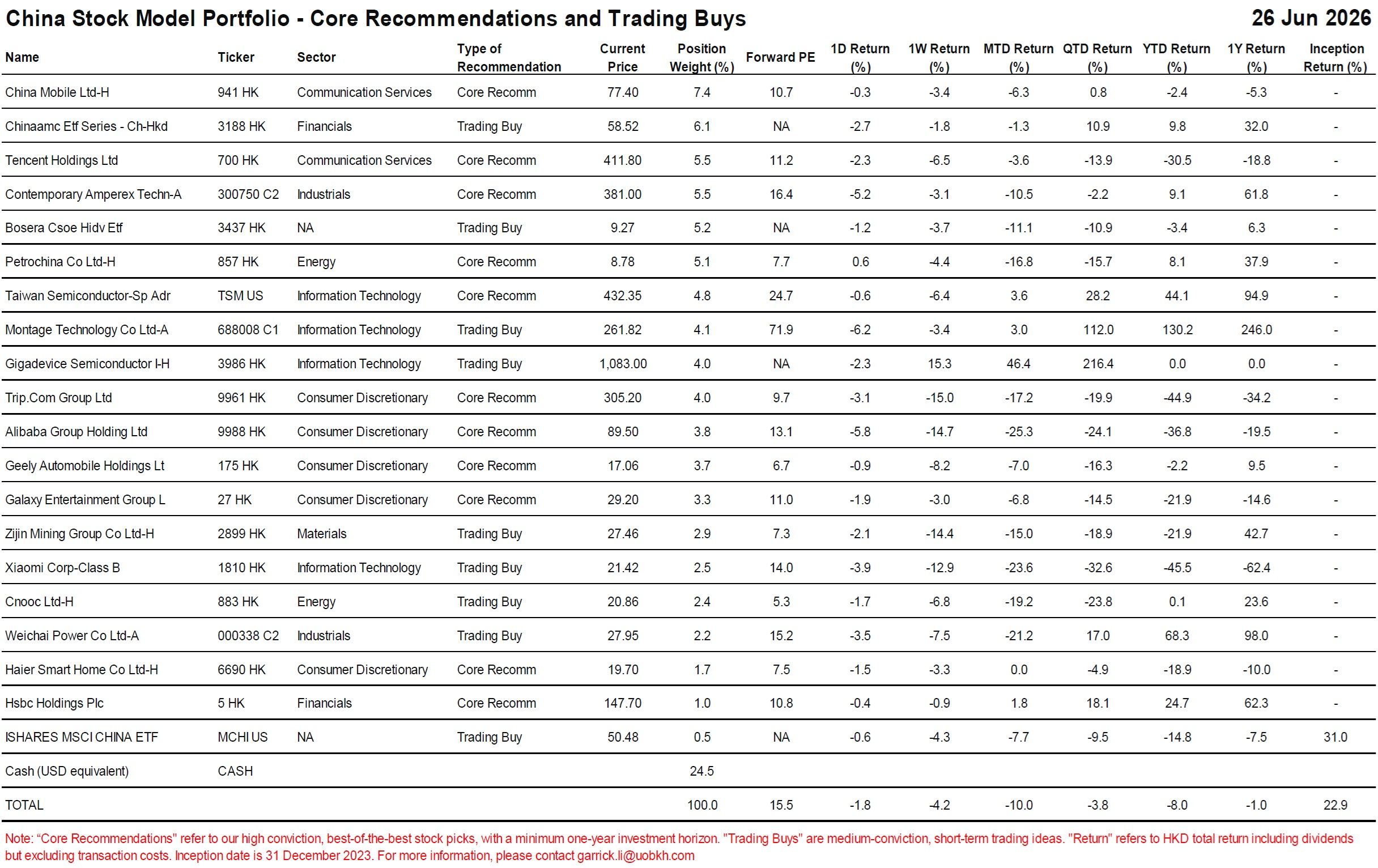

Appendix – China Stock Model Portfolio

Key China Market Indices

China’s Growing Pains. Retail sales (-0.6% yoy) and fixed asset investment (-4.1% yoy) both contracted in May, reflecting the diminishing stimulus of China's consumer trade-in program and a persistent drag from macro weakness. However, exports continued to surge (+19% yoy), fueling industrial production growth (+4.5%) and resulting in a monthly trade surplus of over USD 100 bn. Divergence between a weakening domestic economy and inflationary, silicon-driven exports forms a sharp contrast and sets the macro narrative for China.

Big Tech losing shine. The Hang Seng Index retreated 8.7% over the past two weeks, extending its YTD loss to 11.5%, while the Hang Seng Tech was down sharply by 10.7%, with YTD loss widening to 22.8%. Concerns grew over intensifying AI competition and returns on investment (ROI) for Big Tech’s AI spending. A notable exception was the semiconductor industry, which outperformed under our "silicon inflation" thesis and amid the escalating US-China AI arms race.

A-shares relatively resilient. The Shanghai Composite Index declined by a relatively modest 1.7%, while the CSI 300 Index was nearly flat at -0.5%, leaving its YTD gain at a healthy 5.1%. The outperformance of A-shares reflects low foreign participation, low onshore interest rates and ongoing support from the National Team.

Southbound trading inflows slowed to HKD 4.5 bn but remained positive despite the broad market correction. Investors rotated decisively out of Big Tech names and into semiconductor stocks. SMIC (0981.HK) attracted a staggering HKD 9.5 bn in net buying, while Alibaba (9988.HK) suffered a record HKD 16.3 bn in net outflows.

Best-performing sectors: Health Care (e.g., 2359.HK, 2268.HK) fell by a comparatively modest 2.6%; Industrials (e.g., 1888.HK, 0148.HK) fell 4.9%; Conglomerates (e.g., 0019.HK) shed 5.3%.

Potential movers and shakers:

Positive | - |

Neutral | COLI (0688.HK), CR Land (1109.HK), Longfor (0960.HK) |

Negative | Anta Sports (2020.HK), Galaxy Entertainment (0027.HK), Li Ning (2331.HK), Sands China (1928.HK), Shenzhou (2313.HK), Xtep (1368.HK) |

Must-watch events: Warsh panel appearance with Lagarde (Jul 1), Geely (0175.HK), Xiaomi (1810.HK) Jun Vehicle Sales (Jul 1), EU Trade Deal Deadline (Jul 4), FOMC June Minutes (Jul 8), China Jun CPI/PPI (Jul 9), TSM Jun Monthly Sales (Jul 10), China 2Q GDP, Jun Retail Sales (Jul 15). Earnings: None. Details below.

Date | Macro Data | Sector / Company Events |

Jun 30 | China Jun NBS PMI | China's Top 100 Developer Real Estate Sales (CIRC/CIH) |

Jul 1 | Warsh panel appearance with Lagarde, China Jun Rating Dog PMI-Mfg | Macau Jun Casino Revenue, Geely (0175.HK), Xiaomi (1810.HK) Jun Vehicle Sales est. |

Jul 3 | China Jun Rating Dog PMI-Svcs |

|

Jul 4 |

| EU Trade Deal Deadline |

Jul 7 | China Jun FX Reserves |

|

Jul 8 | FOMC June Minutes |

|

Jul 9 | China Jun CPI/PPI | Taiwan Jun Exports. |

Jul 10 |

| TSM Jun Monthly Sales, China Jun Vehicle Sales |

Jul 14 | China Jun Exports, China Jun M2 Money Supply, New Yuan Loans, Outstanding Loan Growth, Total Social Financing |

|

Jul 15 | China 2Q GDP, Jun Retail Sales, Industrial Production, Fixed Asset Investment (YTD), Unemployment rate | China Jun House Prices

|

Southbound Trading Summary (Past 2 Weeks)

Source: UOB Kay Hian and iFinD, as of June 26, 2026.

Note: Based on the two-week period from June 15 to June 26, 2026. For Stock Connect Southbound trading, only the top 10 most actively traded securities are disclosed. “Full data” means the stock appeared on the top 10 list for each of the past few trading days. “Partial data” means otherwise.

Southbound trading registered a mild net inflow of HKD 4.5 bn over the past 2 weeks, down from HKD 27.1 bn in the prior period – the weakest reading in over two months. The tepid buying came as the Hang Seng Index dropped 8.7%, against a perfect storm of macro headwinds and earning shocks rattling investor confidence. Mainland investors were not afraid to buy selected stocks on dips, as it seems.

The frenzied rotation into semiconductors and the advanced manufacturing supply chain has now overtaken the Big Tech trade. SMIC (0981.HK) headed the leaderboard with HKD 9.5 bn in net inflows as investors viewed domestic chipmakers as the primary beneficiaries of US-China tech decoupling. The semiconductor fervor spilled across the value chain: Hua Hong Semiconductor (1347.HK) attracted HKD 2.5 bn in net buying; KB Laminates (1888.HK) and Kingboard Holdings (0148.HK) each attracted inflows of HKD 15.8 bn and HKD 15.7 bn respectively, with their shares skyrocketing 50.2% and 41.5%. Knowledge Atlas (2513.HK), a domestic LLM play, was the single best-performing stock on the southbound roster – soaring 86.5%. The Tracker Fund (02800.HK) also saw net inflows of HKD 7.5 bn, indicating notable interest by mainland investors in the broader market.

Flight from Big Tech names: Alibaba (9988.HK) suffered a staggering HKD 16.3 bn in net outflows, the largest single-stock southbound outflow on record. Tencent (0700.HK) also saw heavy net outflows of HKD 7.3 bn, reversing the post-earnings optimism that had driven strong inflows in the prior period. The rotation out of internet into semiconductors signals a possible inflection: mainland investors no longer view Big Tech as their default HK allocation but instead pivot towards hardware names at the heart of the US-China AI race.

Best 3 Hang Seng Sectors (Past 2 Weeks)

Health Care was an outperformer, despite a modest overall 2.6% decline over the past two weeks. The relative resilience was driven by a sharp rebound in select CXO (contract research and manufacturing) names that had been deeply oversold previously. WuXi AppTec (2359.HK) surged 16.1% and WuXi XDC (2268.HK) rallied 13.9%, likely due to bargain hunting and short-covering post US-China biotech tensions. BeiGene (6160.HK) also edged up 3.9%. Despite this relative outperformance, the sector's YTD return remains deeply negative at -16.8%, reflecting the structural overhang of geopolitical risks on the China biotech complex.

Industrials fell 4.9% on the back of momentum in electronics supply chains and advanced manufacturing names. Kingboard Holdings (0148.HK) gained 25.6% and Kingboard Laminates (1888.HK) surged 22.9%, as investors continued to pile into PCB and laminate suppliers. These stocks have emerged as the strongest momentum trade in the Hong Kong market, with southbound investors leading the charge.

Conglomerates rounded out the top three with a 5.3% decline as the sector's diversified revenue streams and relatively robust balance sheets offered a defensive shelter. Swire Pacific (0019.HK) was nearly flat at -0.7%. The YTD return remains healthy at 15.7% for investors seeking shelter in a risk-off environment.

Worst 3 Hang Seng Sectors (Past 2 Weeks)

Energy slumped 11.3% as oil price declines accelerated amid the US-Iran negotiations. CNOOC (0883.HK) tumbled 13.8%, bearing the brunt of the crude price correction. PetroChina (0857.HK) fell 9.4%, and China Shenhua (1088.HK) declined 5.75%. The sector's YTD return has now slipped into negative territory at -1.6%. We maintain PetroChina as a Core Recommendation on its strong SOE moat and attractive dividend yield.

Consumer Discretionary fell 14.7%, extending its YTD loss to 30.0%. The sell-off was broad-based and unsparing. Alibaba (9988.HK) led the decline with an 18.1% retreat, hit by a perfect storm of record southbound outflows and deepening investor skepticism over the return on its AI investments. Meituan (3690.HK) tumbled 17.9% before the summer peak season of subsidy war. BYD (1211.HK) fell 15.1% amid intensified EV price wars and weakening consumer sentiment.

Materials suffered a 20.5% collapse, making it the worst-performing sector over the past two weeks. The carnage was led by a notable unwinding of precious metal names, as a sharp strengthening of the USD and a hawkish US Fed sparked a correction in commodity prices. CMOC Group (3993.HK) cratered 23.8%, Zijin Gold (2259.HK) tumbled 22.8%, and Zijin Mining (2899.HK) plunged 18.2%. The panic-selling suggests possible forced deleveraging and capitulation by momentum-driven investors.

Stocks: Potential Movers and Shakers

Stock | Sector | Type of Events | Our Take |

CR Land (1109.HK) | Real Estate | Macro / Industry Data | Neutral |

New-home sales in 19 major cities rose 2% yoy but declined 1% mom in June 2026, with sales momentum weakening in late June. Average daily new-home sales in Tier 1/2/3 cities changed by +4%, -10%, and +16% yoy, respectively, while growth across all tiers moderated after mid-month. Among Tier-1 cities, Beijing, Shanghai, Guangzhou, and Shenzhen recorded yoy sales changes of -7%, +4%, -13%, and +84%, respectively.

Resales in core cities continued to post strong sales growth, even though overall price trends remained on a downward trajectory. Average daily sales of second-hand homes in three Tier-1 cities and nine Tier-2 cities rose 13% and 4% yoy, respectively. Beijing, Shanghai, and Shenzhen saw their average daily second-hand home sales up 5%, 19%, and 12% yoy, respectively, in June.

According to the ICE Index update on 28 June, average listing prices of second-hand homes in 100 major cities fell 0.1% wow, 0.4% mom. Among the four Tier-1 cities, the listing price index of Beijing, Shanghai, Guangzhou, Shenzhen fell by 0.1%, 0.0%, 0.1%, and 0.1% wow; and by -0.5%, +0.3%, -0.2%, and -0.1% mom, and by -2.0%, +1.4%, -2.3%, and -0.7% YTD respectively. Shanghai continues to lead in second-hand home listing prices.

Maintain UNDERWEIGHT on China’s property sector. We think that the recent stabilisation in the property markets of Tier-1 cities remains policy-driven. It is still a bit too early to assess if the market has already reached a definitive bottom. The unchanged five-year loan prime rates and continued tight fiscal policy for the property sector reinforce expectations that no additional broad-based policy easing is likely in the near term. (Liu Jieqi / Damon Shen).

Stock | Sector | Type of Events | Our Take |

Galaxy Entertainment (0027.HK) | Consumer Discretionary | Macro / Industry Data | Negative |

Macau visitations slightly lower. Macau welcomed approx. 380,000 visitor arrivals during the Dragon Boat Festival holiday, representing a 2.5% yoy decline.

Maintain OVERWEIGHT. Our preferred stocks include Mengniu, Midea, Yili and Yum China. (Stella Guo/Ejann Hiew)

Stock | Sector | Type of Events | Our Take |

Anta Sports (2020.HK) | Consumer Discretionary | Earnings | Negative |

Negative read from Topsports’ 1QFY2026/2027 updates. Topsports’ 1QFY2026/2027 total sales of retail and wholesale operations registered a yoy decline in the low teens.

Management’s observations. Overall industry sales pressure increased sequentially in 2Q2026 compared with 1Q2026, with demand weakening and marked by highly promotional offerings. Sales trends have deteriorated further from June 2026, slightly lagging that of 1QFY2026/2027 and falling short of internal expectations. The management has adopted a cautious outlook for 3Q2026.

We expect this to trigger a negative read across on China sportswear names in their 2Q2026 sales performance and full-year outlook commentary. China sportswear companies are scheduled to report 2Q2026 operational results in mid-July. (Stella Guo/Ejann Hiew)

Type of Events | Explanation |

Channel Checks | Industry-wide or supply chain news with implications to a particular sector or company |

Corporate Action | Dividends, special dividends, stock splits, share buybacks, equity / bond financing, M&As, spin-offs and restructuring etc. |

Earnings | Quarterly earnings for US-listed companies. Semi-annual earnings for Hong Kong-listed companies |

Insider Dealing | Company insiders’ buying / selling of stocks and derivatives of the company |

Investor Action | Lead investor buying / selling including activist investor actions |

Investor Roadshow | Deal and non-deal roadshows, reverse roadshows (analyst days), and company meetings at investment conferences |

Legal / Regulatory | Lawsuits, legislature/regulation changes, other regulatory events |

Macro / Industry Data | Regular economic or industry data related to the sector or stock |

Sales / Products | Sales or product related news, such as monthly sales or new product launches |

Public Event | Public speeches and appearances by companies in the media or industry conferences |

Appendix – China Stock Model Portfolio

Disclosures and disclaimers

This report is provided subject to, and must be read together with, the full Disclosures / Disclaimers available at the following link: https://research-api.uobkayhian.com/assets/disclaimer/b2112181-0bf2-4c07-af37-3d7129735e61, which are incorporated by reference into this report. In particular, this report is intended for general circulation and informational purposes only and does not constitute personal investment advice or a recommendation to buy or sell any investment product or security. You should independently evaluate the information and, where necessary, seek advice from a qualified financial adviser regarding the suitability of any investment. Analyst certifications required under applicable regulations, including SEC Regulation AC (where relevant), are included in this report. By accessing, receiving or using this report, you acknowledge that you have read, understood and agreed to be bound by the Disclosures / Disclaimers, as may be amended, supplemented or updated from time to time.